Chinese stocks pounded, plus stock-bond correlation and leading economic indicators

The Sandbox Daily (1.22.2024)

Welcome, Sandbox friends.

Today’s Daily discusses:

sharp decline in Chinese stock market accelerates

positive stock-bond correlation

leading economic indicators (LEI) index shows early signs of stabilization

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 +2.01% | Dow +0.36% | S&P 500 +0.22% | Nasdaq 100 +0.09%

FIXED INCOME: Barclays Agg Bond +0.18% | High Yield +0.08% | 2yr UST 4.393% | 10yr UST 4.107%

COMMODITIES: Brent Crude +1.62% to $79.83/barrel. Gold -0.31% to $2,023.1/oz.

BITCOIN: -4.37% to $39,947

US DOLLAR INDEX: +0.05% to 103.339

CBOE EQUITY PUT/CALL RATIO: 0.59

VIX: -0.83% to 13.19

Quote of the day

“Far more money has been lost by investors preparing for corrections or trying to anticipate them than has been lost in corrections themselves.”

- Peter Lynch, Former PM of the Fidelity Magellan Fund

Sharp decline in Chinese stocks accelerates, roils local investors

The Hang Sang Index, with 82 constituent companies representing ~60% of the market capitalization of the Hong Kong Stock Exchange, finds itself without a buyer in sight – now down -12% year-to-date (in just 15 trading days) and suffering a >50% drawdown in total.

Currently trading at ~10x forward P/E – on par with previous troughs reached over the last 40 years – the Hang Sang is the worst performing major index in Asia and on course for its biggest monthly drop since October 2022.

The steep losses in Hong Kong, where some of China’s most influential and innovative firms are listed and Beijing’s interference is less felt, paint a more worrisome picture of global investor sentiment toward the world’s No. 2 economy.

Part of the selloff was on disappointment that Chinese commercial lenders held their benchmark lending rates unchanged Monday, with some investors interpreting the hold – after the People’s Bank of China (PBOC) refrained from trimming borrowing costs last week – as another sign that Beijing isn't moving on stimulus measures to help prop up the Chinese economy.

Beijing has been reluctant to flood the economy with monetary stimulus despite the nation experiencing its longest deflationary streak since the late 1990s, the ongoing and deepening housing slump, and an ageing population in decline.

The confluence of these major headwinds are contributing to massive underperformance against other equities.

Source: David Ingles, Bloomberg, Chartr, Goldman Sachs Global Investment Research

Positive stock-bond correlation challenges traditional diversification method

Over the past two years, the equity-bond correlation – which is a statistical measure that expresses the extent to which two variables are linearly related – has been mostly positive.

This shift in bond-equity correlation to positive territory has been posing a significant challenge for multi-asset investors, in particular risk-parity strategies and multi-asset strategies (such as the 60-40 portfolio), because stock and bond prices are moving up and down in tandem.

Diversification tells us this poses a risk to our portfolios because bonds are no longer providing an effective hedge to equities. When one assets class zigs, we often want the other asset class to zag.

The current bond-equity correlation backdrop was the norm prior to 2000, when it was more typical for this correlation to be positive.

One potential structural explanation for the change in this relationship from the late 1990s onwards was the emergence of an implicit equity market backstop by central banks, i.e. the so-called “Fed put”, or at least the perception among market participants of the Fed coming to the stock market’s rescue. A more persistent fading of this central bank backstop in the current juncture, perhaps due to heightened uncertainty over the inflation outlook, could thus prolong the past two years’ phase of positive bond-equity correlation and make it more structural.

Source: Potomac Fund Management, Investopedia

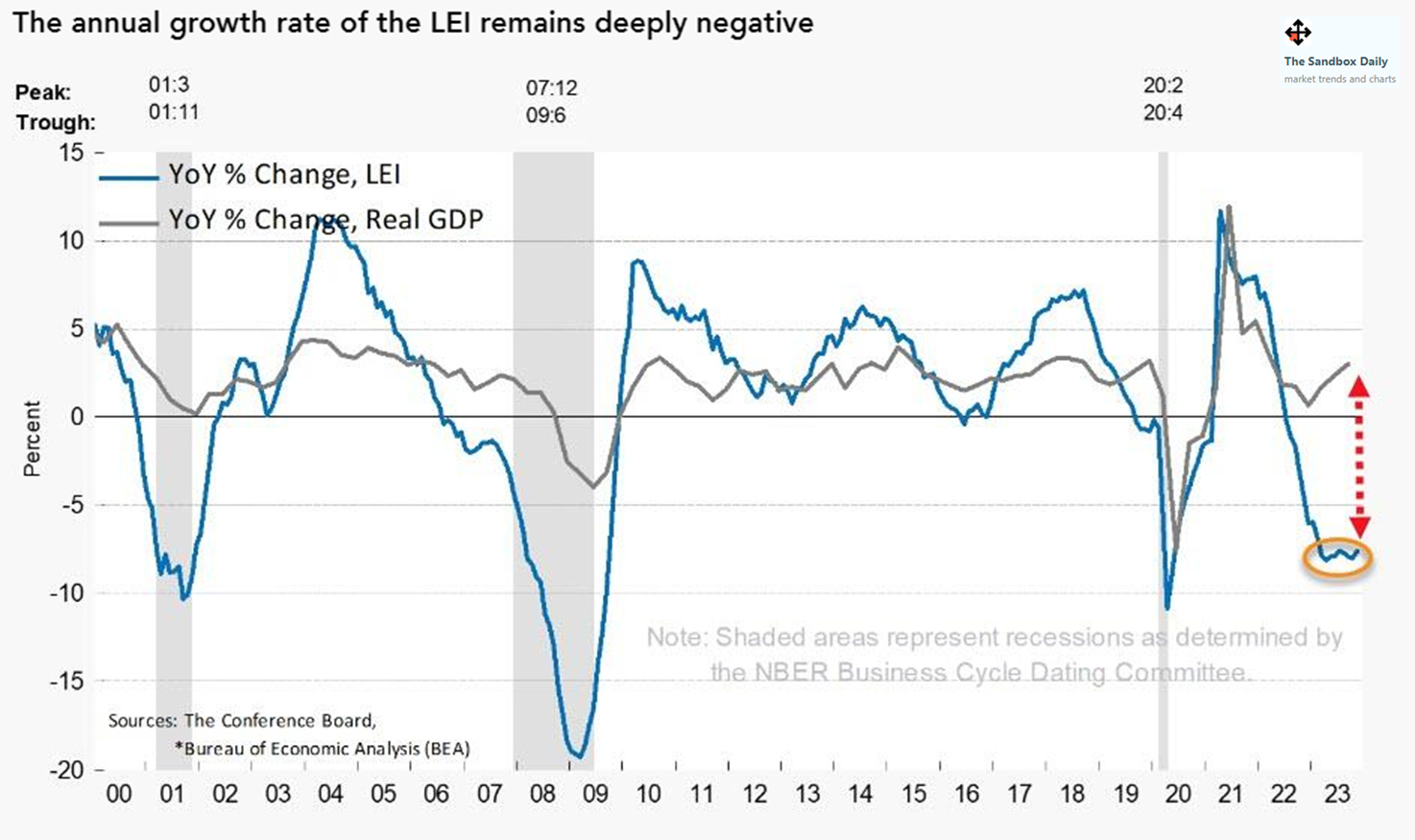

Leading Economic Indicators (LEI) index shows signs of stabilization

The Conference Board’s Leading Economic Indicators (LEI) index continued its decline in December, but dropped just -0.1% month-over-month (MoM) – it’s smallest MoM decline since March 2022 and a likely sign that conditions are stabilizing.

The Conference Board publishes leading, coincident, and lagging indexes designed to signal peaks and troughs in the business cycle for major global economies. Many economists and investors track this measure closely.

In fact, 6 of the 10 LEI components made positive contributions last month, led by higher stock prices, some easing in credit conditions, and fewer jobless claims. Unfortunately, those were more than offset by higher interest rates and declining manufacturing orders.

As you can see in the chart below, the YoY % change in the LEI likely reached a bottoming process, with the latest tick hooking higher. It’s also worth pointing out the decoupling between the LEI index (blue line) and Real GDP (grey line), similar to prior recessionary periods.

December’s decline marked the 21st consecutive decline in a row, suggesting persistent underlying weakness in the economic outlook.

As shown below, declines of this magnitude – of which there aren’t many – have always been associated with recession.

The LEI has been signaling recession for some time but one hasn’t materialized – similar to other common recession markers like the inverted yield curve or oil shocks. To be sure, the Conference Board still expects a “very short recession” in 2024.

For a better understanding of the relationship between the LEI and recessions, the next chart shows the percentage off the previous peak for the index. We are currently 12.5% off the 2021 peak. Also of note, there is usually 10.6 months between a peak and a recession on average; we are currently 24 months off from the 2021 peak.

The common recession indicators listed above contrast to recent economic data – consumer sentiment, retail sales and jobless claims – that have all been positive and consistent with an expanding economy. On Thursday this week, the Commerce Department will release its 1st estimate of 4th-quarter GDP growth for 2023, with forecasts of a number in the 1.7% to 2% range.

It’s possible that the LEI components – which favor manufacturing, credit, and consumer sentiment – could be underestimating the strength of this economy in light of high wealth effects, a tight labor market, and a large share of consumers locked into sub-5% 30-year fixed rate mortgages.

While no forecasting system is perfect, this one has a pretty good track record.

Source: The Conference Board, Liz Ann Sonders, Ned Davis Research, Advisor Perspectives

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.