Central bank policy beginning to diverge

The Sandbox Daily (6.16.2026)

Welcome, Sandbox friends.

Today’s Daily discusses:

central bank policy beginning to diverge

Let’s dig in.

Blake

Markets in review

EQUITIES: Dow +0.64% | S&P 500 -0.57% | Russell 2000 -0.87% | Nasdaq 100 -1.89%

FIXED INCOME: Barclays Agg Bond +0.12% | High Yield -0.01% | 2yr UST 4.439% | 10yr UST 4.941%

COMMODITIES: Brent Crude +0.75% to $79.55/barrel. Gold +0.27% to $4,355.8/oz.

BITCOIN: -1.51% to $65,596

US DOLLAR INDEX: +0.01% to 99.54

CBOE TOTAL PUT/CALL RATIO: 0.89

VIX: +1.30% to 16.41

Quote of the day

“If you have a problem with me, text me. And if you don’t have my number, you don’t know me well enough to have a problem with me.”

- Christian Bale

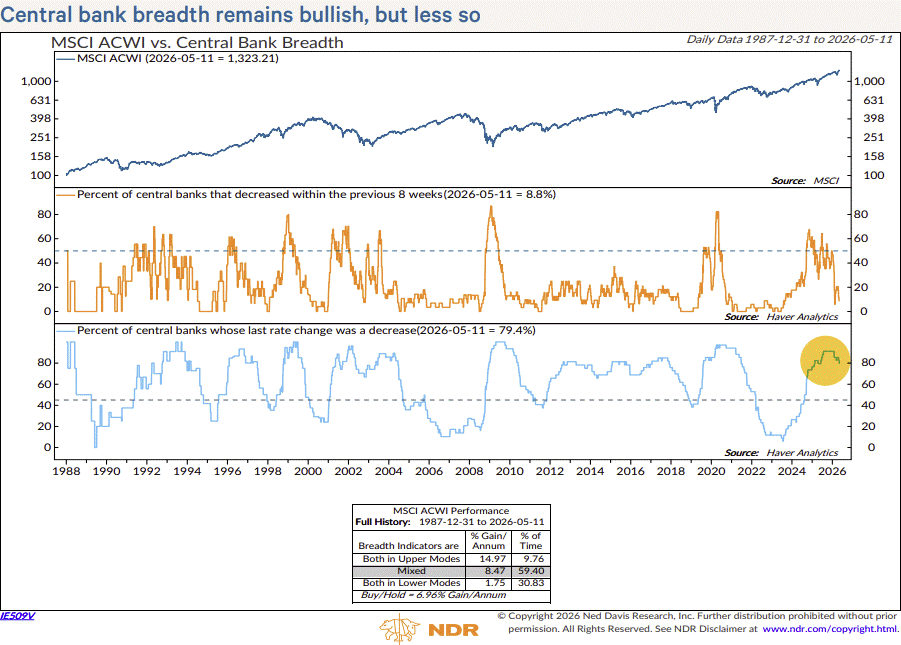

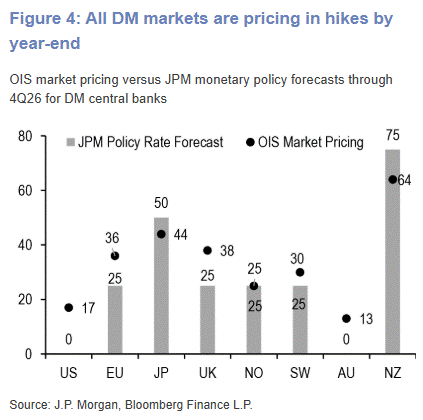

Central bank policy pivoting away from easing bias

Global central bank policy remains broadly supportive of risk assets, even as inflation risks tied to the Iran conflict have narrowed the margin for error.

A majority of central banks are still in easing cycles, a backdrop that has historically favored stocks.

However, persistent commodity-driven inflation could push certain policymakers around the global toward selective tightening over the next 6-12 months.

With interest rate policy now more influential than balance sheet management, market outcomes will increasingly depend on whether inflation pressures prove temporary or require coordinated tightening.

The Fed is expected to remain on hold for now, supported by stable growth and anchored inflation expectations. I’d expect the Fed to remove its easing bias and turn neutral at tomorrow’s June meeting, and then stay on hold for the balance of the year. There remains a non-zero chance that the Fed itself may deliver a rate cut by year-end.

Elsewhere, a few central banks have already shifted course and more may follow.

The European Central Bank (ECB) and Bank of England (BoE) face greater pressure from energy-driven inflation and may each deliver one rate hike despite weaker growth. The Bank of Japan (BoJ) is continuing its gradual normalization, supported by stronger wages and inflation dynamics.

Across Emerging Markets, the easing trend largely remains intact, with China likely to ease further and other economies pausing or adjusting based on Fed policy and inflation trends.

Overall, while policy divergence is increasing, the global backdrop still leans supportive for equities, provided inflation does not force a broader shift toward tightening.

Chart sources: Ned Davis Research, J.P. Morgan

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures (click here)

Please see our SEC Registered firm brochure (click here)

Please see our SEC Registered Form CRS (click here)