Bullish signals from a breadth thrust, plus 2024's BIG employment revision, public vs. private, and 🧁 weekend sprinkles 🧁

The Sandbox Daily (8.23.2024)

Welcome, Sandbox friends.

Today’s Daily discusses:

bullish signal from breadth thrusts

2024’s BIG employment revision

stock of private assets vs. public assets

🧁 weekend sprinkles 🧁

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 +3.19% | Nasdaq 100 +1.18% | S&P 500 +1.15% | Dow +1.14%

FIXED INCOME: Barclays Agg Bond +0.46% | High Yield +0.53% | 2yr UST 3.909% | 10yr UST 3.797%

COMMODITIES: Brent Crude +2.37% to $79.05/barrel. Gold +1.17% to $2,546.2/oz.

BITCOIN: +5.87% to $64,079

US DOLLAR INDEX: -0.79% to 100.704

CBOE EQUITY PUT/CALL RATIO: 0.74

VIX: -9.63% to 15.86

Quote of the day

“The distance between insanity and genius is measured only by success.”

- Ian Fleming, Bruce Feirstein

Bullish signal from breadth thrusts

The strongest rallies tend to occur when most stocks are participating. The rationale is that if a few stocks run into trouble, others can propel the indexes higher. The beginning of major moves is often marked by breadth thrusts, or an extremely high percentage of stocks rallying together.

That is why breadth thrusts are the final step of a bottoming process following a market correction, like the declines we experienced earlier this month. Since the recent drawdown was so quick, the bottoming process should be, too. The market bottomed and hit oversold levels on August 5, rallied on August 6, and retested on August 7. Then the market rocketed higher from there.

One significant breath thrust came on August 8 via an 11:1 up day (advancing volume was 11 times greater than declining volume), signaling a strong move off the local lows.

A second breadth thrust fired on August 19, when over 90% of stocks rose above their 10-day moving averages.

As you can see in the data table in the chart above located in the bottom right corner, these breadth thrusts often indicate more gains lie ahead.

Markets are higher 3-months later 67% of the time (28/42) with an average gain of +2.44%, higher 6-months later 76% of the time (32/42) with an average gain of +4.95%, and higher 12-months later 95% of the time (40/42) with an average gain of +10.15% – when 90% of stocks rise above their 10-day moving average.

Source: Ned Davis Research

2024’s BIG employment revision

The biggest news of the week and a report lost among the shuffle – which included a LOT such as the Fed minutes from the July FOMC meeting, Fed Chair Jerome Powell’s Jackson Hole speech today, new and existing homes sales data, and unemployment claims – was the payrolls revision on Wednesday.

The Bureau of Labor Statistics (BLS) published a preliminary benchmark estimate for the revision to payroll growth between April 2023 and March 2024.

The adjustment?

-818k, or -68k jobs per month. Yup, the U.S. economy added 818,00 fewer jobs than originally reported.

Taken at face value, the preliminary estimate suggests that payroll growth averaged 174k jobs/month between April 2023 and March 2024, vs. 242k jobs/month as currently (previously) reported in the payrolls statistics.

This was the biggest revision since 2009 and very large by any measure. For some perspective, here are the most recent revisions:

2018: +43k

2019: -501k

2020 -173k

2021: -165k

2022: +462k

2023: -306k

2024: -818k

The initial public and media response to this BLS announcement was essentially “the BLS is conning us all with fake figures every month”. And sure, it’s true that the revision was large, but the monthly employment reports are notoriously noisy. They get revised every month and then every year as more and more data trickles in.

And yet, the large downward revision shouldn’t be terribly surprising. Anyone reading the data under the hood and studying the various metrics over the last year could tell that the labor market was weakening. Given the imperfect science of these surveys, it’s always wise not to read too much into the initial print.

But, one thing this report did do for me, was reinforce what we already knew: the U.S. labor market is weakening (albeit off historically strong and tight levels) and the probability of rate cuts only ratchets higher with this revision.

Source: Bureau of Labor Statistics, Barron’s, The Conference Board, Goldman Sachs Global Investment Research

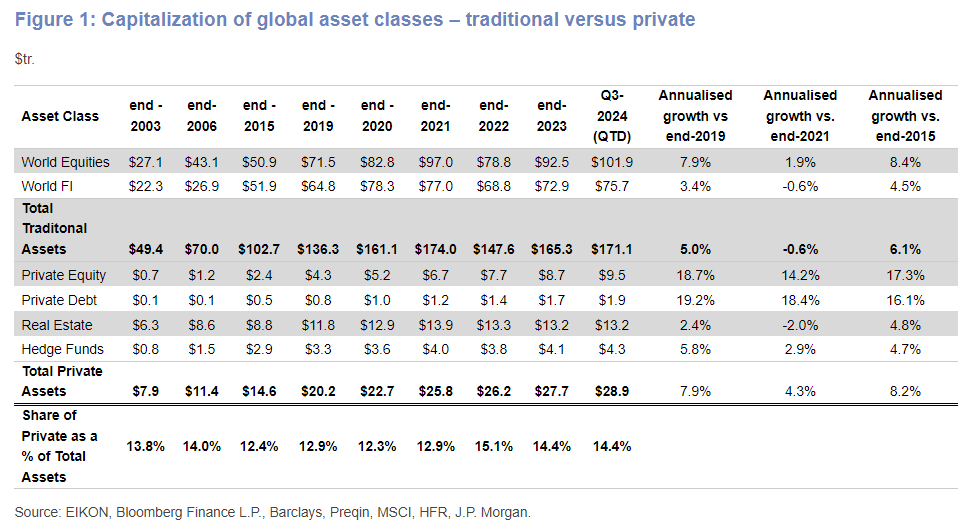

Stock of private assets vs. public assets

The stock of private assets – i.e. private equity, private credit, real estate and hedge funds – has been steadily rising since the turn of the century and continues to grow this year, approaching the $30T mark.

This represents a sizable ~ 15% share of the total asset universe of both private and public assets.

While private assets continue to attract a large amount of investor capital of above $1T each year, inflows have slowed significantly in recent years as higher interest rates have hit private assets such private equity and real estate.

Source: J.P. Morgan Markets

🧁 Weekend sprinkles 🧁

Here are the ideas, sights, and sounds that caught my attention this week – perfect for quiet time over the weekend.

Blogs / Newsletters

OptimistiCallie – How Fear Makes Us Better Investors (Callie Cox)

TKer – There are ‘Rules’ and Then There are ‘Statistical Regularities’ (Sam Ro)

Carson Group – What Tennis Can Teach Us About Investing and Making Your Edge Count (Sonu Varghese)

All Star Charts – Who’s Buying Bonds With Me? (Steve Strazza)

Wall Street Journal – Messing Up the Closest Thing to a Sure Thing in the Stock Market (Jason Zweig)

Hostile Charts – The Volatility Antidote (Larry Thompson)

Podcasts

Lex Fridman – Elon Musk: Neuralink and the Future of Humanity (Spotify, Apple Podcasts, YouTube)

SmartLess – Jason Bateman, Sean Hayes, and Will Arnett host guest Jared Leto (Spotify, Apple Podcasts)

New Hampshire Public Radio – Bear Brook: A True Crime Story (Spotify, Apple Podcasts)

Movies

Twisters – Glen Powell, Daisy Edgar-Jones, Anthony Ramos (IMDB, YouTube)

A Star is Born – Bradley Cooper, Lady Gaga, Sam Elliott, Andrew Dice Clay (IMDB, YouTube)

Music

Post Malone feat. Tim McGraw – Wrong Ones (Spotify, Apple Music)

Mac McAnally – Once in a Lifetime (Spotify, Apple Music)

Brand New - Millstone (Spotify, Apple Music)

Culture

Hard Knocks: Training Camp with the Chicago Bears (YouTube, HBO)

SatPost – How Does Michelin Guide’s Business Work (Trung Phan)

Books

Scott Galloway – The Algebra of Wealth (Amazon)

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.