CPI inflation firmer than expected

The Sandbox Daily (2.14.2023)

Welcome, Sandbox friends.

Today’s Daily discusses the talk of the tape -> the Consumer Price Index (CPI) report from January. Everything else took a back seat to today’s price action.

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 +0.71% | S&P 500 -0.03% | Russell 2000 -0.06% | Dow -0.46%

FIXED INCOME: Barclays Agg Bond -0.35% | High Yield +0.03% | 2yr UST 4.622% | 10yr UST 3.753%

COMMODITIES: Brent Crude -1.47% to $85.34/barrel. Gold +0.08% to $1,864.9/oz.

BITCOIN: +2.72% to $22,234

US DOLLAR INDEX: -0.09% to 103.251

CBOE EQUITY PUT/CALL RATIO: 0.60

VIX: -7.03% to 18.91

January inflation data

This morning, the U.S. Bureau of Labor Statistics released their Consumer Price Index (CPI) report in January.

Headline Inflation

* CPI +0.5% MoM, versus +0.5% estimate and prior month of +0.1%

* CPI +6.4% YoY, versus +6.2% estimate and prior reading of +6.5%

Core Inflation

* CPI ex-food and inflation +0.4% MoM, versus +0.4% est. and prior +0.4%

* CPI ex-food and inflation +5.6% YoY, versus +5.5% est. and prior +5.7%

Overall, headline CPI moved down to +6.4% in January, the 7th consecutive decline in the YoY rate of inflation & the lowest level since October 2021. Core CPI (ex-food & energy) moved down to +5.6%, the 4th consecutive decline in the YoY rate & the lowest level since November 2021.

Source: U.S. Bureau of Labor Statistics, YCharts

Today versus peak inflation

Headline CPI print peaked this cycle in June at +9.06%. Today, we are at +6.41%.

What is driving the decline in consumer prices? Lower rates of inflation in New/Used Cars, Gasoline, Medical Care, Apparel, Food at Home, Electricity, Gas Utilities, and Fuel Oil.

Source: Charlie Bilello

Housing remains an issue

Shelter CPI, the largest component of the basket (33%), moved up to +7.9%, the highest rate of housing inflation since 1982. This category continues to be a hot-button topic and subject to intense debate as to how it influences, and perhaps distorts, the inflation data being reported.

Why is Shelter CPI still moving higher while actual rents (aka spot prices in the market today) are moving lower? Shelter CPI is a lagging indicator – due to how the survey data is collected (see below) – that had significantly understated actual housing inflation over the last 2 years.

Source: Charlie Bilello, Apricitas Economics

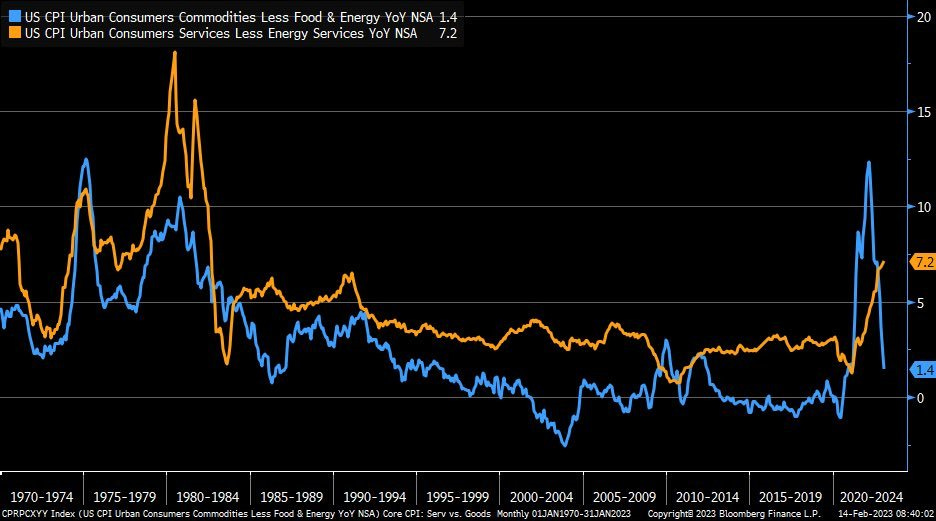

What has the market’s attention

Now much of the narrative and attention has shifted to parsing between goods inflation versus services inflation. As the economy has reopened, consumer preferences and spending have shifted from goods spending to services spending.

Core Goods CPI rose +1.4% YoY in January, while Core Services continues to rise at a much higher rate (+7.2% YoY).

Source: Liz Ann Sonders

Market response

Stocks ended the session somewhat flat after gyrating between gains and losses throughout the session, seemingly struggling to find direction after the slightly hotter CPI report. Treasury yields were mostly higher to reflect the restrictive narrative that Fed policymakers are warning. The VIX had an outsized move lower, closing lower by 7%.

Swaps contracts showed traders gave near-even odds for a 25 bps rate increase by the Fed in June, following similar 0.25% hikes in March and May. The rate-sensitive two-year Treasury yield rose past 4.6%.

Source: CME Fed Watch Tool, CNBC

Takeaways

Resilient consumer demand, particularly for services, paired with a tight labor market threaten to keep upward pressure on prices.

Yet, the Fed is expected to raise interest rates further before pausing to assess how the most aggressive tightening cycle in decades is impacting the economy. Policymakers have emphasized the need to hold rates at an elevated level for quite some time and cautioned against underestimating their will to do so. Investors are still betting the central bank will cut rates by year end, despite officials saying otherwise.

Both the headline and core inflation rates continue to run much higher than pre-pandemic times, but are showing noteworthy signs of cooling – perhaps indicating the worst of the inflationary pressures has likely passed and validating the anticipated phaseout of Federal Reserve interest-rate hikes.

Source: Ned Davis Research, Bloomberg, LPL Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.