Equity flows remain depressed, plus the banner month for bonds, commercial real estate, and financial conditions ease

The Sandbox Daily (12.4.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

retail investor demand for equity funds remains depressed

banner month for bonds

commercial real estate maturity wall approaching

financial conditions in November ease most on record

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 +1.04% | Dow -0.11% | S&P 500 -0.54% | Nasdaq 100 -0.99%

FIXED INCOME: Barclays Agg Bond -0.38% | High Yield -0.25% | 2yr UST 4.633% | 10yr UST 4.257%

COMMODITIES: Brent Crude -0.84% to $78.22/barrel. Gold -1.98% to $2,048.4/oz.

BITCOIN: +5.41% to $41,842

US DOLLAR INDEX: +0.36% to 103.639

CBOE EQUITY PUT/CALL RATIO: 0.51

VIX: +3.56% to 13.08

Quote of the day

“Stock prices move around wildly over very short periods of time. This does not mean that the values of the underlying companies have changed very much during that same period.”

- Joel Greenblatt

Retail investor demand for equity funds remains depressed

As we approach year-end, the attention is inevitably drawn towards the outlook for next year.

With that forward-looking bias weighing on investor’s minds, one must consider a pending shift in flow data that has starved stocks of liquidity for two consecutive years. After all, many headwinds should shift into tailwinds in 2024 – including but not limited to further disinflation, a softening in monetary policy, and perhaps that elusive soft landing – all constructive reasons to support an inflow into equity markets.

Last year, we saw a sharp reversal in equity fund flows, including both mutual funds and ETFs, from a record high of ~$1.1tn in 2021 to just a paltry $5bn in 2022.

This year, we have seen a 2nd consecutive year of muted demand for equity funds, totaling just $24bn.

Source: J.P. Morgan Markets

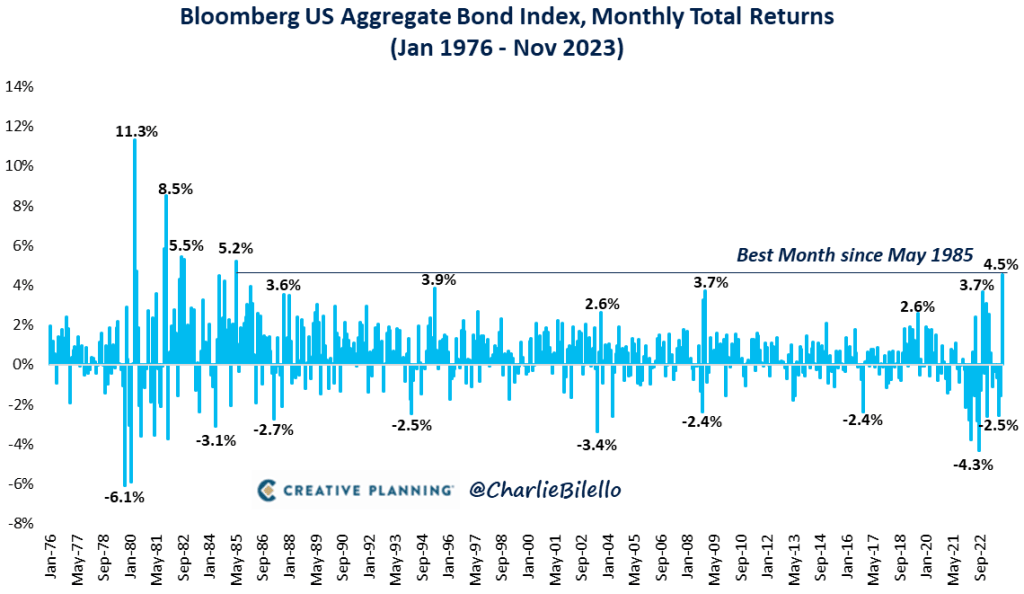

Banner month for bonds

The Bloomberg U.S. Aggregate Bond Index closed +4.5% higher in November, its best month since May 1985 and 8th best return since inception of the index in 1976.

The index measures the performance of U.S. Treasuries, Government-Backed Securities, Corporate Bonds, Mortgage-Backed Securities (MBS), Asset-Backed Securities (ABS), and Commercial Mortgage-Backed Securities (CMBS).

+4.5% for bonds may not sound like a lot compared to the S&P 500 index’s +8.9% gain for November, but the move was historic in respect to its own asset class.

The U.S. aggregate bond index has returned 4% or more in a month only 11 other times.

What’s more striking is the initial months of +4% gains were often followed by more gains on a go-forward basis over nearly every time horizon.

And, naturally, many investors are asking what the near-term implications are for the stock market after such a strong month for bonds, especially as we close out the books on 2023.

Here are the results:

The S&P 500 index exhibited strong performance after major bond rallies, ending the next month higher nine of eleven times with a median gain of +3.61%.

Source: Charlie Bilello, Dwyer Strategy

Commercial real estate maturity wall approaching

The U.S. commercial real estate sector has grappled with fundamental challenges this year: seismic secular shifts in commercial real estate utilization, diminished credit availability from banks, and high interest rates making debt service more burdensome for borrowers.

Compounding these problems, the commercial real estate debt market is facing a large wave of loan maturities, with many borrowers scheduled to repay a lump sum of principal amidst higher borrowing costs.

The scale of the current maturity wall is large on both an absolute and relative basis.

$1.2 trillion of commercial mortgages are scheduled to mature over the next two years, barring extensions.

Stated differently, almost a quarter of outstanding commercial mortgages are maturing in the next two years, the highest recorded level going back to 2008.

Banks are the largest holder of this maturing debt, with a 40% share.

The debt market has so far weathered these challenges better than many had expected, for two key reasons. First, lenders have worked with borrowers to modify and extend maturing loans that might otherwise go down the path of foreclosure. Second, the pressure has largely been concentrated on office properties, with fewer signs of deterioration for other property types.

Source: Goldman Sachs Global Investment Research

Financial conditions in November ease most on record

U.S. Financial Conditions eased 90 bps in November, the largest monthly easing on record (dating back to 1982). This cannot make the Federal Reserve happy.

Much of the change in the underlying components of the Goldman Sachs Financial Conditions Index was due to the retracement in bond yields, namely the monster decline in 10-yr yields.

Source: Bloomberg

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.