Cash Rules Everything Around Me (Or Does It?)

The Sandbox Daily (1.6.2025)

Welcome, Sandbox friends.

As one year comes to a close and another takes shape over the horizon, it’s a fitting moment to pause and reflect on the many experiences that have impacted me, shaped my perspective on life and markets, and sharpened my resilience to the trials and tribulations we all face on a daily basis.

As I turn the page to a fresh start in 2025, I carry both gratitude for where I’ve been and optimism for all the promise that lies ahead. A heartfelt thanks to my family, friends, and colleagues, as well as all of you for joining The Sandbox Daily here each week. Sending my best to everyone in the coming year!

After two weeks off with family and friends for the holidays, I am excited to be back and drop my notes into your inbox.

Today’s Daily discusses:

cash is not king

Let’s dig in.

Blake

Markets in review

EQUITIES: Nasdaq 100 +1.09% | S&P 500 +0.55% | Dow -0.06% | Russell 2000 -0.08%

FIXED INCOME: Barclays Agg Bond -0.10% | High Yield +0.18% | 2yr UST 4.271% | 10yr UST 4.624%

COMMODITIES: Brent Crude -0.38% to $76.22/barrel. Gold -0.32% to $2,646.2/oz.

BITCOIN: +3.87% to $101,813

US DOLLAR INDEX: -0.64% to 108.259

CBOE TOTAL PUT/CALL RATIO: 0.81

VIX: -0.56% to 16.04

Quote of the day

“Twenty years from now you will be more disappointed by the things you didn’t do than by the things you did.”

- Mark Twain

Cash Rules Everything Around Me (Or Does It?)

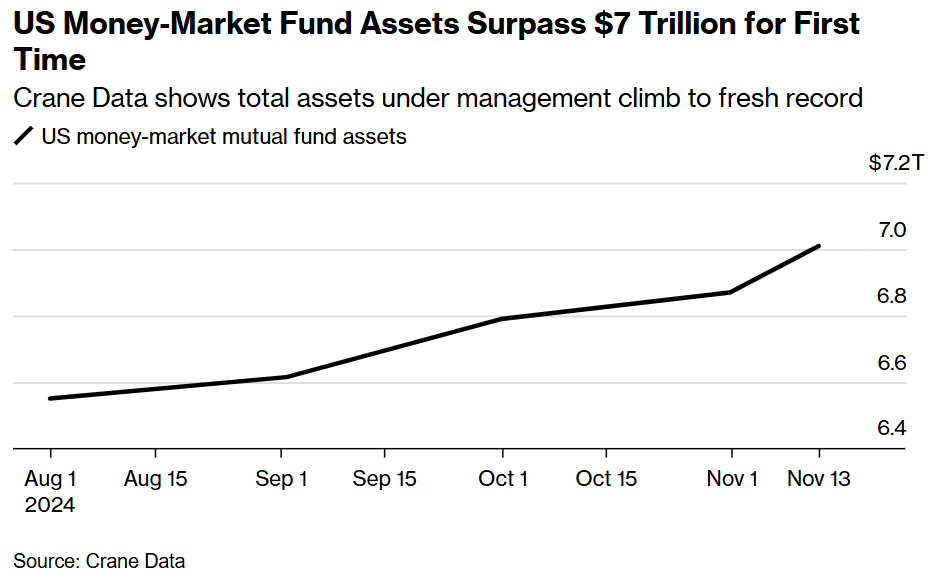

U.S. money market funds have racked up more than $7 trillion in assets under management (AUM) as of 2024 year-end per Crane Data, a milestone for an industry that hasn’t been in vogue since Matchbox 20 and Nelly were charting number one singles like Push and Ride Wit Me.

For the less informed, money markets are a type of mutual fund that invests in short-term high-quality debt securities, cash, and cash equivalents. They are considered one of the lowest, if not the lowest, risk option for investors and are often used to serve short-term goals such as a home downpayment, wedding expense, or unexpected life event.

Easy access, daily liquid, almost zero volatility, and yield on your savings. That’s the gist.

The Wall Street parlance “Cash On The Sidelines” via money market holdings can indicate a safety blanket for investors, money for a rainy-day fund, or firepower for investment during a market correction (assuming you have the mental fortitude to plow into stocks during a 10% or 20% market correction).

Strategists often suggest a huge pool of money awaits to flood the market at any given moment and send asset prices higher by “buying the dip.”

Cash On The Sidelines can also mean missed opportunities. The intermediate to long-term costs of missed opportunities by staying in cash could put an investor’s long-term goals at risk.

Take 2023 and 2024 for example. While cash earned ~5% annualized, equity markets show the real opportunity cost by overstaying your welcome in cash. Missing big gains by not participating in strong bull runs can have damning effects on the probability of successfully meeting various goals in your financial plan.

Perhaps it wasn’t best to “T-Bill and Chill” after all.

Regret aversion is a relevant behavioral input here.

The big question is what to do with the cash?

Human psychology can’t help but immediately go to a dark place suggesting that if I buy the market now, my account will immediately drop. This instinctual fear of regret leads to indecision and suboptimal outcomes because humans have the tendency to avoid making decisions that could lead to future regret and disappointment.

Sitting in cash is supposed to be a placeholder, not an all-in investment strategy. Of course, at risk of stating the obvious, each investor has its own unique situation of return objectives, risk capacity and tolerance, time horizon, tax situation, etc etc.

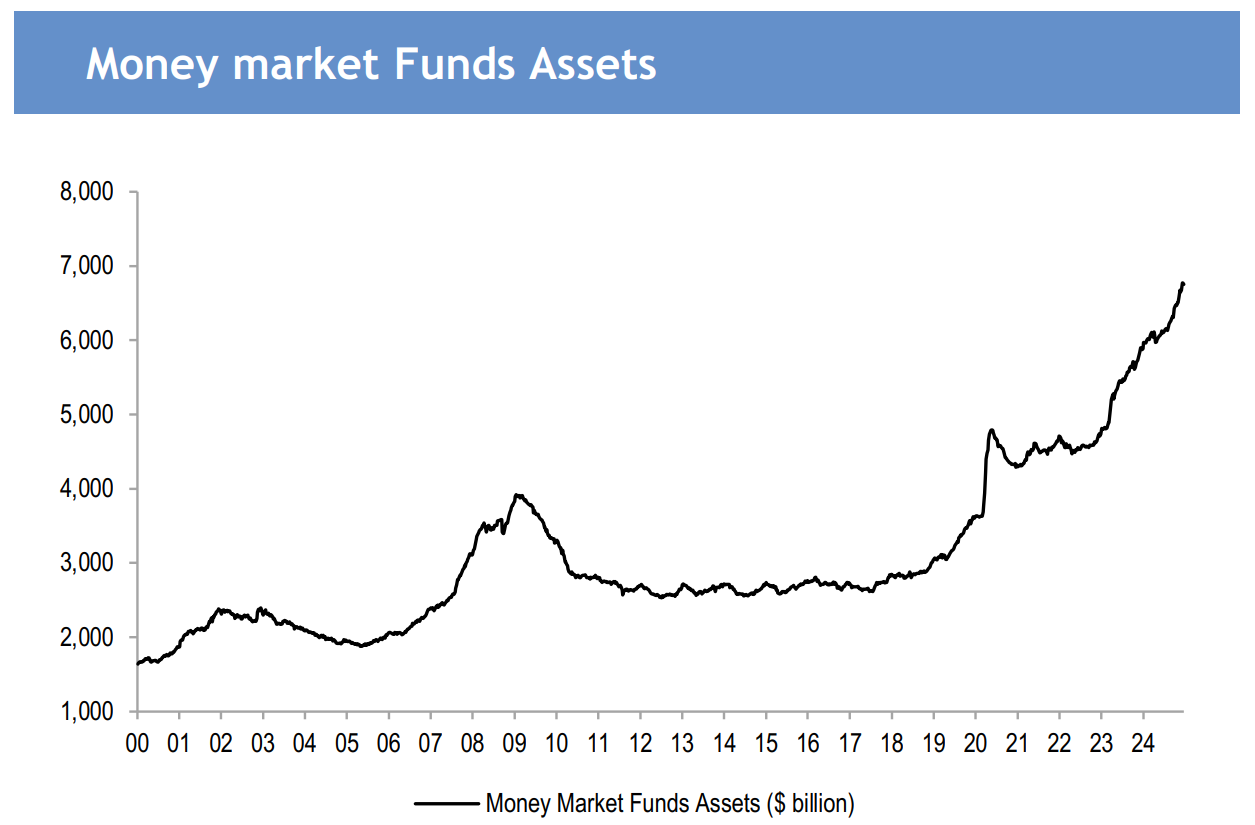

2024 was supposed to be the great exodus for money market funds. The Federal Reserve began its interest rate cutting cycle, while the rally in stocks broadened out during year 2 of the bull market off the October 2022 low.

The problem?

Nobody from the stockpile of money market funds got the memo. Investors are continuing to plow cash into money market funds, despite no discernible reason to do so.

In 2008-2009, investors piled into money market funds as the mortgage crisis eviscerated stocks into oblivion.

In the next major crisis of 2020, the world was reeling from a once-in-a-lifetime global health pandemic.

The tops for each catastrophe are self-evident in the chart below.

But, once the economy and market moved passed each clearing event, flows stabilized and the total stock of cash in money funds leveled off.

What is less clear in 2025 is why this asset class continues to march higher to the tune of a meme coin or Bored Ape Yacht Club digital token.

As rates slide to 4.0%-4.5% and lower, retail investors continue to allocate towards cash. With signs mounting that the Federal Reserve may not cut benchmark rates much more from here, Wall Street is now predicting that Americans aren’t going to suddenly pivot away from cash anytime soon.

What’s more, 75% of central banks around the world are in proactive easing cycles, labor markets remain resilient to higher rates, and earnings growth is hooking higher. So, the backdrop for the market seems quite sanguine; dynamics are not screaming for imminent disaster and a flight to quality.

And yet, like most things in life, everything is relative.

Sure, $7 trillion in money markets is a staggering figure worthy of everyone’s attention. That is, until you measure the stock of money market assets against the size of the U.S. stock market as measured by the S&P 500, which shows balances are quite stable.

Even as the nominal amount of cash regularly hits new record highs, the increase provides us the illusion that there’s an unprecedented amount of money “on the sidelines,” when this supply seems quite small relative to many other market-based measures.

While cash in absolute terms has grown, households have shifted even more aggressively into equities, effectively underscoring the appetite for risk assets remains event stronger.

As a result, cash allocations are at/below long-term average levels while stock allocations are at all-time highs.

Inertia is the tendency for an object to resist any change in motion. What will be the catalyst to jumpstart Cash On The Sidelines?

Some of the most uncertain times – Fed rate hikes, persistent inflation spikes, disappointing earnings – are important market inflection points.

In hindsight, these events are opportune times to reallocate cash in portfolios and align them to their objectives.

Yet, with no meaningful market event currently disrupting the status quo, cash balances remain robust. AND sticky.

Sources: J.P Morgan Markets, Bloomberg, Aptus Capital Advisors, Richard Bernstein Advisors

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures at the Sandbox Financial Partners website: