China's growth tailwind, plus bearish sentiment, affordable homes, the consumer, and the Super Bowl hangover

The Sandbox Daily (2.13.2023)

Welcome, Sandbox friends.

Today’s Daily discusses the boost to global growth from China’s zero-Covid pivot, time to fade the bears, the decreasing stock of affordable homes, the health of the American consumer, and the Super Bowl hangover.

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 +1.60% | Russell 2000 +1.16% | S&P 500 +1.14% | Dow +1.11%

FIXED INCOME: Barclays Agg Bond +0.30% | High Yield +0.25% | 2yr UST 4.517% | 10yr UST 3.703%

COMMODITIES: Brent Crude -0.46% to $85.99/barrel. Gold -0.57% to $1,863.9/oz.

BITCOIN: -1.47% to $21,629

US DOLLAR INDEX: -0.33% to 103.283

CBOE EQUITY PUT/CALL RATIO: 0.69

VIX: -0.93% to 20.34

China’s reopening is poised to boost global growth

China’s reopening from Covid-19 restrictions will not only accelerate the country’s economic recovery, but it will also boost global economic growth.

Due to the faster-than-expected rate of reopening, economists at Goldman Sachs now forecast China’s GDP to grow by +6.5% in 2023. On top of that, the reopening—and the recovery of Chinese domestic demand—could raise global GDP by +1% by the end of 2023.

China’s reopening will impact global growth through three direct channels:

Increased domestic demand: Reopening is expected to lift core goods exports among China’s trade partners. The reopening should increase domestic demand by up to 5% in China. Unsurprisingly, this is welcome news for China’s regional neighbors, as Asia-Pacific economies export more goods to China than many Western economies.

International travel: China’s exit from zero-Covid policy should drive a recovery in demand for foreign services, particularly for international travel. Before the pandemic, China was a net importer of travel services from most economies. And while this took a hit during tight Covid restrictions, a normalization in travel patterns should lead China’s travel trade deficit to increase and boost foreign GDP.

Commodity demand: China is a dominant driver of commodities demand, with market shares in excess of 50% for some commodities. As such, China’s reopening will likely boost commodities demand and prices, particularly for oil. Commodity strategists estimate that Chinese oil demand could recover by at least 1 million barrels per day, boosting Brent oil prices by roughly $15 per barrel. If international travel recovers more rapidly, these prices could rise even further.

“The clear risk from reopening is that stronger growth could lead inflation to surprise to the upside later this year. As a string of mostly downside inflation surprises have driven an easing in global financial conditions and enabled central banks to slow the pace of rate hikes in recent months, a larger inflation impulse from reopening may force central banks to hike rates further than markets currently expect to keep growth below potential and remain on track to tame inflation.”

Source: Goldman Sachs Global Investment Research

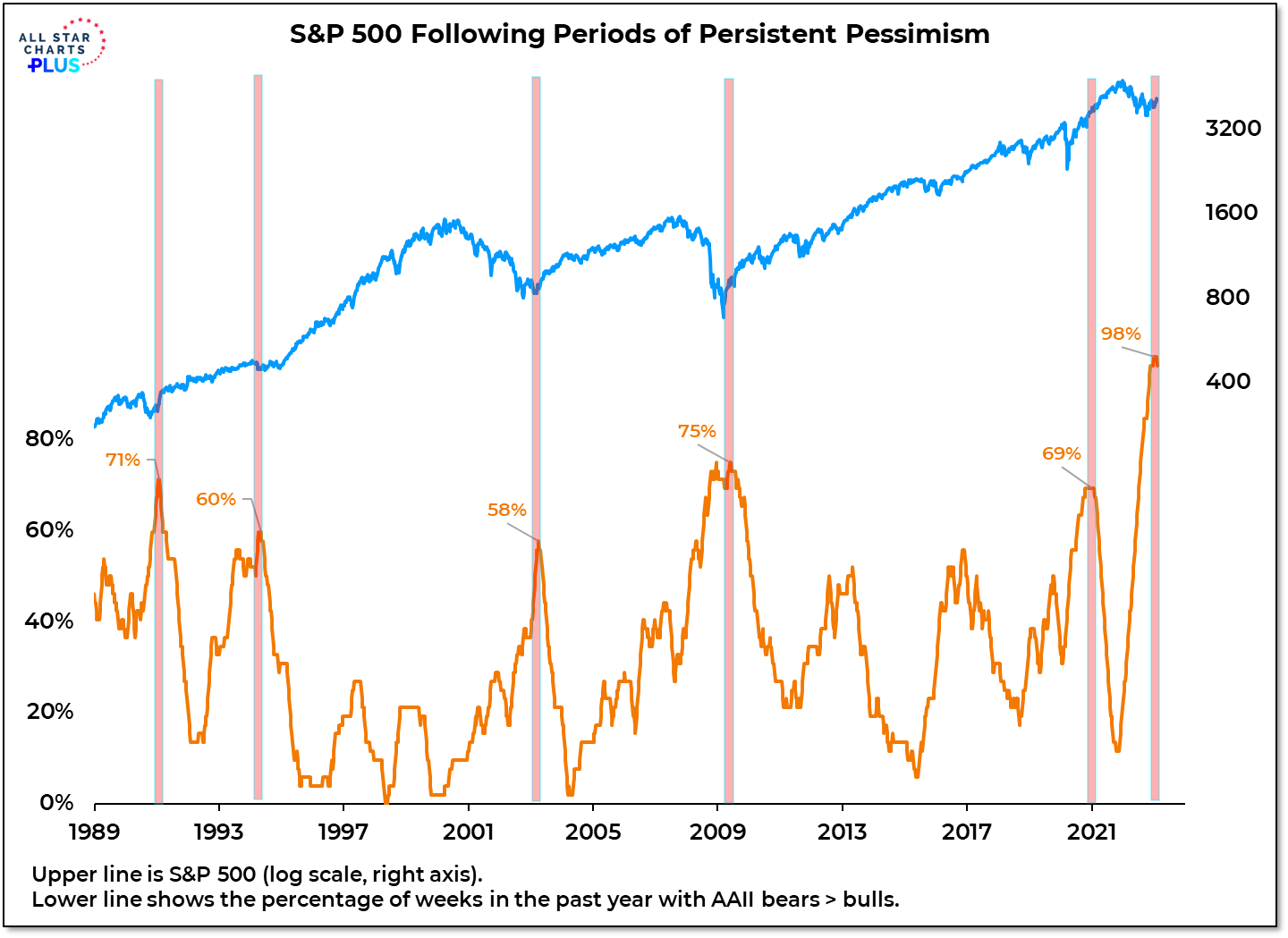

Fade the bears?

We use sentiment data as a contrarian indicator. Yet while optimism begins to increase, the more important point is that it’s turning away from levels of extreme pessimism.

When we look at weekly survey results from the American Association of Individual Investors (AAII), bears have outnumbered bulls for 98% of the weeks over the trailing twelve months. That’s the longest stretch for the bears in over thirty years.

Any increase in the share of bulls at this point would be a positive development for stocks, as extreme pessimism begins to unwind.

Inflection points in sentiment such as this often support sustained rallies for the stock market. Just notice how key market lows over the years coincide with peaks in this indicator.

As such, the contrarian move today suggests fading the bears, not the bulls. It appears the unwind could already be underway, as last week was the first week of bulls outnumbering bears after 44 consecutive weeks of the opposite.

Source: All Star Charts

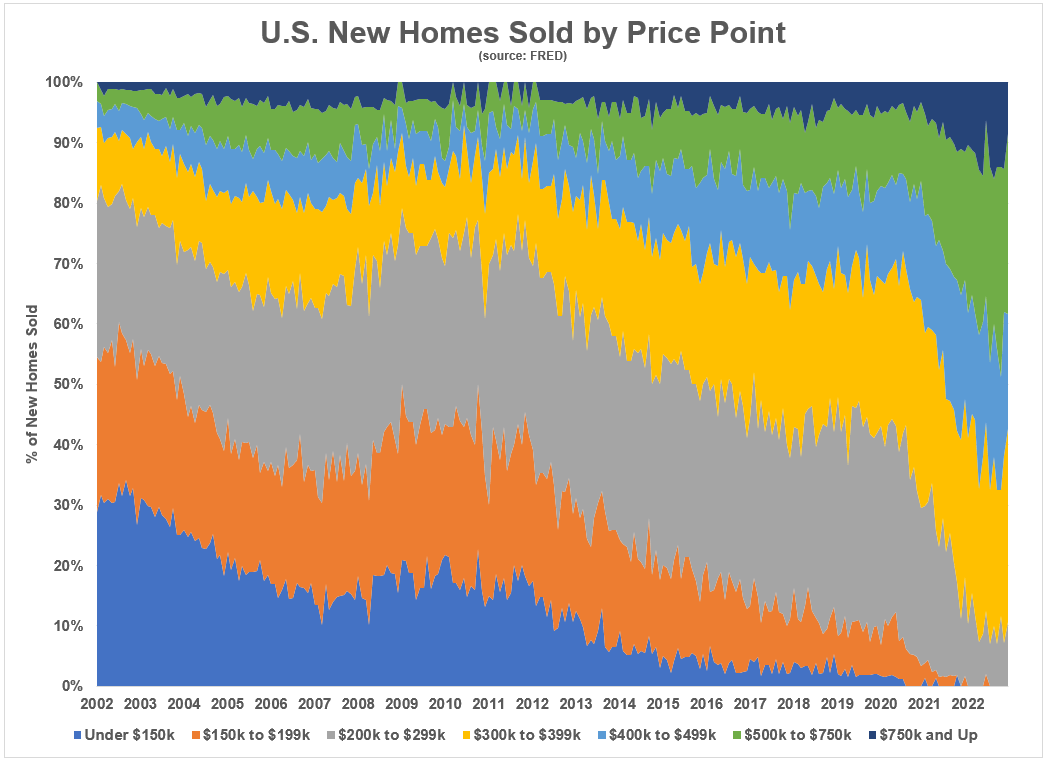

Where are all the affordable homes

The housing stock once called the “starter home” seems to be all but gone.

New homes priced below $200k are now 0% of the market. They were 40% of the market one decade ago.

Meanwhile, $500k+ homes have grown from 17% of the market to 38% of the market during Covid.

The Federal Reserve has new home price data going back to 2000 and it’s not only the $200k and under segment that has fallen off a cliff. New homes going for $300k or less now make up just 11% of the pie, down from 80% of all new home sales in the year 2000.

Here is a look at the same data for new homes but instead of looking at the proportion of homes sold by price point, this shows the actual number of new homes sold over time:

The transition away from the traditional starter home – perfect for many millennials looking to become 1st-time home buyers – underpins many structural changes in the housing market since 2000. Overbuilding for a decade led to a decade of underbuilding. The median (desired) home size has grown as consumer preferences have shifted over time: more bathrooms, more bedrooms, more common areas, more storage, and bigger garages. Then add recent market dynamics like inflated home prices and a doubling in the mortgage rate, and we find a market that is pricing out many potential homebuyers because the housing market is not what it once was.

Source: Federal Reserve Bank of St. Louis, A Wealth of Common Sense

Health of the U.S. consumer

After cleaning up the personal balance sheet during the early days of the pandemic, we have seen a reversal in both credit card loan data and the U.S. personal savings rate.

The personal saving rate has crashed to well below long-term trend (asset side of the equation, down), while credit card balances have reverted back to trend and sit above pre-pandemic levels (liability side of the equation, up). When viewed together, this is not the sign of a healthy consumer.

One key indicator to monitor in light of these developments are delinquencies. The New York Fed releases a quarterly report on household debt and credit to monitor the health and quality of the consumer across an array of traditional loan types, including mortgages, auto loans, students loans, HELOCs and credit cards.

Tracking aggregate delinquency rates shed light on how consumers are responding to post-pandemic trends and cyclically high inflation. Following two years of historically low delinquency, many expect the share of debt newly transitioning into one stage or another of delinquency status to start increasing. The risk that many are fearing are quick and unexpected jumps in delinquency, such what we experienced from 2007-2010 as the Great Financial Crisis stressed millions of American households.

For now, a tight labor force acts as one antidote to this developing story.

Source: Federal Reserve Bank of New York, Freedom Day Solutions

Super Bowl hangover

Roughly 1 in 5 employed Americans say they will report to work late or plan to miss work entirely the Monday after the Super Bowl.

Some 18.8 million Americans are expected to miss work today in what is widely considered one of the most unproductive days on the calendar, according to a recent poll by the Workforce Institute at UKG.

Absent or distracted workers will cost the economy some $6.5 billion this Super Bowl Monday. On the positive side, legal Super Bowl betting was estimated to reach $16 billion.

Source: Workforce Institute at UKG

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.