ECB begins QT, plus Warren Buffett buys OXY, stock buybacks, labor data, and a winning mindset

The Sandbox Daily (3.8.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

Quantitative Tightening (QT) begins for the European Central Bank

Warren Buffett buys more Occidental Petroleum (OXY)

stock buybacks are back

fresh batch of labor data (ADP private payrolls and the JOLTS report from BLS)

an investor’s winning mindset

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 +0.52% | S&P 500 +0.14% | Russell 2000 +0.04% | Dow -0.18%

FIXED INCOME: Barclays Agg Bond -0.10% | High Yield -0.47% | 2yr UST 5.072% | 10yr UST 3.991%

COMMODITIES: Brent Crude -0.94% to $82.51/barrel. Gold -0.11% to $1,818.0/oz.

BITCOIN: -0.42% to $21,987

US DOLLAR INDEX: +0.08% to 105.703

CBOE EQUITY PUT/CALL RATIO: 0.74

VIX: -2.45% to 19.11

Quote of the day

“Focusing on the performance or cost of a portfolio relative to something other than a plan is like decorating a house that has no foundation. Making poor decisions – even if at a low cost or even no cost – won’t do anyone any good.”

-Josh Brown, A Portfolio is Not a Plan

QT begins for the European Central Bank

Last week marked the operational start of the European Central Bank’s (ECB) quantitative tightening (QT) program, the plan to reduce bond holdings via passive balance sheet run-off (aka maturing bonds will no longer be reinvested) – similar to what the Federal Reserve Bank in the United States began in the summer of 2022.

The ECB has set an initial capped reduction of €15bn/month on average between March and June 2023. The subsequent pace is yet to be determined, with the ECB preserving optionality to observe market functioning and adjust the pace accordingly. As a share of GDP, balance sheet run-off in Europe is slower than that of the Fed.

This ends a period of almost a decade during which the ECB’s balance sheet was used actively to reduce yields and dampen volatility.

The market will closely be watching the direct impact on yields but also secondary effects in currency markets and stock prices/volatility.

Source: Goldman Sachs Global Investment Research

Death, taxes, and Buffett buying $OXY under $60

Warren Buffett is back again with the Berkshire put in Occidental Petroleum (OXY).

Since this time last year, every time the stock falls below 60, the market gets an insider filing from Berkshire Hathaway (BRK).

In his first Form 4 filing since September, Buffett just reported an additional 5.8 million shares of OXY at an average price of $61.10 per share. The transactions were spread out over the last three trading days.

The latest purchases, worth roughly $354 million, give Berkshire Hathaway a new ownership stake of roughly 30% – based on 284 million shares, which includes 84 million shares from warrants – and makes Berkshire by far the largest shareholder in the company.

Source: All Star Charts

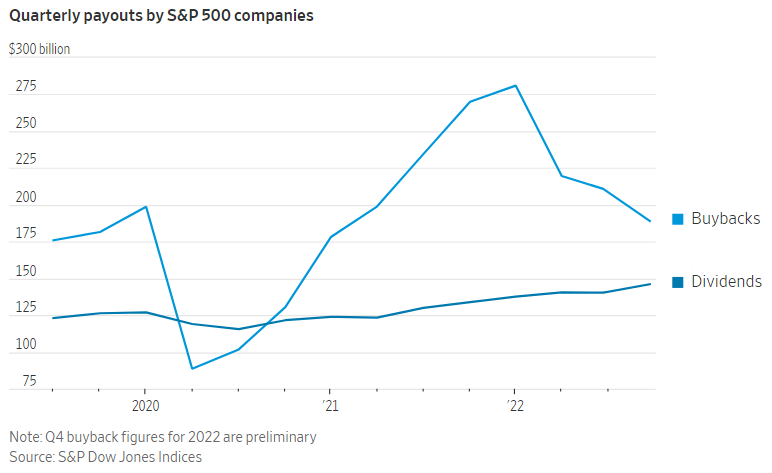

Stock buybacks

Buybacks are back after many companies suspended share repurchase programs in the wake of the pandemic.

Total S&P 500 buybacks jumped from $513 billion in 2020 to $918 billion in 2022. According to S&P Dow Jones Indices estimates, buybacks on the S&P 500 will likely exceed $1 trillion in 2023.

While the raw dollar amounts of buybacks are on the rise, as a percentage of the total value of the S&P 500, they have shrunk by almost half since 2007 – to roughly 0.7% from 1.3%, according to S&P Dow Jones Indices. The buyback boom has been offset (perhaps dwarfed) by the rise in stocks overall.

And here is a chart breaking down total buybacks by sector since 2020:

Rising free cash flows should continue to support buybacks this year. However, Washington’s new 1% tax on net buybacks, rising interest rates, and the prospect of a recession could negatively impact repurchase activity from management’s perspective. In addition, buybacks are also competing with a ramp-up in corporate capital expenditure spending.

Source: Wall Street Journal, LPL Research

Fresh batch of labor data

Two new labor reports for the market to digest today: 1) ADP private payrolls and 2) the BLS Job Openings and Labor Turnover Survey (JOLTS) report.

U.S. companies added more jobs than expected in February, underscoring persistent demand for labor that’s keeping wage growth elevated. Per a jobs report this morning from payroll firm ADP, private employers added 242,000 jobs last month, which is more than double of January’s gain and above the consensus of 205,000. Annual pay for workers who stayed in their jobs experienced a +7.2% pay increase in February from a year ago, another indication of a tight labor market.

The payroll increase last month was widespread across industries, with hiring gains in leisure and hospitality leading the way.

In a separate labor report from the Bureau of Labor Statistics (BLS) – the Job Openings and Labor Turnover Survey (JOLTS) – vacancies at U.S. employers retreated to start of the year but remained historically elevated. Job openings fell by -3.7% in January to 10.82 million, a three-month low. While the number of open positions has come down from its peak level of 11.86 million in March 2022, it is still much higher than pre-pandemic when it was around 7.0 million.

The job openings-to-unemployed ratio ticked down only slightly to 1.90 from 1.96 in the prior month but remains close to the cycle peak of 1.99. Normal is considered 1.0 to 1.2.

On balance, these two reports suggest the labor market is still very tight but perhaps a little less so. Next up is the government’s BLS monthly labor report due this Friday, March 10th.

Source: Ned Davis Research, ADP Research Institute, Bureau of Labor Statistics, Bloomberg

One simple graphic

When stocks go up, we celebrate our paper gains and our expanding net worth. Great!

When stocks go down, we have the opportunity to buy even more shares at discounted prices. Also great!

Source: Brian Feroldi

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.