🍀 Discount window, plus retail sales, rate volatility, and the week in review 🍀

The Sandbox Daily (3.17.2023)

Welcome, Sandbox friends.

Happy St. Patrick’s Day to all! The word of the day is “Erin go bragh,” which is an Irish phrase that means “Ireland forever.”

Today’s Daily discusses:

discount window is open and emergency lending soars

Retail Sales pull back but show underlying strength

volatile week for rates

a brief recap to snapshot the week in markets

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 -0.49% | S&P 500 -1.10% | Dow -1.19% | Russell 2000 -2.56%

FIXED INCOME: Barclays Agg Bond +0.63% | High Yield -0.60% | 2yr UST 3.846% | 10yr UST 3.438%

COMMODITIES: Brent Crude -2.86% to $72.47/barrel. Gold +2.60% to $1,990.2/oz.

BITCOIN: +8.36% to $27,401

US DOLLAR INDEX: -0.53% to 103.864

CBOE EQUITY PUT/CALL RATIO: 0.66

VIX: +8.36% to 25.51

Quote of the day

“Short-term thinking is at the root of most investing problems. If you can focus on the next five years while the average investor is focused on the next five months, you have a powerful edge. Markets reward patience more than any other skill.”

- Morgan Housel, Wall Street Journal

Discount window is open and emergency lending soars

The Fed's "lender of last resort" business is booming, as the collapse of Silicon Valley Bank last week set off one of the worst financial panics since 2008-09.

The amount banks were borrowing from the Fed's "discount window" — its traditional channel of lending during a panic — exploded higher by +$148.3 billion dollars during the weekly period that ended Wednesday, a sign of just how focused banks were on securing cash as a flurry of bank runs broke out.

A key role of central banks is to lend to the financial system during panicky periods. At the window, banks must hand over high-quality assets, such as Treasury bonds, as collateral for loans.

The surge of the discount window borrowing contextualizes the scale of the shock. The only thing comparable in recent memory is the great financial crisis.

Source: Federal Reserve, Financial Times, Axios

Retail Sales pull back but show underlying strength

U.S. retail sales fell moderately in February, likely payback after the prior month's outsized increase, but the underlying momentum remained strong, suggesting the economy continued to expand in the first quarter despite higher borrowing costs.

Retail sales fell -0.4%, down in 3 of the past 4 months, but in line with the consensus. Looking through increased volatility around the turn of the year, the 3-month average of sales - which smoothes some of the volatility – picked up +0.7%. Although there are some signs of weakness amid tighter lending standards and higher financing costs for big-ticket purchases, retail sales continue to show underlying strength in consumer spending.

On a YoY trend basis, retail sales eased to +6.4% from +6.6% in the prior month, the slowest pace since January 2021, but still faster than pre-pandemic.

Consumer demand is being supported by continued labor market strength and nominal wage gains, continued utilization of credit, and savings accumulated during the pandemic. It suggests that the consumer – and to a great extent, the economy – may not be as close to recession despite other indicators pointing in that direction. It also suggests that if the Fed wants to bring down inflation by slowing demand, it will have to keep monetary policy tighter for longer.

Source: Ned Davis Research, Bloomberg

Volatile week for rates

The bond market just experienced one of its most volatile weeks in history.

When it comes to the middle and long end of the yield curve, the U.S. 10-year and 30-year Treasury yields are challenging key former highs.

As you can see, this polarity zone coincides with the June highs from last year and the pivot lows from February, making it a critical level of interest.

If yields violate this level, we could expect further strength from long-duration assets such as bonds and growth stocks in the foreseeable future. However, a bounce from current levels could keep the trend intact.

Source: All Star Charts

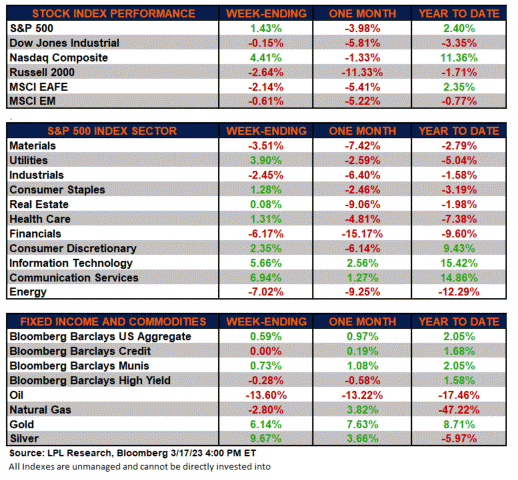

The week in review

Talk of the tape: Banks under pressure and bond market volatility were the overarching themes of the week. Market pricing around the Fed’s rate outlook path has also been very volatile as the banking situation has potentially changed the Fed's reaction function now that it has to balance financial stability concerns with still-elevated inflation that isn't falling as fast as the central bank would like. Also, a lot of market attention shifted to the Fed’s balance sheet, which rose significantly with a spike in borrowing against both the discount window and the new Bank Term Funding Program.

The focus now shifts to next week's Federal Reserve March meeting. Markets see a ~70% chance of a 25bp hike at the Fed March meeting and no further rate hikes beyond this month. Market pricing for cuts starting in June reflects recession/hard landing fears and expectations for tighter bank lending standards.

Stocks: Stocks ended the week mixed as trading was quite volatile. Bank balance sheets are a new worry for investors, in addition to concerns with hawkish central banks’ tenuous response to persistent inflation. SVB Financial and Signature Bank’s failures this past weekend along with First Republic Bank’s challenges has market participants concerned over more banking woes as some investors believe the economy may be on the brink of recession.

As the Federal Reserve has increased interest rates, longer-term bonds purchased by banks have since declined in value, creating a headwind for the banking sector. Given the market decline of bonds last year, some poorly hedged banks find themselves in a predicament where they may need to raise additional capital per banking regulations. Raising capital may include stock sales, putting downward pressure on share prices as banks are hamstrung from the inverted yield curve.

Bonds: The Bloomberg Aggregate Bond Index finished the week higher as yields declined, reversing a pattern of lower bond prices and higher yields. Given the concerns over the banking landscape, bond investors believe the Fed could reverse course on monetary policy and the “higher-for-longer” theme.

U.S. corporate credit spreads widened last week with the investment grade segment higher by 0.15% and the high yield segment wider by 0.54%. Neither market has meaningful exposure to regional banks, so the selloff we’re seeing is likely from growing risk aversion instead of an increase in default expectations. Nonetheless, despite the recent widening, credit spreads for both markets are at historical average levels.

Commodities: Energy prices finished lower as traders grew concerned over the present banking climate and its potential effect on the economy as oil reached a 15-month low this week. Natural gas prices declined even as winter makes a last stand in the United States. The major metals (gold, silver, and copper) ended the week mixed as gold and silver caught bids this week as some investors sought refuge in precious metals given this week’s banking news.

Source: Dwyer Strategy, LPL Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.