Consumer credit, plus 1st quarter GDP growth, stocks diverge from earnings, Fed breaking things, and defensive leadership

The Sandbox Daily (4.27.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

consumer credit fine, for now

real GDP growth slows but domestic demand still strong

divergence between stocks and earnings

when the Fed breaks things

defensive leadership following low VIX readings

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 +2.76% | S&P 500 +1.96% | Dow +1.57% | Russell 2000 +1.20%

FIXED INCOME: Barclays Agg Bond -0.36% | High Yield +0.33% | 2yr UST 4.082% | 10yr UST 3.524%

COMMODITIES: Brent Crude +0.81% to $78.32/barrel. Gold +0.05% to $1,997.1/oz.

BITCOIN: +7.64% to $29,643

US DOLLAR INDEX: +0.02% to 101.482

CBOE EQUITY PUT/CALL RATIO: 0.87

VIX: -9.61% to 17.03

Quote of the day

“Success is not final, failure is not fatal: It is the courage to continue that counts.”

-Winston Churchill

Consumer credit fine, for now

Household balance sheet levels remain strong, but Goldman Sachs estimate that households have drawn down around 40% of their excess savings so far and will have spent almost 60% by end-2023.

As cash levels come down, people turn to credit to fill the void. Household leverage, debt servicing costs, and delinquency rates remain low by historical standards, but revolving credit as a percentage of income could rise to its pre-pandemic level in 2023H2 if debt growth were to reaccelerate to its rapid pace in the 2nd half of 2022.

While overall loan delinquency rates remain low, some signs of stress are starting to emerge, as credit card delinquency rates for younger borrowers have now risen above their pre-pandemic levels.

Source: Goldman Sachs Global Investment Research

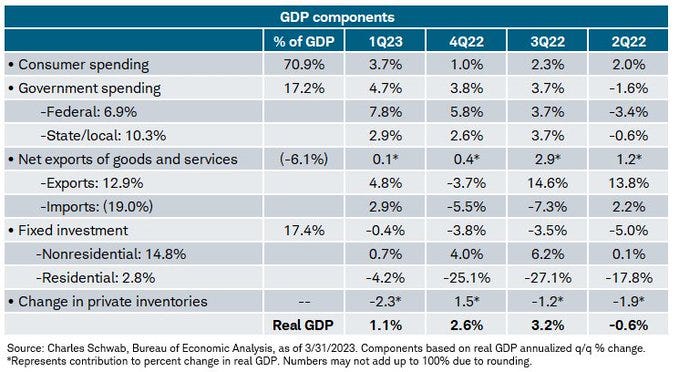

Real GDP growth slows, but domestic demand still strong

Real GDP rose at a +1.1% annualized rate in the 1st quarter, well below the consensus expectations of +2.0% and largely driven by a steep drop in inventories.

Consumer spending re-accelerated to +3.7% showing demand for goods and services remains strong. While sources of consumer strength such as excess savings from the pandemic stimulus and easy access to credit may be waning, consumer demand was supported in Q1 by stronger income growth. Real disposable personal income shot up at an 8.0% annualized rate, the most since 1Q21.

The headline GDP print of +1.1% was a sharp deceleration from the +2.6% growth rate in the 4th quarter of 2022 and the +2.1% growth for calendar year 2022. For context, the average growth rate for GDP since 1947 is +3.2%.

Here’s a detailed look at the sub-components of GDP and how 1Q23 measures against recent prior quarters:

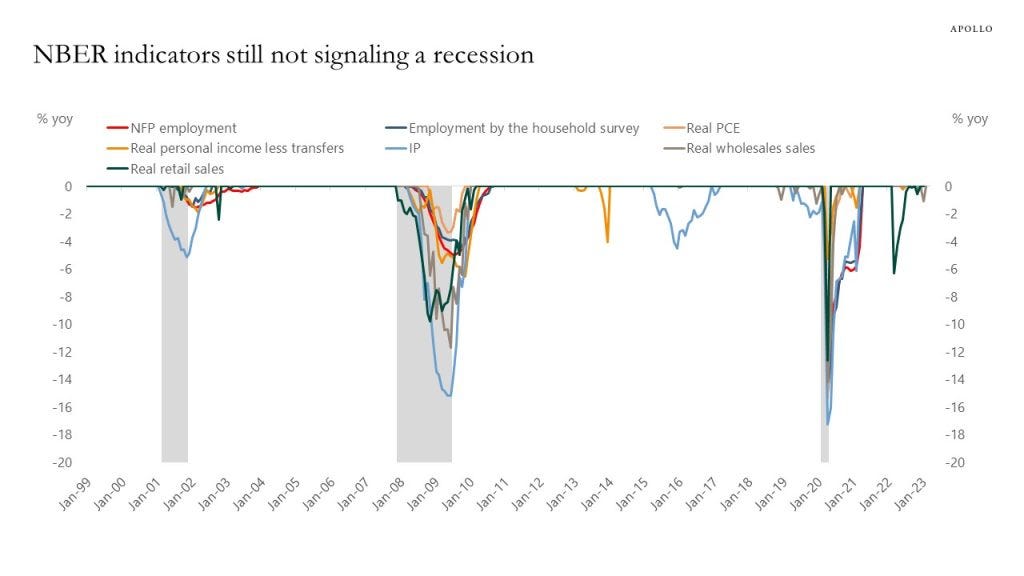

Economic growth is gradually downshifting under the enormous weight of the Fed’s tightening cycle, yet none of the indicators that the NBER recession committee normally monitors suggest we’re in a recession at the present moment.

Perhaps this slowing pace of growth signals the Federal Reserve's interest rate hikes are taking hold and an end to the tightening cycle may be near.

Source: CNBC, Bloomberg, Ned Davis Research, Charlie Bilello, Liz Ann Sonders, Apollo Global Management

Divergence between stocks and earnings

Stock markets may have become too pessimistic about corporate earnings despite the gloomy outlook for the economy.

The chart below tracks the forward earnings forecast versus the S&P 500 index since 2000. For the most part, the market tends to correlate to the direction of earnings over time because earnings are driven by the direction of economic activity.

Earnings crashed during the Global Financial Crisis, and so did the market. When EPS flatlined in 2015 and 2016, the market followed. 2020 COVID-19 health crisis – same thing.

In the past year or so, earnings forecasts have continued to rise (the blue line), while the S&P 500 remains 14-15% below its all-time high reached in January 2022 (the white line).

In part, this reflects a lower multiple of earnings that investors are willing to pay for stocks in light of sharply higher interest rates. It also shows analysts are overly optimistic regarding future earnings in corporate America, especially in the event of a broader economic slowdown.

But if earnings continue to rise – like much of history – then stocks will eventually follow and trade-up back to trend.

Source: Bloomberg, LPL Research

When the Fed breaks things

History repeats itself over and over again, as Fed tightening cycles generally end with a major financial event.

With First Republic Bank (FRC) bank in the news cycle this week – thanks to its stock trading down -61% since Monday and down -95% year-to-date – it’s often helpful to remind ourselves that the Fed often breaks something during the final stages of the economic cycle.

This rate hiking cycle has “broken” a number of things: pensions in the United Kingdom, the decade+ tech boom, crypto, SPACs, and regional and zombie banks.

Will there be another domino to fall?

Source: Yardeni Quick Takes

Defensive leadership following low VIX readings

The VIX Index dropped to 16.5 on April 19th, its lowest reading since December 31, 2021, a few days prior to the bull market top. Since then, it has risen to 18.8, but it remains low against the current market and macro backdrop.

This chart shows forward sector returns based on the market’s expectations for volatility – when the VIX is between 16 and 18 – and these low readings have been consistent with investor complacency, leaving stocks vulnerable to pullbacks. Forward 3-month returns have favored defensive leadership, as seen here by strength in Consumer Staples, Health Care, and Utilities.

Source: Ned Davis Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.