Buyers of U.S. Treasurys, plus the week in review

The Sandbox Daily (10.13.2023)

Welcome, Sandbox friends.

Happy Friday, the 13th!

Today’s Daily discusses:

who will buy U.S. Treasurys

a brief recap to snapshot the week in markets

But first, the sunsets in Annapolis are just incredible:

Let’s dig in.

Markets in review

EQUITIES: Dow +0.12% | S&P 500 -0.50% | Russell 2000 -0.84% | Nasdaq 100 -1.24%

FIXED INCOME: Barclays Agg Bond +0.43% | High Yield -0.08% | 2yr UST 5.058% | 10yr UST 4.617%

COMMODITIES: Brent Crude +5.69% to $90.89/barrel. Gold +3.17% to $1,928.5/oz.

BITCOIN: +0.36% to $26,902

US DOLLAR INDEX: +0.07% to 106.672

CBOE EQUITY PUT/CALL RATIO: 0.80

VIX: +15.76% to 19.32

Quote of the day

“Being right may be a necessary condition for investment success, but it won’t be sufficient. You must be more right than others… which by definition means your thinking has to be different.”

- Howard Marks, Oaktree Capital

Who will buy U.S. Treasurys?

The U.S. Treasury’s barrage of bill issuance is starting to expose some cracks in the federal budget funding space. Concerns over the fiscal position of the U.S. government have been one driver of the volatility in the Treasury market.

Remember for a moment the Treasury spooked analysts at the end of July by raising its borrowing estimate for the 3rd quarter to roughly $1 trillion, more than $270 billion above its forecast. This caused further pressure on rates that were already on the move higher.

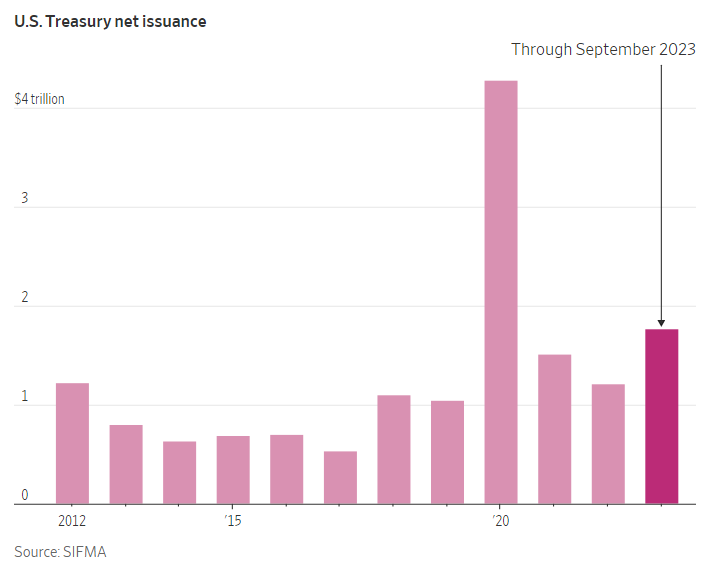

Year-to-date through September, more than $1.76 trillion of Treasury bonds have been issued on a net basis – higher than in any full year in the past decade, excluding 2020’s pandemic surge.

This brings the conversation to the supply/demand mismatch that is causing concerns for many Fed watchers.

With the Fed no longer an active buyer of Treasurys (transitioning from a net buyer to net seller), we are witnessing a vacuum in demand from a key source.

Obviously, this intensifies the spotlight on foreign investors, who own the largest share of outstanding of Treasury bonds (30%):

A key issue here is the depressed demand from America’s biggest foreign creditors, which will likely keep longer-term rates elevated for some time to come.

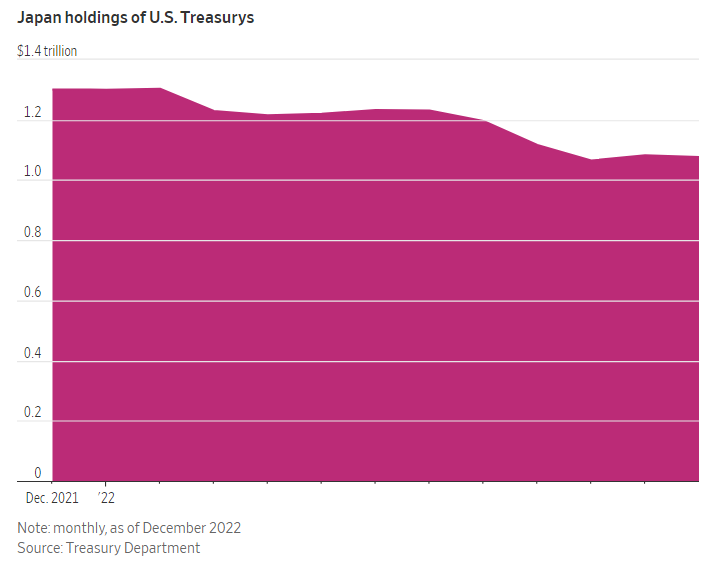

One example is Japan, the largest foreign holder of Treasurys owning $1.1 trillion worth. But, the Bank of Japan – like many other economies – are experiencing higher local market yields themselves, providing local investors less reason to buy U.S. debt.

So, who becomes the next incremental buyer of Treasurys?

Since the pandemic, the biggest buyers have been state/local governments, the Fed, and the banks.

But, with all three cutting back in recent quarters on their buying and/or reducing their holdings, the burden is falling down the chain to households, pensions, and the rest.

Source: Wall Street Journal, Ned Davis Research, Goldman Sachs Global Investment Research

The week in review

Talk of the tape: Rates remain the market's primary focus, although Treasury yields have softened somewhat after some more dovish Fedspeak arguing the recent big Treasury yield backup might make it less urgent for the Fed to hike further. A mixed September CPI report and a 3rd-straight disappointing Treasury auction were headwinds on the Peak Fed narrative. A lot of attention on today's money center bank earnings as the unofficial launch of the Q3 earnings season, which is expected to see a slowdown of earnings declines.

Soft-landing expectations underpin the bullish narrative. The potential for a return to positive earnings growth in Q3, record amount of money market assets on the sidelines, and favorable seasonality in Q4 flagged as other bullish drivers. Consumer resilience, although showing some signs of fatigue, continues to be a higher-profile bright spot.

Bearish talking points, which have gained traction over the last couple months, revolve around the upward pressure on rates, liquidity headwinds, and the lagged effects of policy tightening (19 months now). Geopolitical concerns, oil markets, and Congressional bickering all cited as near-term overhangs as the market decides what to make of their implications. Narrow market leadership a constant talking point among the bears.

Stocks: The major averages ended the week mixed, although some of the recent weakness has subsided as upside momentum in interest rates faded. According to the most recent AAII Sentiment Survey, the percentage of bullish investors jumped from 30.1% to 40% – above the historical long-term average of 37.5% – while bearish investors reversed three straight weeks of increases. Comments from various Fed officials throughout the last couple of weeks suggest the tighter financial conditions may reduce the need for further rate hikes in the short-term.

Bonds: The Bloomberg Aggregate Bond Index ended the week higher as investor concerns over the Fed’s higher-for-longer policy subsided. While spreads are still below historical averages, the speed with which the spread widening has taken place is a yellow flag that many are intently watching.

Commodities: Commodities had a mostly positive week amid the recent geopolitical crisis in the Middle East. The International Energy Agency this week described market conditions as “fraught with uncertainty” but stated that the Israel-Hamas war had not yet directly impacted physical energy supplies. Gold and silver also caught a bid as investors look to safe havens given the geopolitical tensions.

Source: Dwyer Strategy, LPL Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

beautiful sunset - Annapolis looks amazing at night!