Assembling the market’s jigsaw puzzle

The Sandbox Daily (2.24.2026)

Welcome, Sandbox friends.

Today’s Daily discusses:

the market’s jigsaw puzzle

Let’s dig in.

Blake

Markets in review

EQUITIES: Russell 2000 +1.20% | Nasdaq 100 +1.09% | S&P 500 +0.77% | Dow +0.76%

FIXED INCOME: Barclays Agg Bond -0.01% | High Yield -0.07% | 2yr UST 3.465% | 10yr UST 4.035%

COMMODITIES: Brent Crude -0.11% to $71.41/barrel. Gold -0.91% to $5,178.2/oz.

BITCOIN: -0.05% to $63,898

US DOLLAR INDEX: +0.18% to 97.879

CBOE TOTAL PUT/CALL RATIO: 0.93

VIX: -6.95% to 19.55

Quote of the day

“I know I’m gonna get got, but I’m gonna get mine more than I get got though.”

- Marshawn Lynch, Seattle Seahawks

The market’s jigsaw puzzle

If markets are a jigsaw puzzle, as Goldman’s Tony Pasquariello wrote this morning, the U.S. equity market is one huge messy pile scattered across the table – pieces lack order, edges hard to find, the picture not yet obvious.

Technology stocks have been slammed particularly hard, with the Tech Sector SPRD $XLK down roughly 4% year-to-date and scores of individual stocks down 20% or more, as scrutiny around AI spending and disruption fears – particularly in software – have triggered aggressive de-risking.

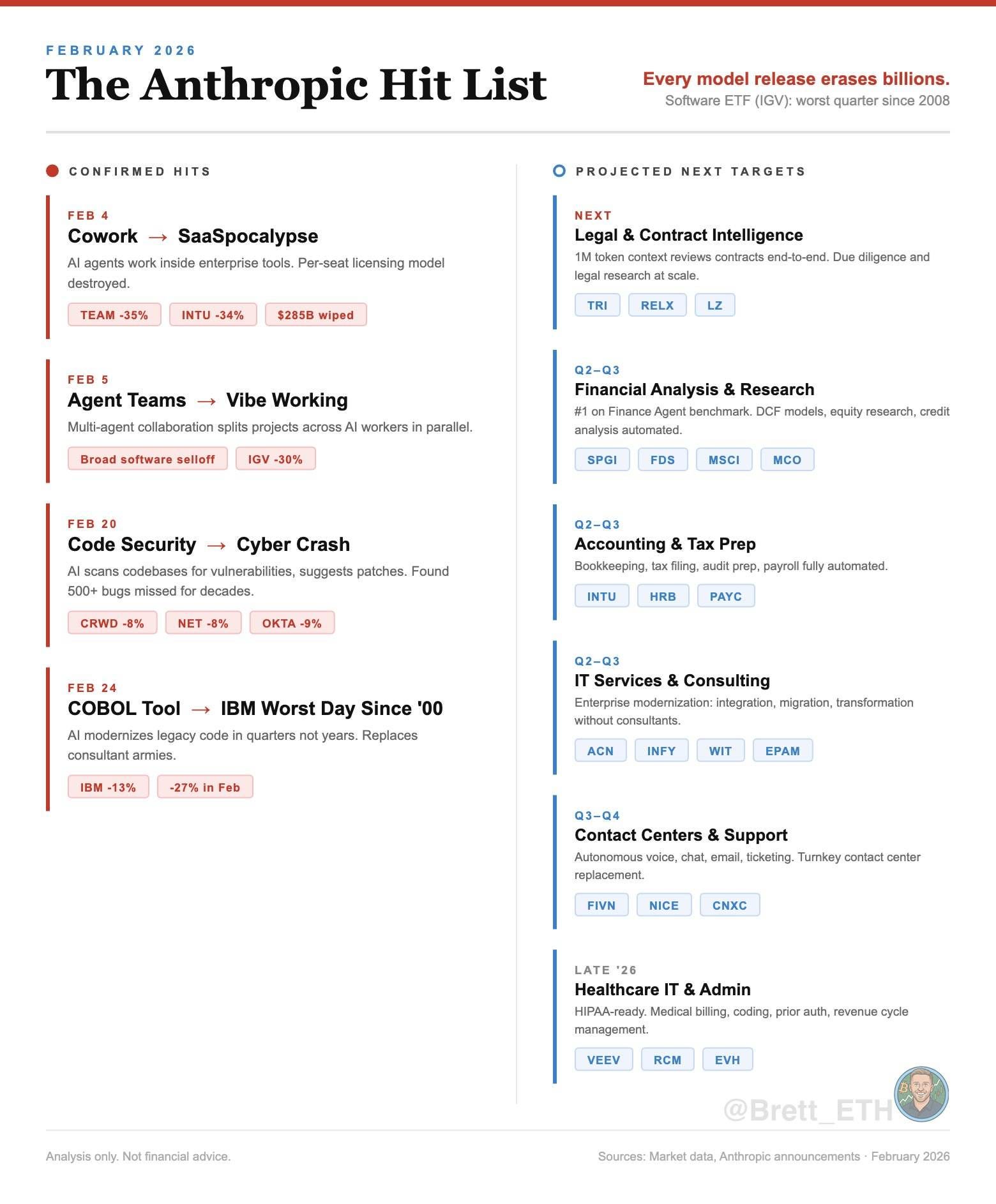

In the last 3-4 weeks, Anthropic’s Claude Code releases have only amplified anxiety that AI may compress margins before it expands them.

As shown below, Claude single-handedly triggered several waves of market selloffs.

A few weeks back, whiz kid Matt Shumer broke the internet with “Something Big is Happening”.

In short, AI has reached an inflection point from possibility to reality and Matt argues that AI’s capabilities are greatly underappreciated by the wider public.

Then it was a viral blog post over the weekend from small research firm Citrini Research and its 33-year old founder that triggered a stock market meltdown on Monday.

The dystopian report described a hypothetical economic plunge in which mass white-collar layoffs create a deflationary cascade that pushes the unemployment rate above 10% while stock prices get wiped out. It goes on to describe the risk of “Ghost GDP,” which represents a scenario where AI drives massive productivity gains and corporate profits even as wage growth and employment weaken beneath the surface.

But, take a step back from this AI doom vortex and the broader canvas looks… fine?

The underlying fundamentals of the U.S. economy still remain more or less on solid footing.

Inflation continues to moderate, real economic growth (GDP) grew at a healthy 2.2% pace for all of 2025, and corporate earnings remain robust – all of which support valuations and long run growth. This in spite of some yellow flags that exist at the margin: labor market direction of travel, rising margin debt, and the upcoming changing of the guard at the Fed Chair in May.

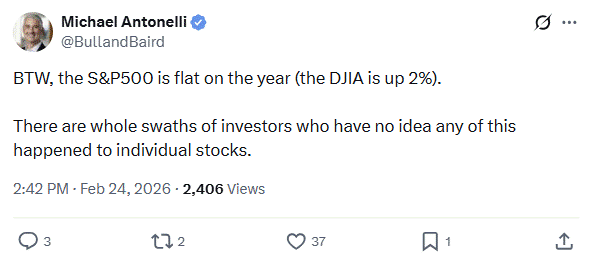

The S&P 500 is flat on the year. The Dow is up ~2%. International markets up mid-single digits.

Under the surface, however, there has been real violence.

Software has endured its largest non-recessionary drawdown in three decades, with positioning collapsing to extreme lows and short interest surging.

As Michael Antonelli quipped: “There are whole swaths of investors who have no idea any of this happened to individual stocks.”

Capital has rotated aggressively into value, commodities, international stocks, and small caps – anything underowned and optically “cheap.”

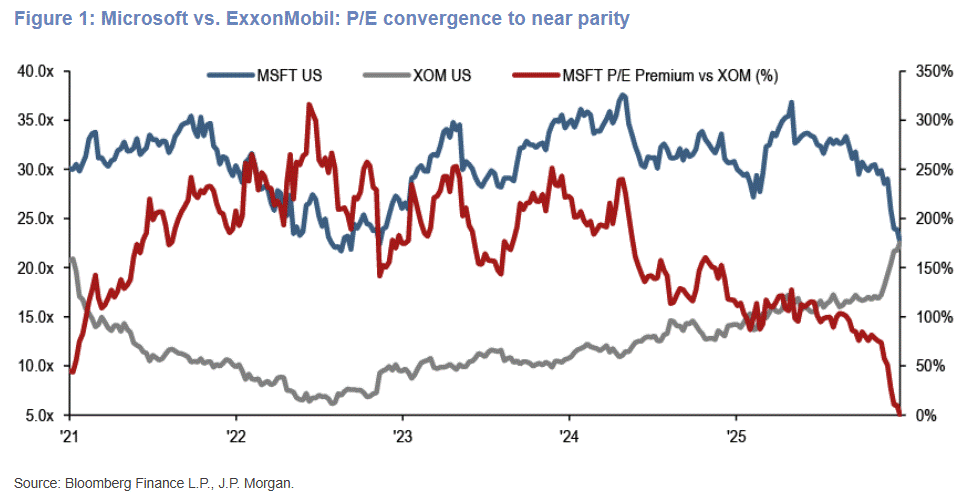

JPMorgan argues that this rally is now roughly “85% complete,” with crowding near decade highs and the valuation gap between former Quality bellwethers and 2026 winners nearly erased.

As one example, Microsoft now trades at a multiple not meaningfully different from Exxon. That’s not a sign of tech excess. It’s a sign of rotation excess.

Importantly, Tech fundamentals haven’t cracked. Consensus still expects double-digit sales and earnings growth for software in 2026, margins remain healthy, and balance sheets are strong.

Where the market likely has this whole AI-doom narrative askew is AI will likely enhance many platforms, rather than replace them – particularly in cybersecurity and workflow automation.

And technically, the market hasn’t deteriorated either.

Major indices remain range-bound, with one of the narrowest starts to a year in over 40 years.

Equal-weight indices are still trending higher, while breadth indicators and measures like the NYSE Advance-Decline Line show widespread participation and strength.

So what’s really happening?

This is market rotation, period.

A positioning unwind in crowded trades, not a structural collapse.

A diversification impulse after a narrow leadership regime.

The puzzle is messy, but the picture isn’t broken.

Respect the volatility. Move light and tight. And, above all, stay on target.

Sources: Goldman Sachs Global Investment Research, Anthropic, Matt Shumer, Citrini Research, Michael Antonelli, J.P/ Morgan Markets

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures (click here)

Please see our SEC Registered firm brochure (click here)

Please see our SEC Registered Form CRS (click here)