ChatGPT and the week in review

The Sandbox Daily (1.20.2023)

Welcome, Sandbox friends.

Today’s Daily discusses the ChatGPT language model and a brief recap to snapshot the week in markets.

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 +2.86% | S&P 500 +1.89% | Russell 2000 +1.69% | Dow +1.00%

FIXED INCOME: Barclays Agg Bond -0.41% | High Yield +0.20% | 2yr UST 4.177% | 10yr UST 3.482%

COMMODITIES: Brent Crude +1.74% to $87.66/barrel. Gold +0.22% to $1,928.2/oz.

BITCOIN: +7.57% to $22,571

US DOLLAR INDEX: -0.06% to 101.992

CBOE EQUITY PUT/CALL RATIO: 0.76

VIX: -3.27% to 19.85

ChatGPT

ChatGPT, the AI model which engages in conversational dialogue, has taken the internet by storm – with Silicon Valley salivating at its future potential. It was developed by OpenAI, a tech research company dedicated to ensuring that artificial intelligence benefits all of humanity. The "GPT" in ChatGPT refers to "Generative Pre-training Transformer," referring to the way that ChatGPT processes language.

Microsoft is reportedly preparing for its largest startup investment in history: a $10 billion stake in OpenAI that could value the research lab at $29 billion. A bet this big on the free chatbot shows how much interest has developed into artificial intelligence. Microsoft’s AI ambitions go beyond just integrating ChatGPT know-how into its own search engine, Bing. The company wants to incorporate OpenAI’s tools in its Office suite.

Here is an example of how the tool works, with Taylor Swift singing a love sone about the volatile stock market:

Source: ChatGPT

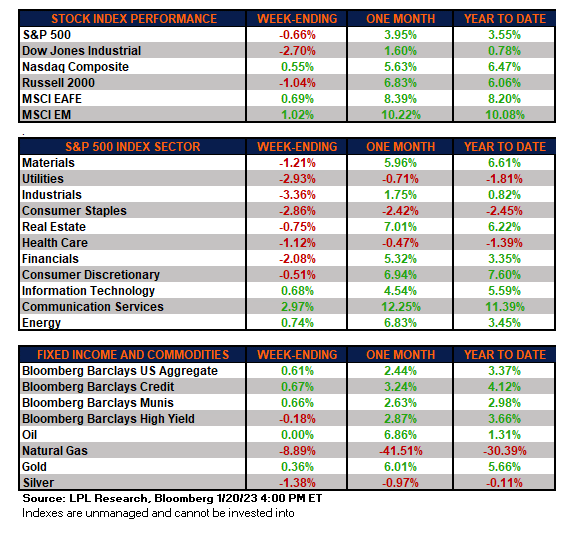

The week in review

Talk of the tape: The recent ramp in soft-landing expectations was dented by some softer U.S. economic data, such as retail sales and existing home sales. Disappointing earnings/guidance also playing into growth concerns (beat rates sluggish despite the lower bar), as are corporate layoff announcements, which initially seemed to be spun in favor of economic normalization and profit margin protection.

At the same time, there’s no letup in the Fed's higher-for-longer messaging, while ECB officials have also pushed back against speculation of a near-term slowdown in the pace of easing. Some thoughts around the street suggest the recent bounce may be running out of room given outsized short covering and an uptick in positioning and sentiment indicators. Valuation and technicals are also increasingly flagged as overhangs.

Elsewhere, debt ceiling concerns have flared up with no evidence either side prepared to back down.

Stocks: The major markets mostly finished lower, reversing two straight week of gains, although stocks finished the week on a strong, positive note. Market participants were concerned about earnings quality as top and bottom-line beat rates were light, despite lower estimates. In addition, steadfast Federal Reserve (Fed) policy on interest rates and debt ceiling concerns weigh on investor’s minds. Emerging markets finished the week on a positive note as Hong Kong and Chinese stocks outperformed given positive reopening/policy support dynamics.

Bonds: The Bloomberg Aggregate Bond Index finished the week higher as yields declined on the latest evidence of easing price pressures. In addition, high-yield corporate bonds, as tracked by the Bloomberg High Yield index, finished the week higher, following their equity counterparts.

This week, investors flooded municipal bond funds with the biggest influx of cash in more than a year, as demand returned to the $4 trillion state and local government debt market. Municipal bond funds garnered $2 billion in the week ended Wednesday, the largest inflow since July 2021, according to Refinitiv Lipper US Fund Flows data.

Commodities: Oil and natural gas prices finished the week mixed as both commodities moved in opposite directions for the second straight week. Oil moved higher given an improving economic backdrop in China. European natural gas prices continue to fall, reaching prices below levels last seen since before the Russia-Ukraine conflict amid warmer-than-anticipated weather and storage facility inventories at record seasonal highs. The major metals, including gold, silver, and copper finished the week mixed.

Source: Dwyer Strategy, LPL Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.