America's debt problem, plus Bitcoin, behavioral finance, and the week in review

The Sandbox Daily (2.17.2023)

Welcome, Sandbox friends.

Today’s Daily discusses the New York Fed’s quarterly report on household debt and credit, Bitcoin breaks out of its base, the psychology of portfolio happiness, and a brief recap to snapshot the week in markets.

Have a wonderful long Presidents’ Day weekend.

Let’s dig in.

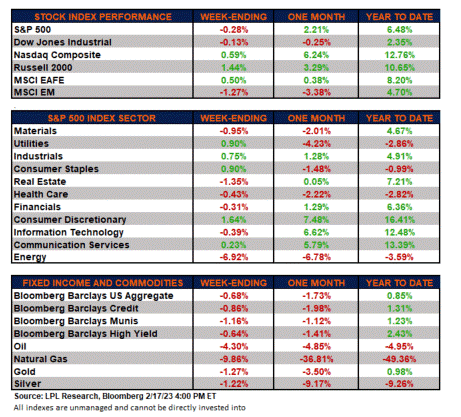

Markets in review

EQUITIES: Dow +0.39% | Russell 2000 +0.21% | S&P 500 -0.28% | Nasdaq 100 -0.68%

FIXED INCOME: Barclays Agg Bond +0.24% | High Yield +0.39% | 2yr UST 4.621% | 10yr UST 3.817%

COMMODITIES: Brent Crude -2.58% to $82.95/barrel. Gold -0.02% to $1,851.4/oz.

BITCOIN: +0.88% to $24,769

US DOLLAR INDEX: +0.02% to 103.877

CBOE EQUITY PUT/CALL RATIO: 0.60

VIX: -0.74% to 20.02

Debt balances continue expand

Total household debt rose by $394 billion, or 2.4%, to $16.90 trillion in the fourth quarter of 2022, according to the latest Quarterly Report on Household Debt and Credit.

Total U.S. credit card debt balances increased by $61 billion to reach $986 billion – a record high – surpassing the pre-pandemic high of $927 billion.

Mortgage balances rose to $11.92 trillion, auto loan balances to $1.55 trillion, and student loan balances to $1.60 trillion.

The share of current debt transitioning into delinquency increased for nearly all debt types.

Fastest rising interest rates in history with record credit card debt. What could possible go wrong?

Source: Federal Reserve Bank of New York

Bitcoin breaks out of its base

Bitcoin (BTC) is on track to reach its highest level in over eight months as bulls reclaim the highs from late last summer. After trading in a sideways range for most of the trailing month and digesting gains from the January runup, buyers appear to be taking control of the short-term trend once again.

Here is a daily chart showing BTC pressing on the upper bounds of its current consolidation:

If today’s move holds, it could signify much more than just new highs. Bitcoin is on the verge of resolving higher from a major bearish-to-bullish reversal pattern.

Notice how momentum achieved one of its highest readings on record in January while the long-term moving average flattened out and curled higher. These are common characteristics of a trend reversal. We're looking for price to confirm the potential uptrend over the coming weeks.

Source: All Star Charts

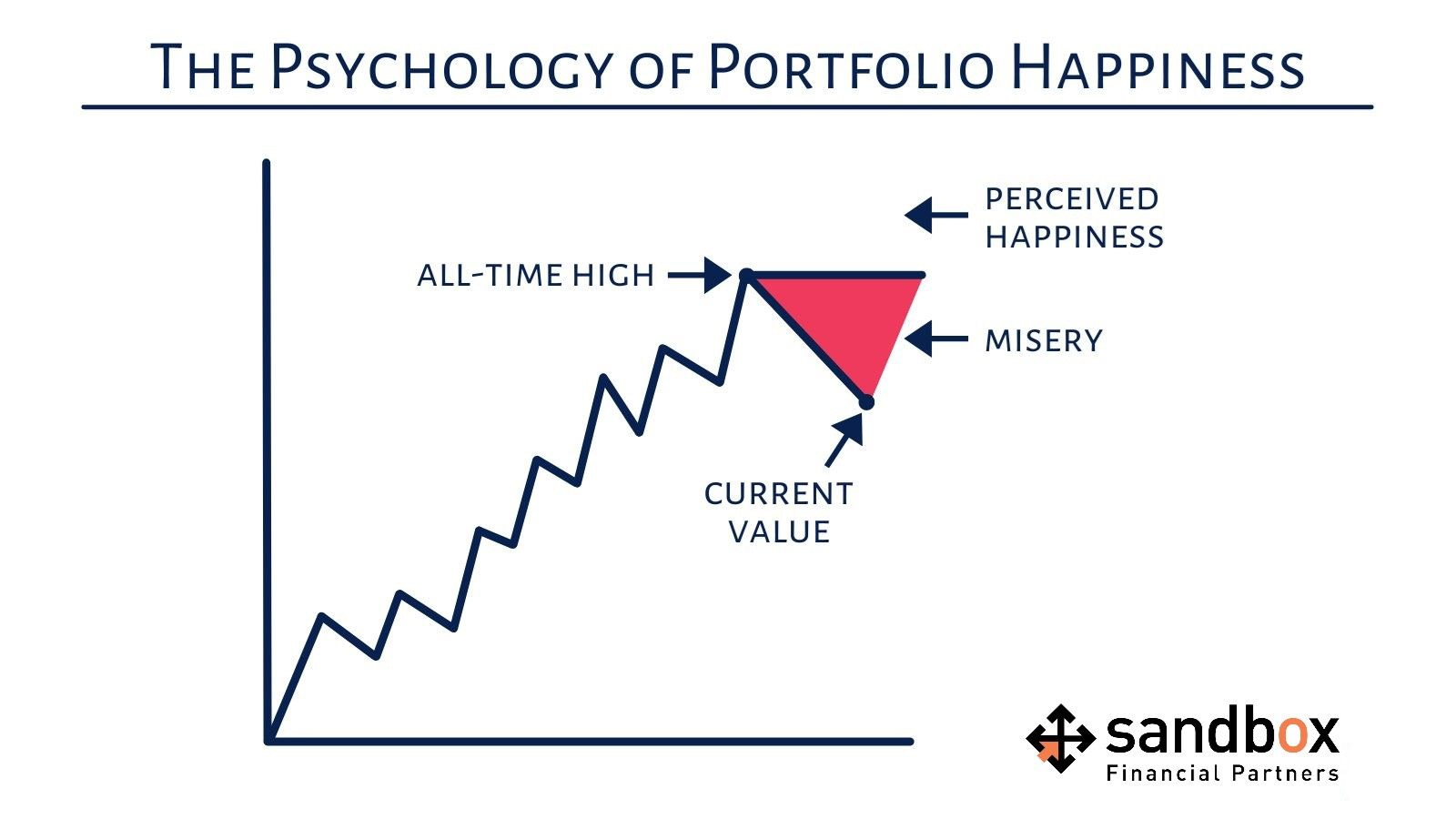

One simple graphic

The stock market is only at all-time highs 5% of the time, which is why we spend the majority of our investing life in misery.

This helps explain why people try to shortcut the process of wealth accumulation by chasing returns, adding leverage, and making concentrated bets.

Have an investment plan – stick to it and you'll be rewarded over time. If you don't have a good plan, then it’s time to start one. Not tomorrow. Not week. Now.

Source: Sandbox Financial Partners

The week in review

Talk of the tape: Another risk-off move this week amid more focus on the latest repricing of the Fed rate path after some macro updates this week showed strong economic growth and more persistent inflation that led to more hawkish Fed commentary. St. Louis Fed's Bullard added to the upside risk as officials seemingly putting 50 bps hikes back into play. The Fed rate path adding uncertainty to the soft-landing or no-landing scenarios, with BofA saying a 1st half no landing could lead to a 2nd half hard landing for both markets and the economy. However, some noted that the peak level Fed officials have discussed is only slightly higher the December median dot, suggesting cycle peak not dramatically higher.

Bullish narratives continue to center around factors including strong economy, consumer resilience, milder earnings reset scenarios, and stronger economic growth in Eurozone and China.

Stocks: The major market averages finished mixed, with sector action varied. This week, energy performed poorly on the back of lower oil and natural gas prices. International markets also ended the week mixed as these economies continue to perform better than expected amid global price pressures and energy supply concerns.

So far this year, the Dow Jones Industrial Average is lagging the S&P 500 by its largest margin since 1934, as the blue-chip average outperformed the S&P 500 by 11% in 2022. Investors have been shifting risk from blue-chip value names to growth sectors, like communication services, consumer discretionary and information technology, on the belief the Fed will change course on rates.

Bonds: The Bloomberg Aggregate Bond Index finished the week lower as yields increased for the second straight week. Bonds have been directly influenced by hawkish Fed speak last week in addition to marginally higher-than-anticipated inflation print.

Commodities: Many commodity watchers believe that oil could return to $100 a barrel this year amid China’s reopening along with better-than-expected economic reports out of Europe. However, energy prices declined this week as traders are concerned that the Federal Reserve will not pivot on monetary policy given last month’s inflation prints. The major precious metals, gold and silver, finished the week lower, following energy’s path lower given future economic growth concerns.

Source: Dwyer Strategy, LPL Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.