Despite Iran conflict, the U.S. economy remains resilient to risks

The Sandbox Daily (5.7.2026)

Welcome, Sandbox friends.

Today’s Daily discusses:

U.S. economy remains battle-tested

Let’s dig in.

Blake

Markets in review

EQUITIES: Nasdaq 100 -0.12% | S&P 500 -0.38% | Dow -0.63% | Russell 2000 -1.63%

FIXED INCOME: Barclays Agg Bond -0.24% | High Yield -0.37% | 2yr UST 3.907% | 10yr UST 4.382%

COMMODITIES: Brent Crude -0.07% to $101.27/barrel. Gold +0.66% to $4,725.3/oz.

BITCOIN: -1.71% to $80,123

US DOLLAR INDEX: +0.14% to 98.16

CBOE TOTAL PUT/CALL RATIO: 0.67

VIX: -1.78% to 17.08

Quote of the day

“You have to slow down to see the miracles.”

- Thích Nhất Hạnh, Vietnamese Monk and Peace Activist

Despite Iran conflict, the U.S. economy remains resilient to risks

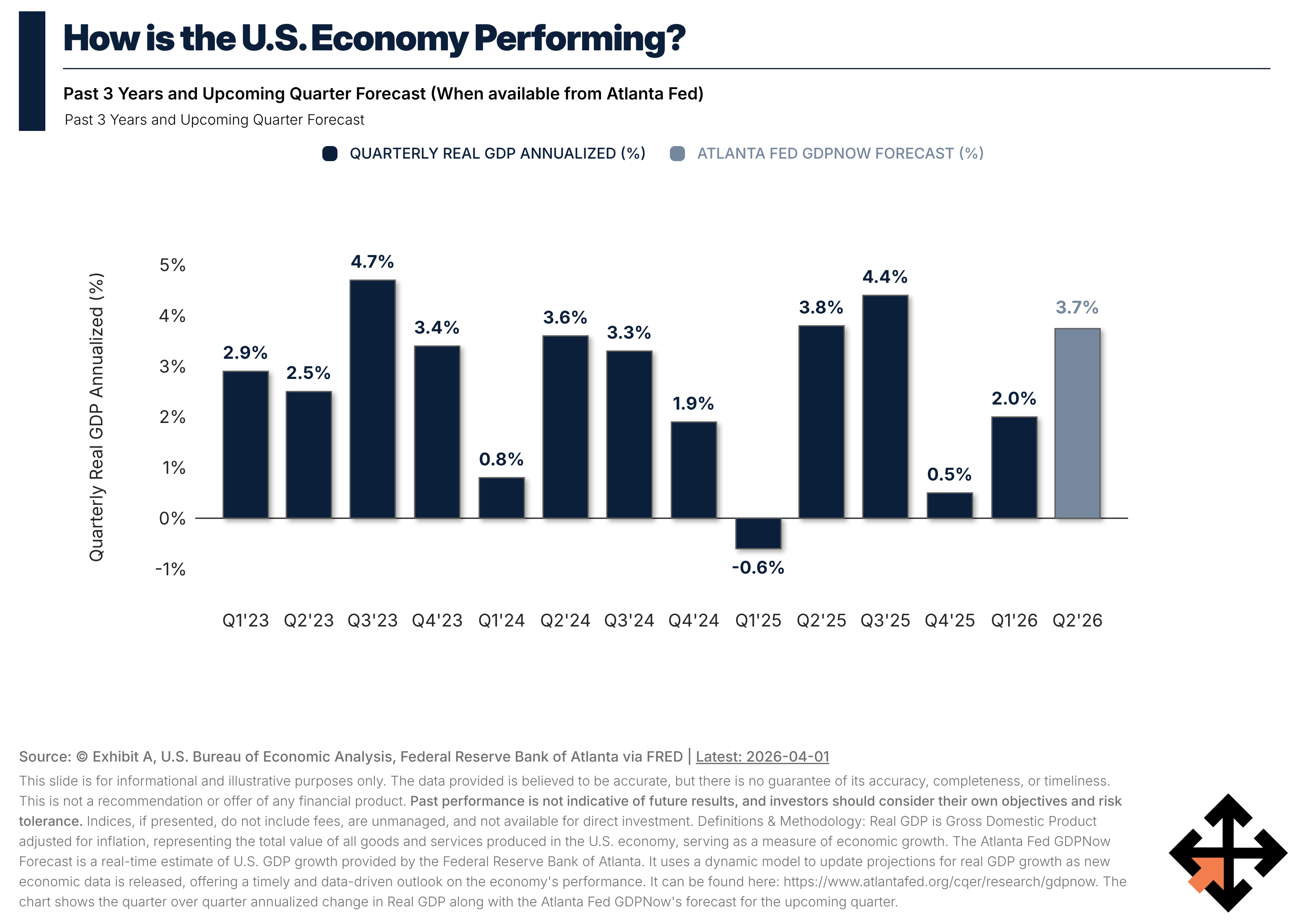

Data since the start of the Iran conflict shows the U.S. economy has continued to expand.

Real GDP increased at a robust 2.0% annualized rate in Q1, led by AI-related capex. The Atlanta Fed’s GDPNow Model estimates an acceleration in Q2 at 3.7%.

Manufacturing PMIs showed continued sector growth in April. Consumer spending has softened amid rising inflation, but there is no evidence of significant demand destruction yet. Labor market conditions remain stable amidst this low-hire-low-fire environment.

Most recession indicators remain neutral, indicating low risk of recession in the near term.

Broadly speaking, recent economic data has been coming in line with expectations, supporting a continued bull market in equities.

Does that mean that the U.S. economy is impervious to the Iran war?

In short, no.

Oil prices, which are about 50% higher than pre-war, could drive up inflation by an estimated 0.5%–2.0% this year per estimates and subtract from real GDP growth. Other commodity prices have also increased, and global supply chain pressures have started to build, both posing additional upside risk to inflation and downside risk to growth.

The risks would become more pronounced if the war, now in its 3rd month, draws out further or intensifies and the Strait of Hormuz remains closed.

But there are near-term factors, such as larger tax refunds this year, a positive stock market wealth effect, and increased defense spending on the war, that are boosting the economy in the short run. This in addition to AI-related spending, which has been strong and shows no signs of slowing.

Let’s unpack these positive developments a bit further:

Tax refunds

Tax refunds this year are boosting disposable income and providing a cushion against the surge in gasoline prices and inflation more broadly.

Per the Tax Foundation, tax refunds are higher by 14-15% from the same time last year; cumulative refunds could be ~$50 billion higher than 2025. Consumers spend about 90% of their income, with the rest going toward interest payments, transfers, and savings. That is a lot of money that will find its way back into the economy.

Most of the additional spending and GDP growth from tax refunds is taking place in the first half of the year, so we should expect slower consumer spending in the 2nd half as the sugar rush wears off.

Household wealth generation

Despite slower income growth, the offset can be mitigated by continued growth in household net worth – driven by the ongoing bull market in equities.

Real household net worth rose 4.7% YoY in 4Q25, above the 3.4% average annual gain historically. It has supported consumer spending for most of the post-pandemic expansion, and will continue to do so in 2026. At least while the bull market remains intact.

Military spending

Increased national defense spending should give a short-term boost to the economy.

Per the Pentagon, the Iran war has cost the U.S. an estimated $25 billion in the two months since it started. On an annualized basis, that’s equivalent to $150 billion, or 0.5% of nominal GDP – potentially adding to growth in 1H26 and offsetting some of the initial impact of the Iran war.

Despite the resilience of the economy so far in 2026, declines in consumer and small business confidence show growing anxiety about the outlook, which is a downside risk to future spending growth.

Persistent geopolitical risk and high economic policy uncertainty are also headwinds to growth.

Although many economic drivers remain in place, it’s always paid to be mindful of downside warnings to consider where the next shoe might fall.

Sources: Exhibit A, Ed Yardeni, St. Louis Fed, Bloomberg

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures (click here)

Please see our SEC Registered firm brochure (click here)

Please see our SEC Registered Form CRS (click here)