Consumer confidence, plus Apple and a key lending survey

The Sandbox Daily (2.5.2024)

Welcome, Sandbox friends.

Today’s Daily discusses:

consumer confidence highest in 2 years, still below pre-pandemic levels

AAPL support at $180 has importance for investors

tighter credit having little impact on broad economy

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 -0.17% | S&P 500 -0.32% | Dow -0.71% | Russell 2000 -1.30%

FIXED INCOME: Barclays Agg Bond -0.82% | High Yield -0.47% | 2yr UST 4.481% | 10yr UST 4.168%

COMMODITIES: Brent Crude +0.92% to $78.04/barrel. Gold -0.60% to $2,041.3/oz.

BITCOIN: -1.24% to $42,362

US DOLLAR INDEX: +0.53% to 104.471

CBOE EQUITY PUT/CALL RATIO: 0.62

VIX: -1.30% to 13.67

Quote of the day

“Plans are worthless, but planning is everything.”

- Dwight Eisenhower

Consumer confidence highest in 2 years, still below pre-pandemic levels

The U.S. economy is performing well: real GDP grew 2.5% last year, real disposable income rose over 4%, the unemployment rate is just 3.7%, and inflation is slowing sharply. And yet…

Despite having rebounded from its lowest levels to near two-year highs, consumer confidence and Americans’ assessment of the government’s economic policies remain clearly below pre-pandemic levels.

Americans appear to be judging the state of the economy and government economic policy more harshly than usual.

So why is this?

Occam’s Razor would likely tell us to look at inflation.

Frustration with past high inflation appears to depress confidence for an enduring period of time, perhaps because consumers continue to find price levels unreasonable for some time.

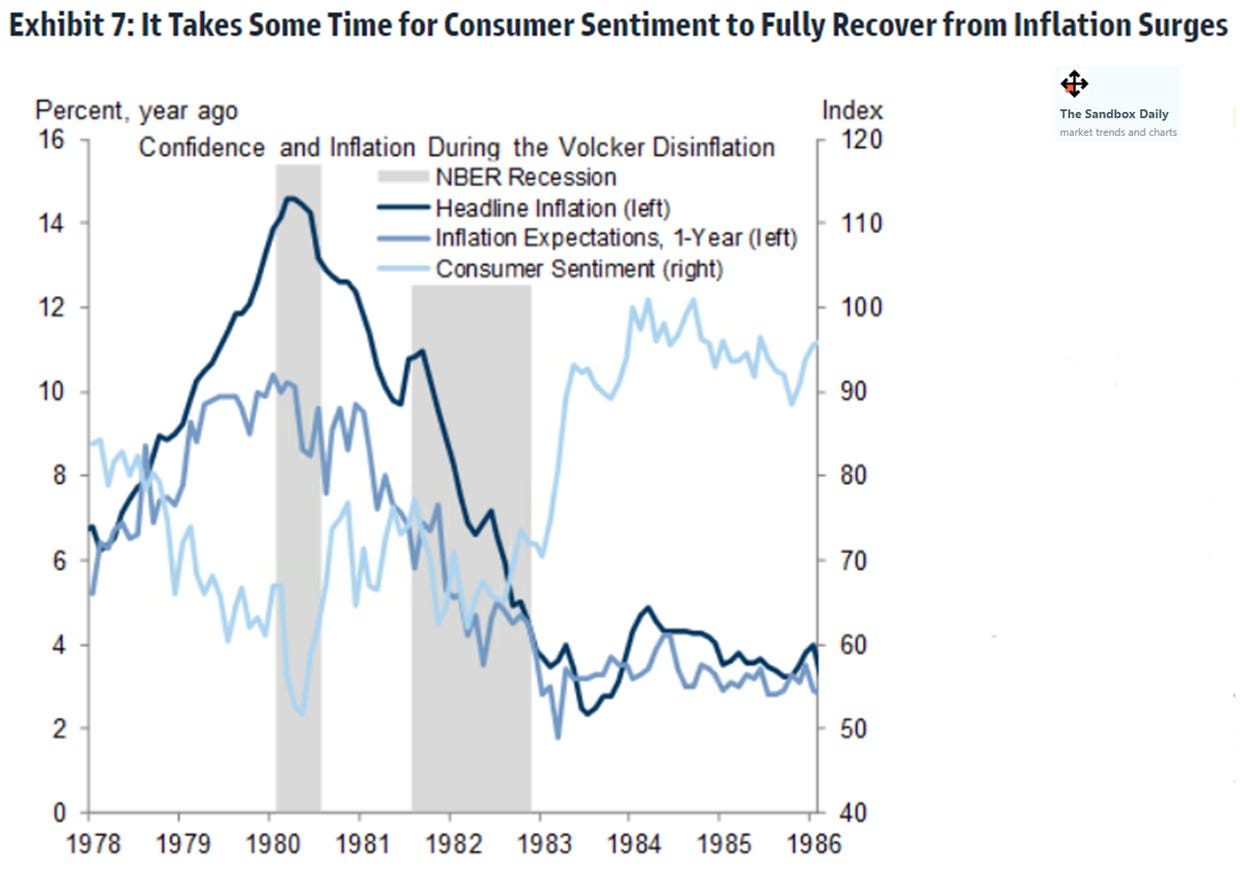

For example, the chart below shows that confidence only began to recover during the Volcker disinflation when YoY realized headline CPI inflation and year-ahead inflation expectations had fallen below 4%.

More importantly, though, the items with the greatest salience for consumers’ perception of inflation experienced especially large price increases over the last few years.

The items consumers buy most often, such as gasoline and frequently purchased food products (e.g. milk and eggs), have an outsized impact on perceptions of inflation, relative to their weight in the consumption basket. Some of these key items are up over 20% in cost in just the last few years.

And with the November election in the not-too-distant-future, what impact will voter perceptions of the state of the economy have on their ballots?

It appears that voters still rate inflation as the most important financial problem for their family in 2023.

Source: Wall Street Journal, Goldman Sachs Global Investment Research

AAPL support at $180 has importance for investors

Last week offered no shortage of fireworks for investors: JOLTS, a Fed meeting, the Employment Cost Index, the blowout nonfarm payrolls report, a swell of earnings reports ($GOOGL, $AAPL, $AMZN, $META, $MA to name a few), and Friday’s S&P 500 close going out at a fresh all-time high.

Yet what caught my attention was Apple holding key support around ~$180, a longer-term resistance-turned-support polarity level going back to 2021.

Apple delivered another subpar quarterly earnings report. AAPL’s post-earnings move noticeably lacked the firepower that stocks like Netflix, Meta Platforms, and Amazon showed after hours.

Quick reminder for those keeping score at home: Apple is 6.5% of the S&P 500 and 8.5% of the Nasdaq 100, so this stock is critically important for investors everywhere.

As shown below, its recent pullback got close to, but did not undercut, serious support around $179-180 that remains important for Apple structurally.

While Apple has underperformed its peers and the broader S&P 500 in recent months and has largely gone nowhere since mid-2023, its technical pattern has not yet turned bearish. This is due to lack of meaningful deterioration in its trend. The ability to hold near its 52-week highs and churn sideways, technically speaking, can be thought of as minor consolidation that normally is resolved by a push higher. But any break of $180 could metastasize to the broader U.S. equity market given Apple’s size and significance to indexes and passive strategies.

Thus, most investors should pay attention in the weeks and/or months ahead for any evidence of AAPL breaking down below the key level of $179-180, which is its technical line in the sand. Until/unless that happens, it’s right to not think too negatively of Apple despite some consolidation and underperformance since last summer.

Source: Brown Technical Insights, Fundstrat

Tighter credit having little impact on broad economy

The Federal Reserve's quarterly Senior Loan Officer Opinion Survey (SLOOS) report showed that through the 4th quarter of 2023, banks continued to tighten their lending standards/terms for commercial and industrial loans but at a slower pace than in recent quarters.

Meanwhile, loan demand continues to fall but at a slower rate, and may even be showing early and tepid signs of a rebound – an indication that customers remain cautious about accumulating more debt amidst higher interest rates but activity should improve alongside the better economic outlook.

Overall, banks had tightened access to credit due to the uncertain macro outlook, reduced tolerance for risk, falling credit quality and collateral values, and higher funding costs.

But the slowdown in the pace of tightening and recent strength in eco-data bodes well for lending conditions, and in turn, credit outperformance and tighter spreads.

Source: Federal Reserve, Ned Davis Research, Calculated Risk

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.