A difficult year for the S&P 500, fresh housing data, and the one-year anniversary of the ProShares Bitcoin ETF (BITO)

The Sandbox Daily (10.19.2022)

Welcome, Sandbox friends.

Today’s Daily discusses the numbers behind the S&P 500’s difficult year, fresh data today showing the continued slowdown in the housing market, the one-year anniversary of a Bitcoin ETF, bank deposits are shrinking, and what moves the stock market over time.

Let’s dig in.

Markets in review

EQUITIES: Dow -0.33% | Nasdaq 100 -0.40% | S&P 500 -0.67% | Russell 2000 -1.72%

FIXED INCOME: Barclays Agg Bond -0.84% | High Yield -0.96% | 2yr UST 4.552% | 10yr UST 4.129%

COMMODITIES: Brent Crude +2.47% to $92.24/barrel. Gold -1.31% to $1,634.1/oz.

BITCOIN: +0.03% to $19,204

US DOLLAR INDEX: +0.68% to 112.890

CBOE EQUITY PUT/CALL RATIO: 0.66

VIX: +1.02% to 30.81

Some numbers behind the S&P 500’s difficult year

The year-to-date percentage of days that the S&P 500 index has seen a positive daily return is just 43.5%, the lowest since 1974. Years with such low percentages of up days unsurprisingly end the year in the red, with only 1982 managing a positive return after so few up days. The good news from this data is that the year following on from one with such few up days tends to see well above average returns, with an average and median return of 12% and 17% respectively (although the sample size is small).

So far this year we have seen an elevated number of instances of daily returns (positive or negative) greater than 2%. There have been 39 occurrences year to date, with 7 of these occurring in the last 14 trading days.

Source: LPL Financial

More housing data shows slowdown

Housing starts fell -8.1% in September to a 1.44 million unit annual rate, the Commerce Department reported this morning. Although the monthly changes have been switching between positive and negative territory this year, the trend in starts has been decidedly downward. September saw the second lowest level in starts since February 2021, while the three-month average was the lowest since October 2020. Excluding starts on multifamily dwellings, which can be volatile from month to month, and the decline was even more severe. Single-family starts, at an annualized 892,000 homes, were down -18.5% YoY. It’s harder to build it when you aren’t so sure they will come.

Meanwhile, the demand for mortgages fell to a quarter-century low last week as mortgage rates hover near 7%. The Mortgage Bankers Association (MBA) Market Composite Index, which last month fell below its pandemic low, reported that mortgage application volume fell -4.5% from the week before, reaching the lowest level since 1997. Applications are into their fourth straight month of declines. Homebuyers’ demand for mortgages is now down -38% YoY. Dwindling mortgage applications reflect more cyclical weakness in housing demand and imply that home sales will continue to shrink in the near-term.

Sources: United States Census Bureau, Bloomberg, Wall Street Journal, Ned Davis Research, Mortgage Bankers Association, Calculated Risk

One year anniversary for a Bitcoin ETF

The ProShares Bitcoin Strategy ETF (BITO) launched one year ago on October 18th, 2021. This matters because BITO was the first U.S. bitcoin-linked ETF offering investors an opportunity to gain exposure to bitcoin returns in a convenient, liquid, and transparent way.

So, after one-year, how are things going? BITO is down -71.77%, while the underlying asset itself (Bitcoin) is down -68.58%.

Despite the difficult macro backdrop and abysmal performance, the fund’s assets under management (AUM) have drifted down but still remain healthy.

Source: ProShares

Bank deposits are shrinking

Tracking bank deposits as an inflationary or disinflationary measure is important when you consider that all money is lent into existence.

The lending process – and therefore money creation – begins with bank deposits. As bank deposits shrink, as they recently have been, less money is created. As shown below, money supply growth is shrinking quickly and in line with bank deposits. This bodes well for inflation. The interplay between the money supply and monetary velocity, or how often money circulates, drives inflation. With bank deposits and the money supply growth shrinking, inflation should decline. If the economy weakens further and velocity slows, inflation could fall rapidly.

Source: Lance Roberts

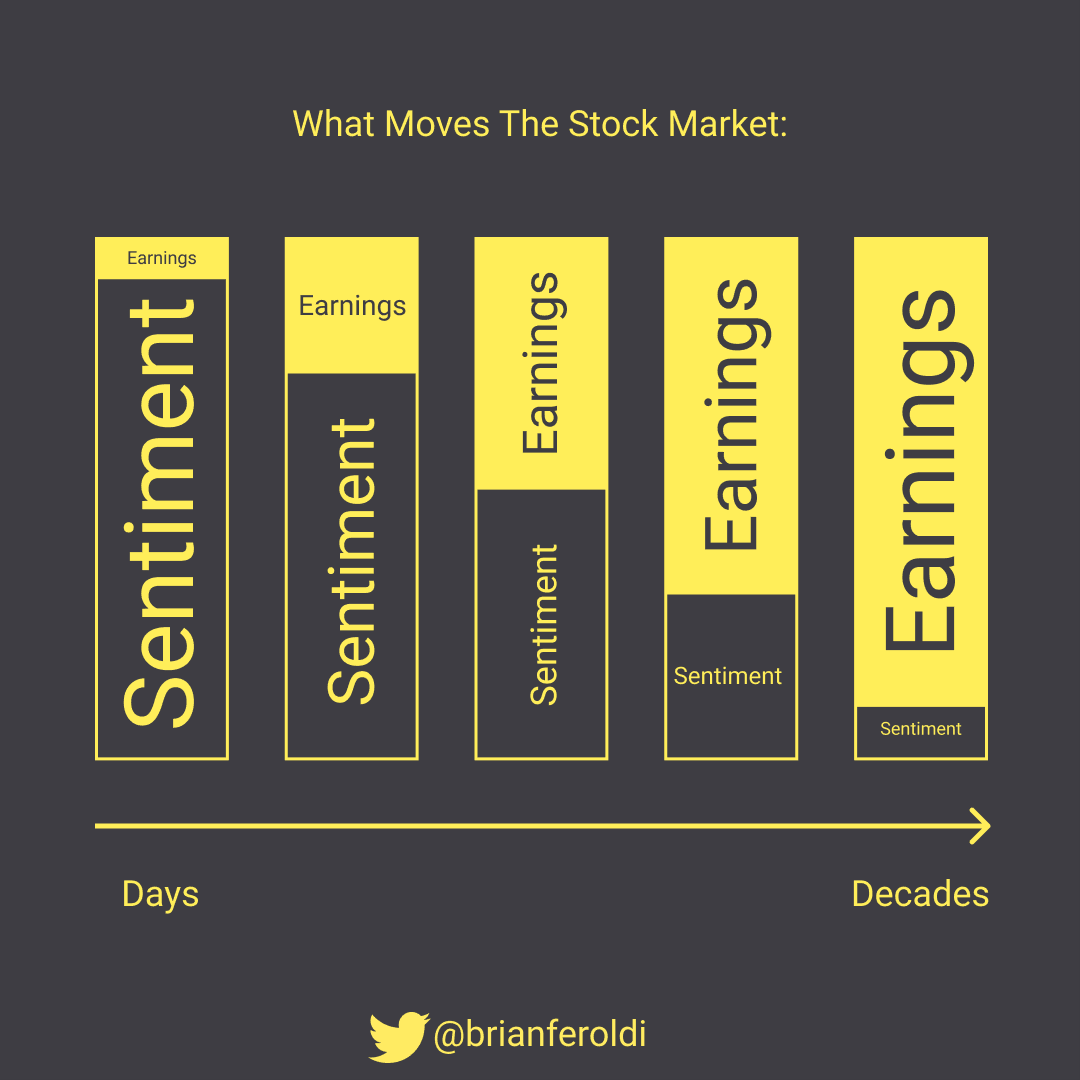

Time horizon matters

Short term results can often be driven by investor sentiment, flows, price momentum, and technicals, while long term results are mainly predicated on the company’s ability to deliver shareholder value.

As Warren Buffett once said: “Price is what you pay; value is what you get.”

Source: Long-Term Mindset

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.