East Coast dockworkers strike, plus the residential housing unlock and central banks are easing (lots of them)

The Sandbox Daily (10.3.2024)

Welcome, Sandbox friends.

Today’s Daily discusses:

not quite pandemic-level disruptions, but disruptive nonetheless

one scary chart

global “recalibration”

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 -0.05% | S&P 500 -0.17% | Dow -0.44% | Russell 2000 -0.68%

FIXED INCOME: Barclays Agg Bond -0.41% | High Yield -0.24% | 2yr UST 3.709% | 10yr UST 3.852%

COMMODITIES: Brent Crude +5.25% to $77.78/barrel. Gold +0.31% to $2,677.8/oz.

BITCOIN: -0.18% to $60,758

US DOLLAR INDEX: +0.29% to 101.971

CBOE EQUITY PUT/CALL RATIO: 0.56

VIX: +8.41% to 20.49

Quote of the day

“You will face many defeats in life, but never let yourself be defeated.”

- Maya Angelou

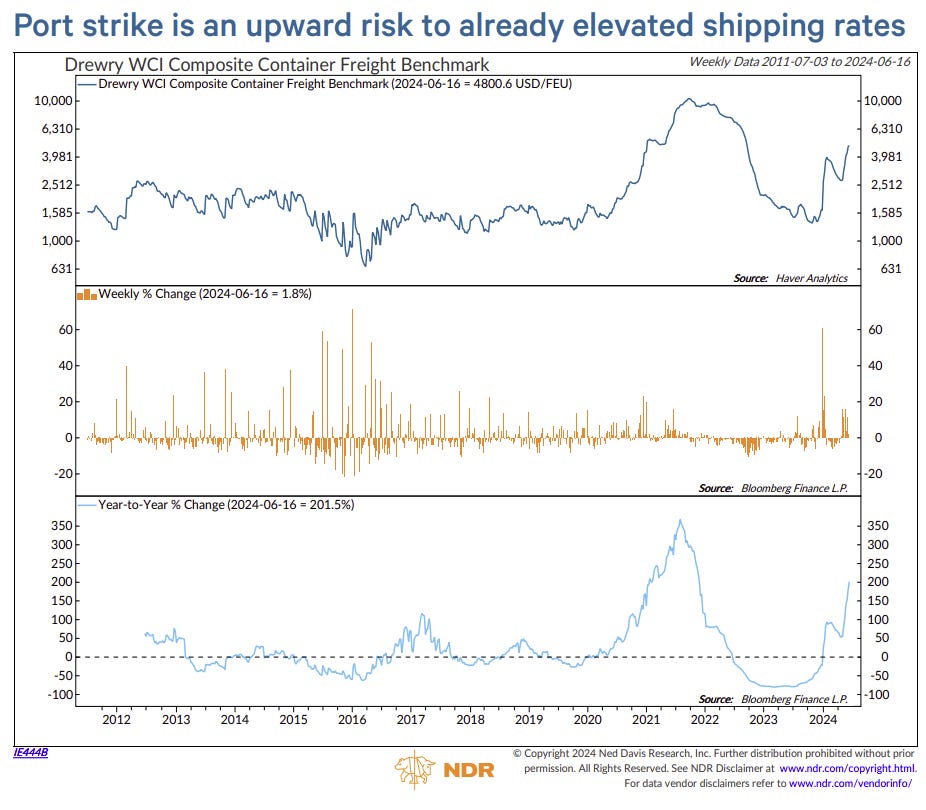

Not pandemic-level disruptions, but disruptive nonetheless

Dockworkers and longshoremen in East Coast ports are now on strike in a major labor action with as-yet-unknown consequences for the U.S. economy and international trade.

An estimated 45,000 workers of the International Longshoremen’s Association (ILA) are impacted as work stoppages began Tuesday, with compensation and automation the key points of contention. 36 ports that handle more than half of U.S. container shipments and roughly 25% of U.S. good imports have been disrupted.

Policy experts are saying the strike could cost the economy $4-5 billion per day.

Like the pandemic and other periods of supply-chain disruptions, a prolonged port strike will strain existing inventories – which have normalized and returned to pre-pandemic trends across most industries.

Most consumers won’t notice a meaningful change in prices, but that could change if the labor strike drags on weeks and/or months.

Major businesses are responding to the disruption by placing orders early and rerouting some shipments through the West Coast ports.

Ultimately, higher prices could be down the road.

The deadlock on contract negotiations come at a time when shipping rates have already been rising amidst war conflicts in the Middle East and the Red Sea.

Unless the port strikes drag on longer than anticipated – they often don’t, see chart below – the overall impact should be immaterial.

America's latest GDP figures were $29 trillion annually. Assuming the $4-5 billion of forecasted economic activity is lost, GDP will contract by only 0.027% for each week the port strike lasts.

Source: AP News, CNBC, Ned Davis Research, Goldman Sachs Global Investment Research

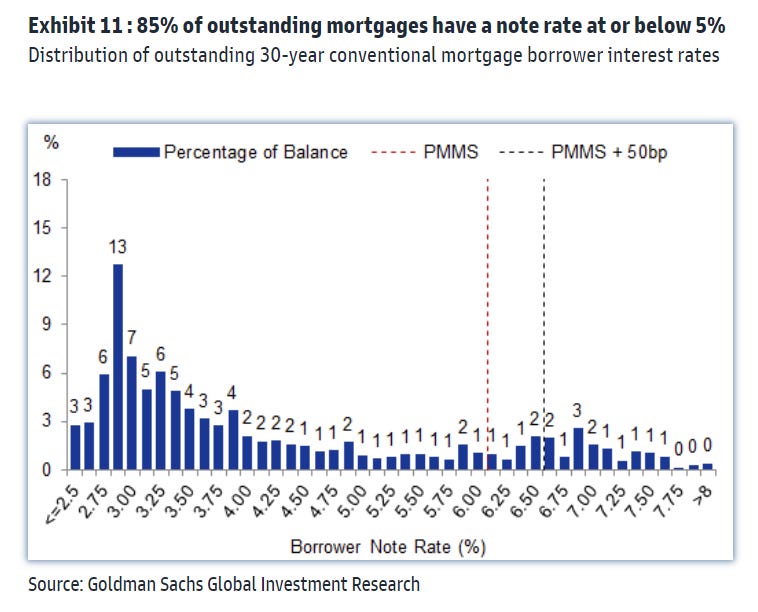

One scary chart

If the incremental home buyer is seeking a 5-handle on mortgage rates, then the residential housing market unlock is still a ways off.

Given that the most recent Freddie Mac Primary Mortgage Market Survey (PMMS) rate is 6.1-6.2%, the market rate for mortgage loans still has to drop another full percentage point before inventories change hands.

Wow.

Keep in mind the outstanding stock of the mortgage pool remains at that key 5% level.

Source: Goldman Sachs Global Investment Research, Daily Chartbook, Rick Palacios Jr.

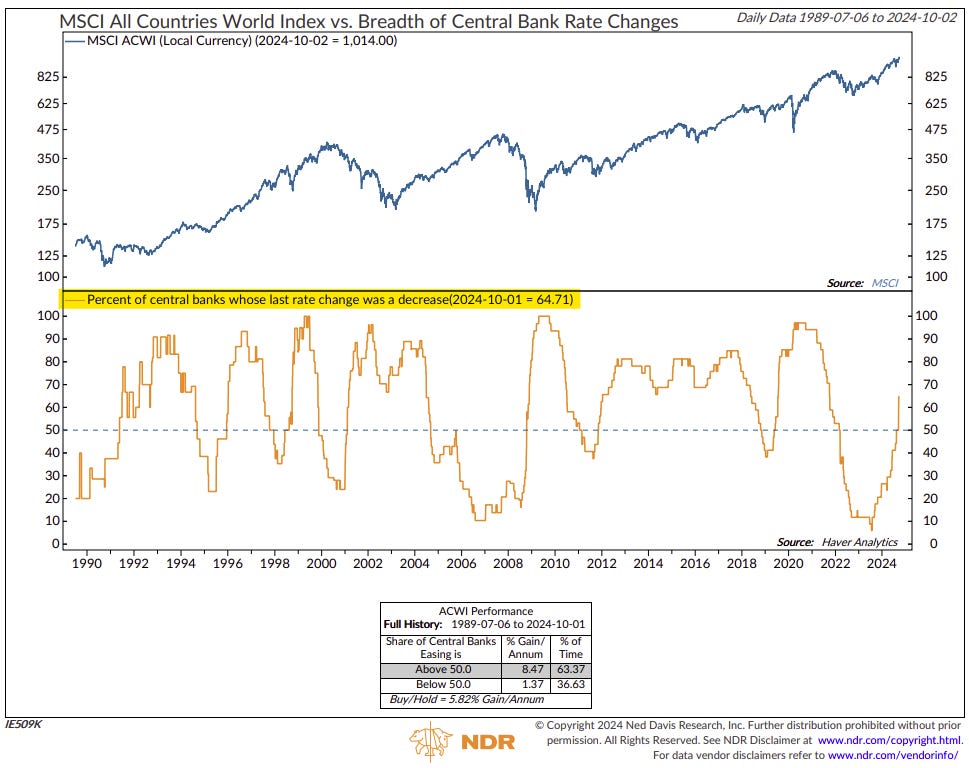

Global “recalibration”

Central Banks around the world are easing off their aggressive stance, as policymakers have (mostly) lowered inflation within sight of their targets. Now, each is attempting to delicately steer their economies towards the so-called soft landing.

Keep rates too high for too long and risk excessive damage – such as a spike in unemployment – by unnecessarily self-inducing economic recession.

Instead, officials are responding to the data – as they should – and are lowering rates to remove their restrictive monetary biases.

The pivot has important ramifications as it eases global financial conditions. Manufacturing, housing, and automobile sales can all shake free from their own localized comas. C-Suites, after preparing for Jamie Dimon’s economic “hurricane,” finally can greenlight CapEx plans. The credit creation cycle can thaw.

And this pivot is happening everywhere. Two-thirds of the world’s central banks are now in easing cycles.

As shown in the bottom cutout table in the chart above, when more than half of the world’s central banks are in easing cycles, it’s historically been a bullish backdrop for global equities – with the MSCI All Country World Index (ACWI) averaging 8.47% per year.

And, to be clear, these Central Banks aren’t Eswatini in Africa or Albania in Europe.

Save Japan, these are the Central Banks that move the needle.

Source: Ned Davis Research, J.P. Morgan Markets

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures at the Sandbox Financial Partners website: