Back from the beach: August in review

The Sandbox Daily (9.2.2025)

Welcome, Sandbox friends.

Today’s Daily discusses:

back from the beach

Let’s dig in.

Blake

Markets in review

EQUITIES: Dow -0.55% | Russell 2000 -0.60% | S&P 500 -0.69% | Nasdaq 100 -0.79%

FIXED INCOME: Barclays Agg Bond -0.27% | High Yield -0.11% | 2yr UST 3.645% | 10yr UST 4.275%

COMMODITIES: Brent Crude +1.47% to $69.15/barrel. Gold +2.33% to $3,598.1/oz.

BITCOIN: +1.91% to $111,239

US DOLLAR INDEX: +0.57% to 98.326

CBOE TOTAL PUT/CALL RATIO: 0.83

VIX: +6.51% to 17.17

Quote of the day

“Life is a verb. Life is not a noun. It is really 'living,' not 'life.' It is not love, it is loving. It is not relationship, it is relating. It is not a song, it is singing. It is not a dance, it is dancing. See the difference, savor the difference.”

- Osho

Back from the beach: month in review

As summer winds down, September brings a shift in pace and focus. Schools are back in session, businesses ramp up towards year-end, and markets often take on a sharper tone.

For investors, that makes this a natural checkpoint.

The past month delivered a mix of strong performance and mounting uncertainty, a reminder that it’s never wise to leave portfolios fully on autopilot. Elevated valuations, shifting economic signals, and policy moves out of Washington all deserve attention as we head into the fall.

August insights

The stock market climbed to new all-time highs in August, while bonds also contributed positively to portfolios. This occurred despite continued uncertainty around tariffs, Fed independence, and technology stocks.

Markets stumbled mid-month due to concerns that the Fed could keep rates higher for longer to fight inflation. Recent inflation reports, such as the Producer Price Index (PPI), suggest that companies are beginning to pass tariff costs through to consumers.

However, market sentiment quickly rebounded due to better-than-expected corporate earnings and greater confidence that the Fed will cut policy rates at its upcoming September meeting following Chair Powell’s speech at Jackson Hole.

Economic figures were mixed. GDP growth for the 2nd quarter was revised higher from 3.0% to 3.3%, a strong improvement from the first quarter's 0.5% decline. However, the jobs report published at the start of the month showed a significant decline in new payrolls, including large downward revisions to prior months. This led the White House to fire the Commissioner of the Bureau of Labor Statistics, adding to the uncertain environment.

Despite these challenges, market volatility remains low by historical standards.

Key Market and Economic Drivers

The S&P 500 rose 1.9% in August, the Dow Jones Industrial Average 3.2%, and the Nasdaq 1.6%. Year-to-date, the S&P 500 is up 9.8%, the Dow is up 7.1%, and the Nasdaq is up 11.1%.

The Bloomberg U.S. Aggregate Bond Index gained 1.2% in August. The 10-year Treasury yield ended the month lower at 4.2%.

International developed markets jumped 4.1% in U.S. dollar terms using the MSCI EAFE index, while emerging markets gained 1.2% based on the MSCI EM index. Year-to-date, the MSCI EAFE index has gained 20.4% and the MSCI EM index 17.0%.

Bitcoin fell in August, ending the month at 109,127 after experiencing a “flash crash” on August 24.

Gold prices ended the month at a new all-time high of $3,487.

The Consumer Price Index rose 2.7% on a year-over-year basis in July, in line with economist expectations.

The jobs report showed that the economy added only 73,000 jobs in July. Significant downward revisions to the May and June figures mean that the labor market was much weaker than originally reported. The unemployment rate remained low at 4.2%.

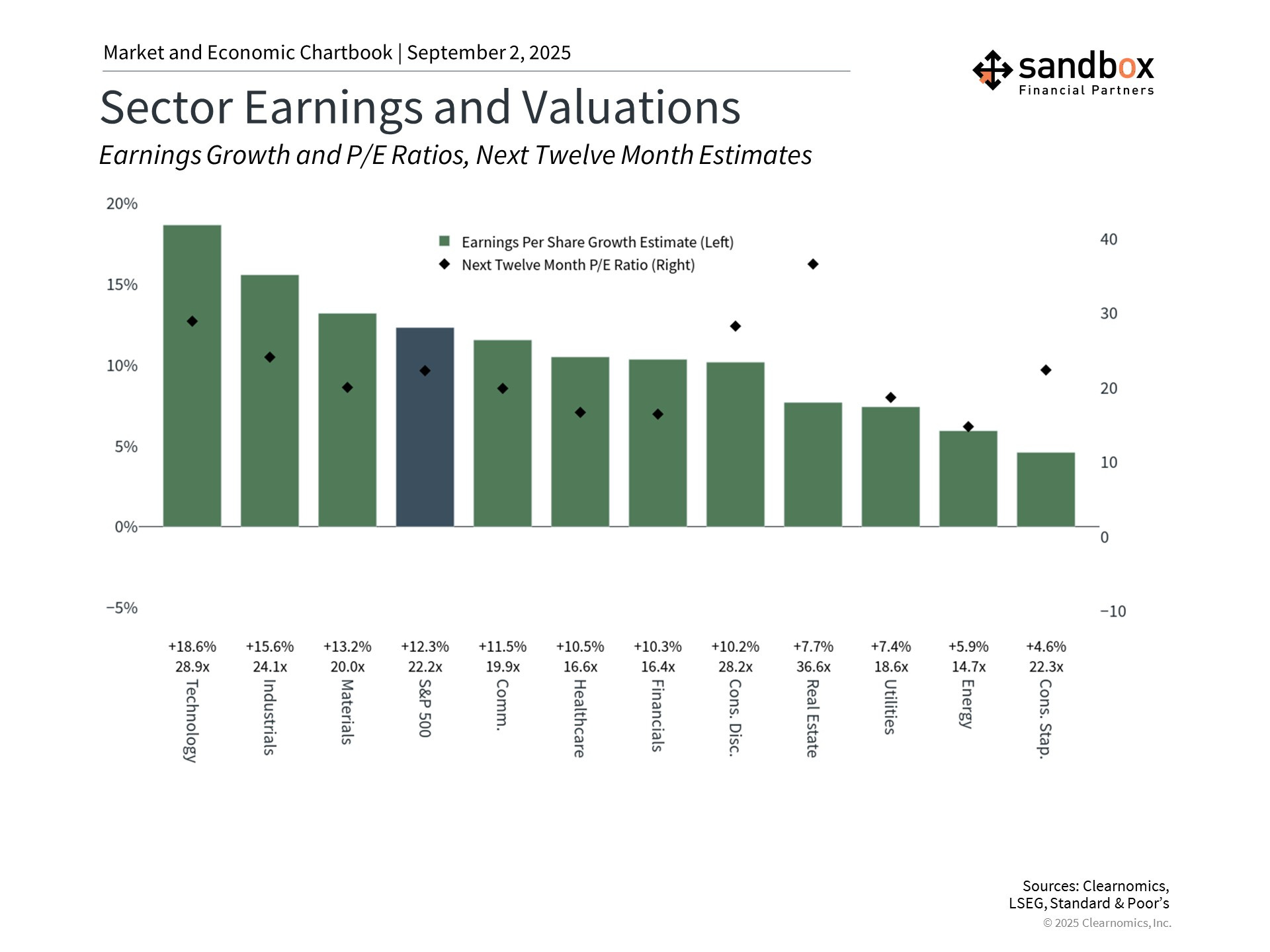

Markets climbed higher on healthy earnings

While day-to-day news and headlines can drive markets in the short run, fundamentals like earnings and valuations are what affect portfolio returns in the long run.

Although stock market valuations are quite high by historical standards, this is supported by corporations that continue to grow earnings at a healthy pace.

The latest earnings season numbers show that 83% of S&P 500 companies have beaten estimates, the highest percentage since 3Q23, while profits grew 12% versus 4% expectations – thus demonstrating that the economy and corporate fundamentals have been quite strong.

This also underscores the adaptability of companies as they adjust to tariffs, absorb higher costs, and find ways to grow despite policy uncertainty.

The Fed is expected to cut rates

In contrast, consumer-facing businesses reported mixed results due to changing household spending patterns. This is exacerbated by the implementation of tariffs, as companies pass on a greater proportion of tariff costs to consumers.

Combined with the weaker-than-expected jobs data, markets began anticipating greater rate cuts beginning in September.

Fed Chair Jerome Powell, in a speech at their annual conference in Jackson Hole, Wyoming, provided the clearest signal yet that the central bank is prepared to resume cutting interest rates after pausing this year.

Remember, the Fed has a “dual mandate” to keep inflation steady and unemployment low. Recently, they have kept interest rates relatively high due to stubborn inflation and a strong job market. Thus, early signs of job market softness should tip the Fed’s decision-making toward proactive rate cuts.

Fed rate cuts can create opportunities across asset classes

The prospect of additional Fed rate cuts could create opportunities across asset classes.

In addition to supporting broad economic growth, lower interest rates can improve borrowing costs for companies, reduce hurdles for new projects, and increase the present value of future cash flows.

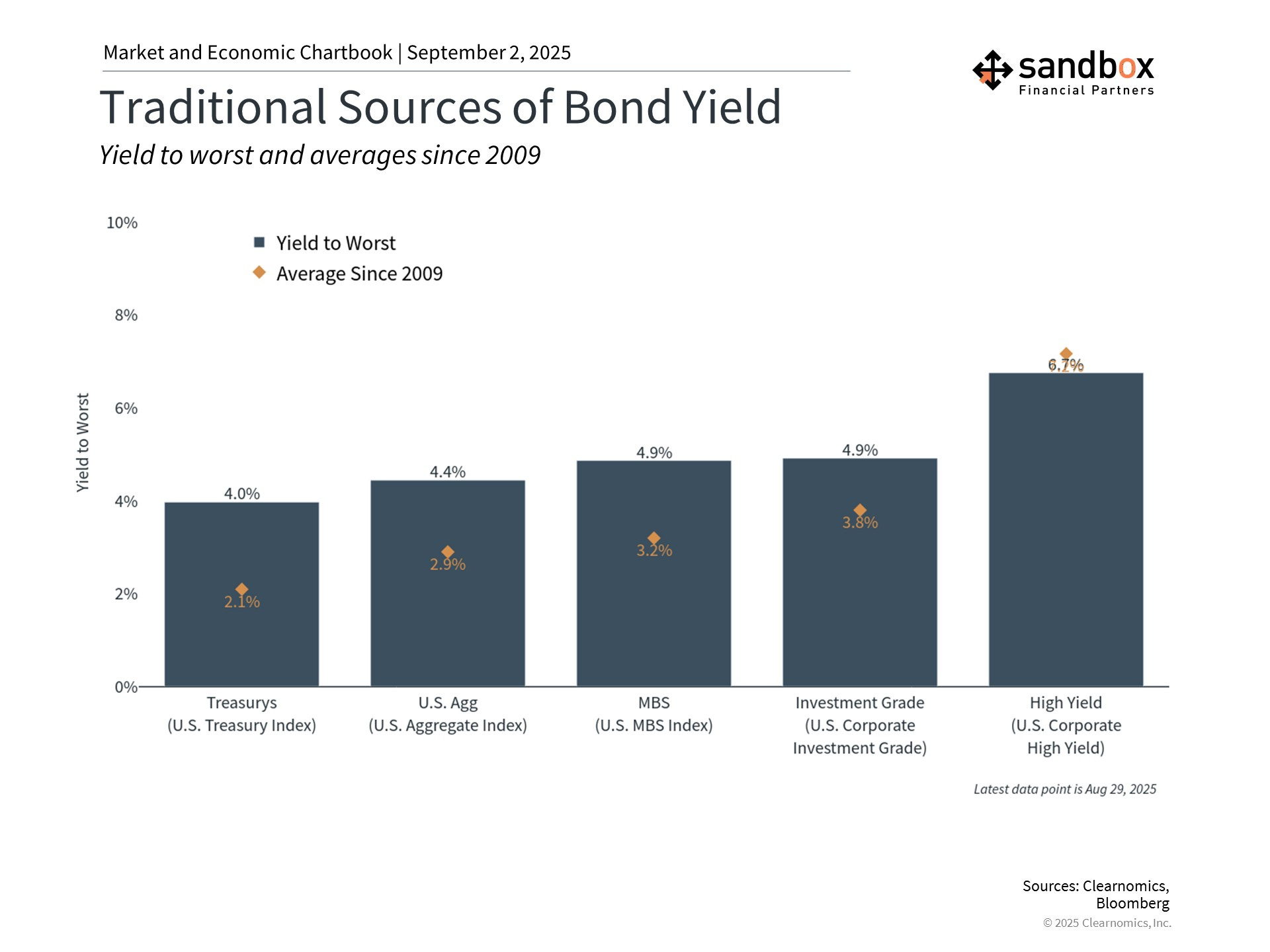

For bonds, lower interest rates boost the prices of existing bonds that were issued at higher yields.

Bond yields have hovered in a narrow range this year, with the 10-year Treasury yield generally fluctuating between 4.0% and 4.5%.

Even if short-term yields decline as the Fed cuts rates, many bond sectors are providing healthy levels of income. The U.S. aggregate bond index is yielding 4.4%, investment grade corporate bonds 4.9%, and high-yield bonds 6.7%. These levels are well above historical averages and support balanced portfolios.

Looking ahead

Congress returns after a month-long break and they will have only three weeks to pass legislation on a budget to avoid a government shutdown on October 1. If Congress cannot come to an agreement on funding, it will look towards the Continuing Resolution (CR) procedure that maintains budgets at their current spending levels.

Fed policy will be under the microscope as the Federal Open Markets Committee (FOMC) next convenes on September 16-17 to set its benchmark interest rate. Following Fed Chair Powell’s speech at Jackson Hole in late August, the market has increased expectations that the central bank will cut rates now that the economy, specifically the labor market, has moved into a position where a rate cut could be appropriate.

Elsewhere, tariffs will continue to garner headlines as a federal court has now challenged President Trump’s policies.

Sources: Clearnomics, FactSet, Bureau of Labor Statistics

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures (click here)

Please see our SEC Registered firm brochure (click here)

Please see our SEC Registered Form CRS (click here)