A BIG welcome to the TCAF "Pounders"

The Sandbox Daily (7.24.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

Q2 earnings season hits full stride

U.S. dollar retest or failed breakdown?

home affordability is crashing

market valuations perplexing investors

savings fall short of desired retirement funds

What a big week for markets: interest rate policy decisions from 3 key central banks (Federal Reserve, European Central Bank, Bank of Japan) as well as earnings from market leaders across all sectors. Plenty for investors to chew on this week.

Let’s dig in.

Publisher’s note

Last week, Sam Ro of TKer was so kind and generous to spread the word of our newsletter to the masses on The Compound & Friends podcast.

Sam is a gracious friend and silent mentor of The Sandbox Daily. The words here cannot express our profound gratitude; in fact, Sam, if you are reading this, expect a big bear bull hug in Huntington Beach, California at Future Proof 2023 !!!

To all the new faces affectionately known as the “Pounders,” welcome! We are so happy to have you here. Our founding principles are to deliver value, perspective, and timeliness for capital markets.

Here is the 1-minute clip for those that missed the shoutout (click the blue YouTube hyperlink directly below):

The Compound & Friends - We Have Lost All Sense of Decorum, TCAF 102

Markets in review

EQUITIES: Dow +0.52% | S&P 500 +0.40% | Russell 2000 +0.28% | Nasdaq 100 +0.14%

FIXED INCOME: Barclays Agg Bond -0.18% | High Yield -0.17% | 2yr UST 4.913% | 10yr UST 3.874%

COMMODITIES: Brent Crude +2.22% to $82.86/barrel. Gold -0.49% to $1,995.4/oz.

BITCOIN: -2.97% to $29,175

US DOLLAR INDEX: +0.32% to 101.398

CBOE EQUITY PUT/CALL RATIO: 0.56

VIX: +2.28%to 13.91

Quote of the day

“Identifying the direction of primary trends is helpful because without understanding the environment we’re in, how could we possibly pick and choose which tools and strategies to incorporate?”

- J.C. Parets of All Star Charts, Know What Game to Play

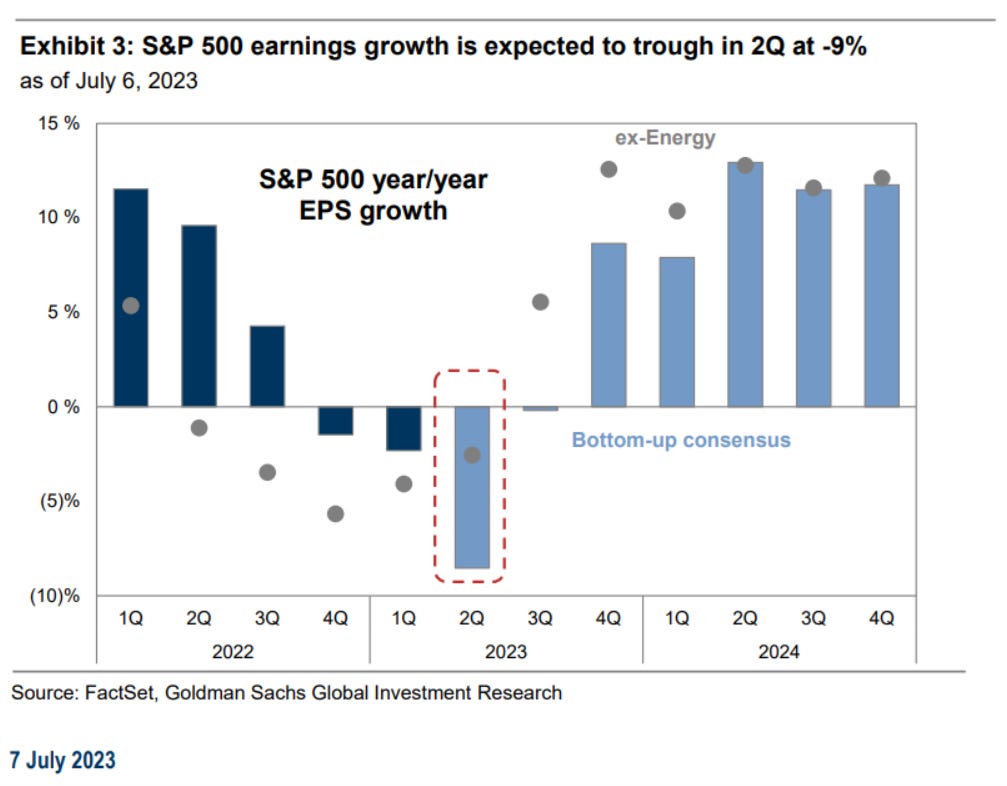

Q2 earnings season hits full stride

The S&P 500 will have 166 companies report earnings this week, nearly 40% of the index’s market capitalization.

Marquee names are reporting results every day. Big tech comes into focus with Microsoft, Alphabet, and Meta Platforms. Exxon Mobil, Visa, Mastercard, Procter & Gamble, Texas Instruments, Chevron, McDonald's, Intel, Boeing, GE, Verizon, AT&T, GM, and Ford are other notable reporters.

Consensus expects 2Q profits for the aggregate S&P 500 index to fall by -9% YoY, however, EPS growth estimates for the median S&P 500 stock are more optimistic (+1%). Many expect this reporting season to be the trough in the earnings cycle, yet S&P 500 ex-Energy EPS already troughed in Q4 of 2022, coinciding with the market bottom (October 2022).

Earnings season at this early marker is best described as better-than-feared. We will find out much more on corporate profits this week and next when a combined 336 index companies report.

Of the 89 companies in the S&P 500 (18%) that have reported, 74% have reported actual EPS above their estimates, which is below the 5-year average of 77% but slightly above the 10-year average of 73%. In aggregate, companies are reporting earnings that are +6.4% above estimates, which is below the 5-year average of +8.4% and in line with the 10-year average of +6.4%.

The blended earnings decline (blended combines actual results for companies that have reported and estimated results for companies that have yet to report) for the 2nd quarter is -9.0% today, which would mark the 3rd consecutive quarter in which the index has reported a year-over-year decline in earnings – so the earnings valley/recession is here, as expected.

Unlike the past 5 quarters, forward earnings revisions appear to have bottomed. Bottom-up consensus S&P 500 EPS estimates for 2023 and 2024 steadily declined between the start of the year and 1Q earnings season by -4% and -3%, respectively. These estimates have since stabilized and started to improve. Revision sentiment, which measures the relative shares of positive versus negative revisions, has also recovered from recessionary levels and is back to neutral territory. Earnings revision sentiment tends to move with S&P 500 returns.

Grab your popcorn, folks – should be a fun couple of weeks learning about the health of corporate America, the consumer, and where management teams see things in the 2nd half of 2023.

Source: Goldman Sachs Global Investment Research, Earnings Whispers, Fundstrat, FactSet

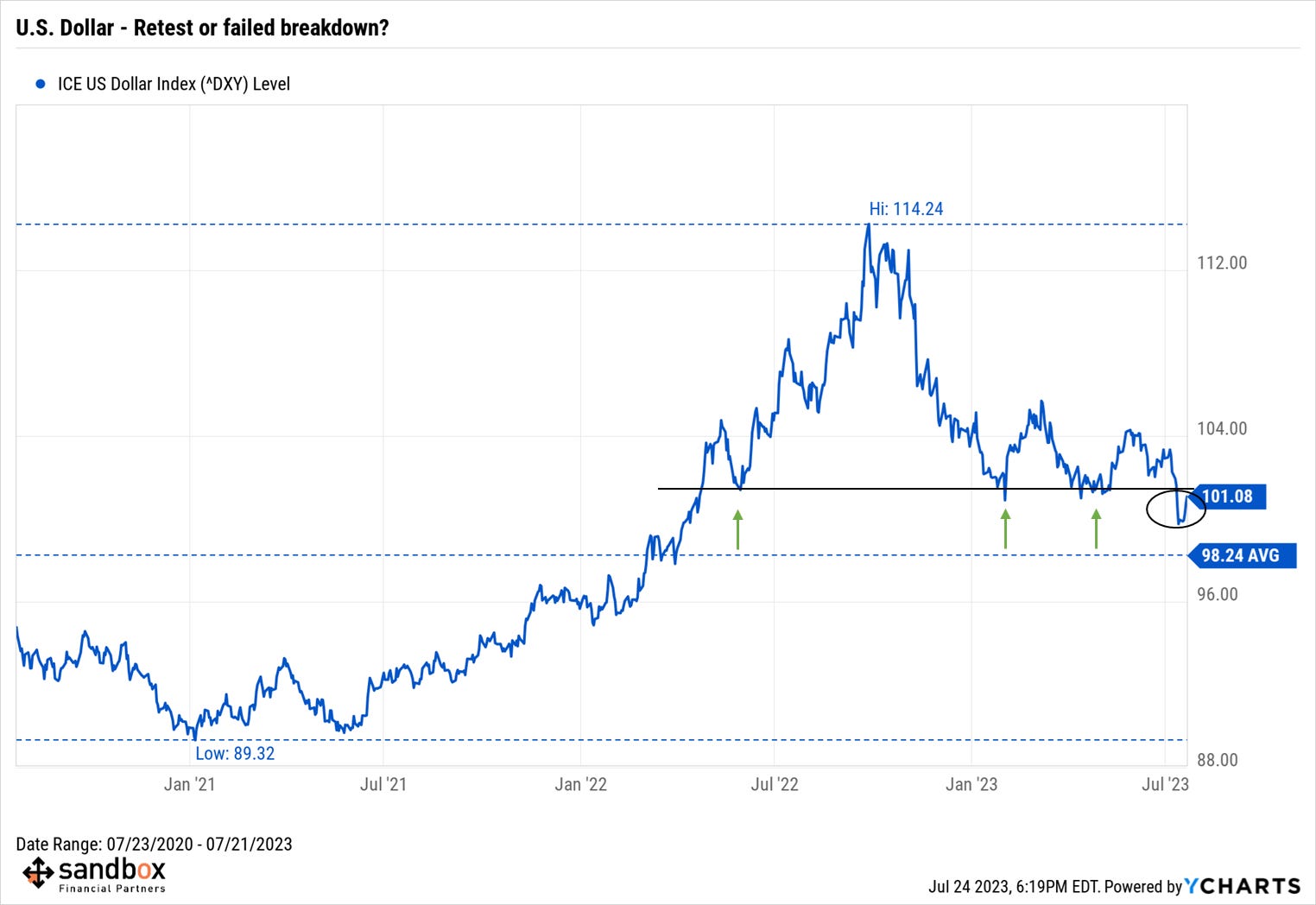

U.S. dollar retest or failed breakdown?

The U.S. Dollar Index – a geometrically-weighted basket of six currencies consisting of the euro, Japanese yen, British pound, Canadian dollar, Swedish krona, and Swiss franc – has broken down to 52-week lows of late, but King Dollar is not going down without a fight.

The U.S. Dollar Index (DXY) is trading back at a critical shelf of former 2023 lows:

A pullback in price generally resolves one of two ways: a retest followed by further weakness (continuation of the underlying trend), or a failed breakdown resulting in swift upside resolution.

Given the strong negative correlation to equities over the last five years, stock market bulls are hoping this is a simple retest. However, if this recent price action over the last 10 days represents a failed breakdown and the dollar is mounting a comeback, expect risk assets to come under increased selling pressure.

The 14-day relative strength index (RSI) falling below 30 has marked a significant shift in momentum, confirming the selling pressure may have exhausted the recent move.

Source: All Star Charts

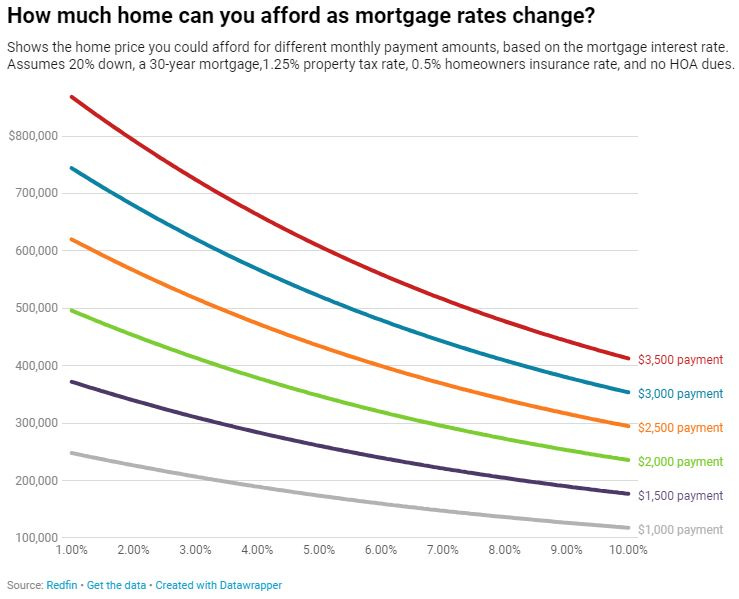

Mortgage rates are cutting into homebuyers’ budgets

A homebuyer on a $3,000 monthly budget can afford a $450,000 home with today’s average mortgage rate. That buyer has lost $30,000 in purchasing power since February 2023, when they could have bought a $480,000 home with that month’s average rate of around 6%.

Prices are rising despite relatively low demand because there are so few homes for sale.

New listings are down 27% year over year, the biggest drop since March 2020, and the total number of homes on the market is down 14%, the biggest drop since March 2022. That’s mostly because potential sellers are locked in by low rates; nearly all homeowners have a rate below 6%.

Source: Redfin

Market valuations perplexing investors

The 5 biggest companies in the S&P 500 (blue line below) are currently trading at a combined 30 times forward earnings. This is the highest level since March of 2022 and nearly 2x the multiple for the rest of the S&P 500 index.

This comes at a time when the weight of the largest stocks is around its highest level, yet not quite justified by their respective earnings.

Some call this multiple expansion, others a crowded trade.

Source: Bloomberg, J.P. Morgan Guide to the Markets

Savings fall short of desired retirement funds

Americans believe they will need to save $1.3 million for retirement.

The average amount currently saved? $89k.

Those closest to retirement had more saved, but not by much, with an average of $110,900 for those in their 50s, $112,500 for those in their 60s and $113,900 for those in their 70s.

Source: Northwestern Mutual, CNBC

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.

Respect !!

Great report - looking for to more daily commentaries !