Don't fight the Fed!!, and what today's FOMC meeting means about the coming global easing cycle (hint: it's historic)

The Sandbox Daily (7.31.2024)

Welcome, Sandbox friends.

Market stalwart Nvidia exploded to the upside today gaining +12.8% (+$329B in market cap, the largest addition in a single-day) and the Federal Reserve kept interest rates unchanged (more on that below).

Today’s Daily discusses:

the coming global easing cycle

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 +3.01% | S&P 500 +1.58% | Russell 2000 +0.51% | Dow +0.24%

FIXED INCOME: Barclays Agg Bond +0.54% | High Yield +0.36% | 2yr UST 4.271% | 10yr UST 4.044%

COMMODITIES: Brent Crude +2.66% to $80.72/barrel. Gold +0.78% to $2,492.4/oz.

BITCOIN: +0.72% to $64,811

US DOLLAR INDEX: -2.19% to 104.016

CBOE EQUITY PUT/CALL RATIO: 0.68

VIX: -7.52 % to 16.36

Quote of the day

Rule #6: Don’t fight the FED (less valid than #1).

Rule #1: The trend is your friend, don’t fight the tape.

- Marty Zweig

Synchronized easing on the way

Today, the Federal Reserve left rates unchanged at 5.25%-5.50% (a 23 year high) for the 8th consecutive meeting, reiterating that the Federal Open Markets Committee will not cut interest rates until it “has gained greater confidence” that inflation is move closer to 2%, however Federal Reserve Chair Jerome Powell did acknowledge it could cut rates at its September meeting if economic data continues its current path.

The growing easing bias was apparent in the FOMC statement that showed some meaningful changes from the June meeting.

OUT: “the Committee remains highly attentive to inflation risks”

IN: “the Committee is attentive to the risks to both sides of its dual mandate”

The shift in the scope and tone of the statement and press conference shows a departure from the 2022-2023 inflation fight to the acknowledgment of recent cooling in the labor market here in 2024.

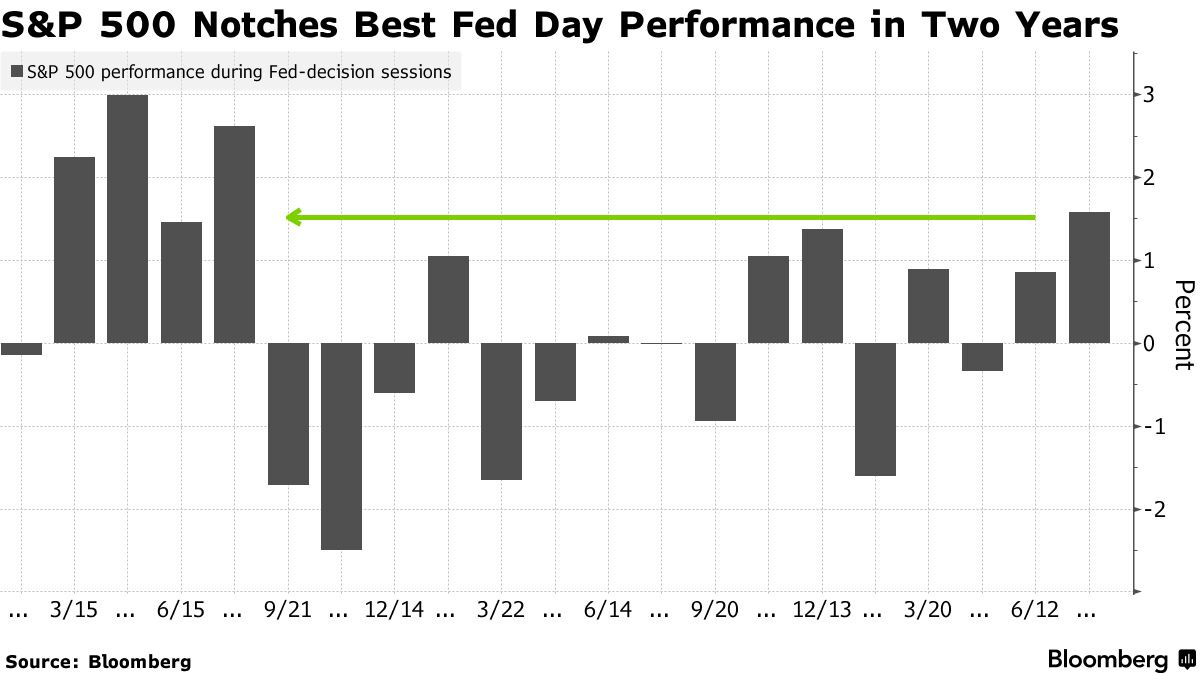

Dovish comments from Jerome Powell in his press conference helped extend a rally in stocks that started with a surge in key technology companies, with the market scoring its best Federal Reserve day in two years.

Neil Dutta at Renaissance Macro Research had this to share: “It definitely sounds like they are just waiting for the sake of waiting. After all, by his own admission, all the data are already pointing in the direction he wants to see!”

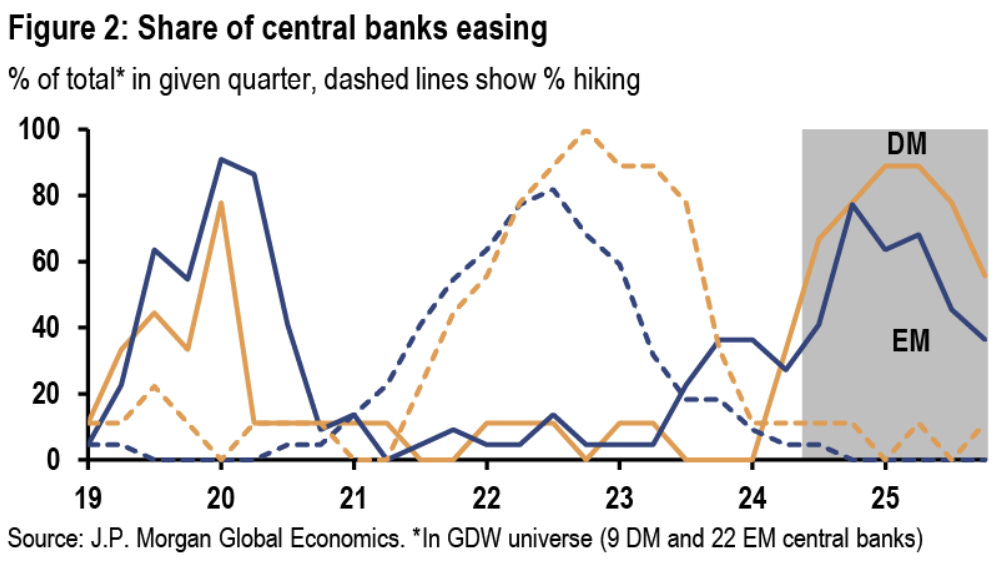

Since flipping the calendar to 2024 and looking over the horizon in the coming months, the expectation is nearly all central banks will be on a slow path back toward neutral. In fact, the coming year is forecasted to deliver the most synchronized monetary easing cycle in history, outside of a recession.

As you can see below, the past 4 years have delivered large swings in global monetary policy as central banks responded to significant shifts in activity and inflation. Some call this oversteering.

From rapid rate cuts in March 2020 as the pandemic left the global economy in tatters to sharp rate hikes in 2022-2023 as inflation surged in response to wide demand-supply imbalances, global policy rates went from multidecade lows to multidecade highs in under 3 years.

Domestic conditions are almost always the key to policy setting. Progress on inflation and recoveries vary considerably across economies. And yet, with core inflation having cooled considerably from its peak in 4Q22, expectations are now for an easing cycle that brings rates back closer to neutral over the coming years.

Sufficient disinflation for some has already enabled 1/3 of DM central banks to deliver initial rate cuts, with 1/3 of EM economies already easing for the better part of the past year.

The chart below shows just how much monetary policy has swung over the past 4-5 years.

The rapid cuts in response to the pandemic saw the balance of global central bank rate action (% hiking - % cutting) of -83% in 1Q20, a low only ever seen during the Global Financial Crisis in 1Q09.

Even more remarkable than the breadth of the cutting cycle is the breadth of the 2021-2023 hiking cycle. The unwind of easy policies was so fast and broad-based that rate hiking delivered a +73% balance by 4Q22 -> the most concentrated period of rate hiking in over half a century.

In late 2023 and throughout 2024, we’ve seen the pendulum swing back down again as the easing bias takes shape across the globe.

Looking forward, we should expect easing cycles to broaden in 2H24 and into 2025. Along with varying domestic outcomes, there is also a risk is that central banks feel a gravitational pull from the Federal Reserve or European Central Bank that moves more cautiously in easing, and global policy remains tighter than necessary.

Despite broad commonalities across economies, domestic factors continue to be the key driver of setting monetary policy.

Reaction functions are not the same across the world, however the last 4-5 years show how truly unique this economic cycle has been!

Source: Nick Timiraos, CNBC, J.P. Morgan Markets, All Star Charts, Global Sachs Global Investment Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.