Do you smell that? The asymmetric opportunity for bondhodlers.

The Sandbox Daily (1.29.2025)

Welcome, Sandbox friends.

Today’s Daily discusses:

the opportunity in bonds

Let’s dig in.

Blake

Markets in review

EQUITIES: Nasdaq 100 -0.24% | Russell 2000 -0.25% | Dow -0.31% | S&P 500 -0.47%

FIXED INCOME: Barclays Agg Bond -0.06% | High Yield -0.06% | 2yr UST 4.221% | 10yr UST 4.536%

COMMODITIES: Brent Crude -0.84% to $76.84/barrel. Gold +0.08% to $2,769.9/oz.

BITCOIN: +2.89% to $104,384

US DOLLAR INDEX: +0.11% to 107.982

CBOE TOTAL PUT/CALL RATIO: 0.75

VIX: +0.91% to 16.56

Quote of the day

“Ships are safe at harbor but that's not what they're built for.”

- John A. Shedd

The asymmetric opportunity for bondhodlers

The path of interest rates has been highly uncertain and quite volatile over the past few years as investors play catch up to the everchanging expectations around economic growth, Federal Reserve rate moves, and White House policy.

The 10-year Treasury yield has risen as high as 4.8% in recent weeks before settling below 4.6% today. The 2-year Treasury yield remains elevated around 4.2%, while the 30-year fixed mortgage rate remains above 7%.

Without some context though, the aforementioned levels are somewhat meaningless.

Rewinding the clocks all the back to the early days of the pandemic, we had the 10-year Treasury yield trading as low as 0.5%, the 2-year yield at 0.1%, and the 30-year fixed mortgage at 2.6%.

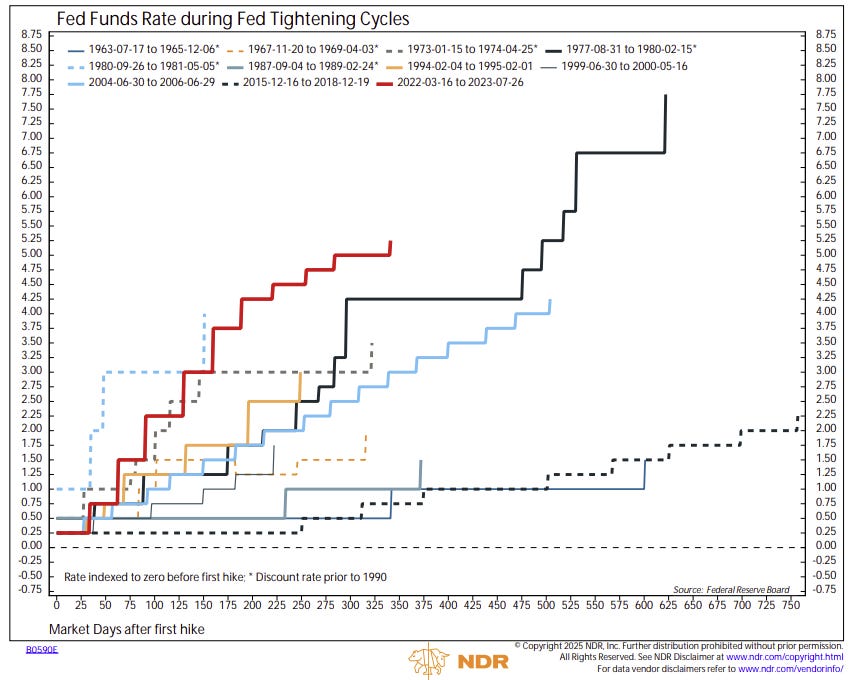

Think about the significant difference in these two sets of numbers for a minute because the rise in rates we’ve just endured over the last five years was the result of the fastest tightening cycle in modern history. See the red line below.

This monetary policy tightening matters because the rate increases have been quite problematic for bond investors, many of whom are in retirement.

Bonds as an asset class have lagged stock returns by a staggering amount. Only High Yield bonds, colloquially known as chicken equity, have come within a whiff of U.S. equities.

Just today, the Federal Reserve held interest rates steady – leaving their key overnight benchmark rate between 4.25% and 4.50%. The job market has proven to be remarkably resilient, while the future trajectory of inflation remains on a protracted path down to their target of 2.0-2.5%. For now, the Fed will judge the future course of its policy and procedures by synthesizing the incoming data over the coming weeks and months.

Interest rates are important because they affect the balance between stocks and bonds.

When interest rates are higher, investors can earn more from relatively safe investments like government bonds.

At 4.5-5.0%, bonds become real competition for stocks.

This is especially true when equity valuations are high. The historical record shows the future distribution of returns has been relatively muted on average, as is the case today.

Another important point. Against a backdrop of higher yields, yield investors face asymmetric opportunities ahead.

In the graphic below, J.P. Morgan captures the relationship between bond prices and interest rates in rather simple mathematical terms, showing the one-sided risk/reward opportunity in favor of bonds at these higher interest rate levels.

Assuming a parallel 1% shift in interest rates higher and lower from current rates, the chart shows how different sectors across fixed income would perform.

Example: If interest rates fall 1% from current levels, Investment Grade Corporate Bonds will generate a total positive return of +12.1%. If the opposite happens and interest rates continue to rise another 1%, IG Corporates will only lose -1.5% on a total return basis.

That is what you call asymmetric return.

With the Federal Reserve no longer hiking interest rates, the primary headwind this cycle – hawkish monetary policy jawboning the bond market – has been cleared. The Fed is done hiking rates.

Today, the market landscape for bonds has transformed into one of opportunity.

Based on current relative valuations and higher starting yields, there is compelling value across many fixed income market segments. Absolute yields are attractive compared with other assets across the risk and liquidity spectrum – including cash – and historically, starting yields have been a strong indicator of long-term fixed income performance.

All this to say it’s a compelling environment ripe with opportunity for bondhodlers.

Source: All Star Charts, Ned Davis Research, YCharts, PIMCO, J.P. Morgan, The Big Short

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures at the Sandbox Financial Partners website:

"When interest rates are higher, investors can earn more from relatively safe investments like government bonds. At 4.5-5.0%, bonds become real competition for stocks."

However, there is a price you pay for safety. I remember at the beginning of 2023, people were saying there was no point of investing in risk assets given that they could get 5% risk free. Back then, everyone was predicting a recession based on the unprecedented speed of rate hikes.

That year, the S&P went up 24%. Man plans, God laughs.

Good stuff, thx! 🙌