February: month in review

The Sandbox Daily (3.2.2026)

Welcome, Sandbox friends.

Today’s Daily discusses:

February market bites

Let’s dig in.

Blake

Markets in review

EQUITIES: Russell 2000 +0.90% | Nasdaq 100 +0.13% | S&P 500 +0.04% | Dow -0.15%

FIXED INCOME: Barclays Agg Bond -0.40% | High Yield -0.06% | 2yr UST 3.477% | 10yr UST 4.038%

COMMODITIES: Brent Crude +7.22% to $78.13/barrel. Gold +1.98% to $5,351.8/oz.

BITCOIN: +5.39% to $69,404

US DOLLAR INDEX: +0.95% to 98.54

CBOE TOTAL PUT/CALL RATIO: 0.84

VIX: +7.96% to 21.44

Quote of the day

“We are in the business of making mistakes. The only difference between the winners and the losers is that the winners make small mistakes, while the losers make big mistakes.”

- Ned Davis

February: month in review

February is a stark reminder to investors that markets don’t move in a straight line.

After January’s positive momentum carried major indices to new all-time highs, the mood shifted in the 2nd month due to a landmark Supreme Court ruling on tariffs, concerns around artificial intelligence, softer labor market data, and major escalations in the Middle East. Meanwhile, international stocks and small caps continued to outperform, and bonds saw further gains, highlighting the importance of holding a balanced portfolio.

While headlines can create short-term volatility, the overall economy remains healthy and corporate earnings continue to expand.

Key Market and Economic Drivers in February

• The S&P 500 fell -0.9% and the Nasdaq 100 dropped -2.3% for the month. Meanwhile, the Dow Jones Industrial Average rose +0.2% for its 10th consecutive monthly gain

• The VIX, a measure of stock market volatility, increased to 19.9 at the end of the month due to AI-related concerns and trade policy uncertainty

• International Developed Markets (DM) jumped +4.5% in US dollar terms based on the MSCI EAFE Index, while Emerging Markets (EM) gained 5.4% based on the MSCI EM Index. Year-to-date, they have gained +9.9% and +14.6%, respectively.

• The 10-year Treasury yield ended the month lower at 3.95%. This is the first month it has fallen below 4% since last November.

• Gold closed lower at $5,279 per ounce but reached as low as $4,661 at the beginning of the month amidst significant precious metals volatility

• January inflation showed headline CPI at 2.4% YoY and core CPI at 2.5%

• The unemployment rate edged down to 4.3% in January, with 130,000 nonfarm payroll jobs added. However, annual benchmark revisions showed the economy created only 181,000 jobs in all of 2025, roughly 15,000 per month.

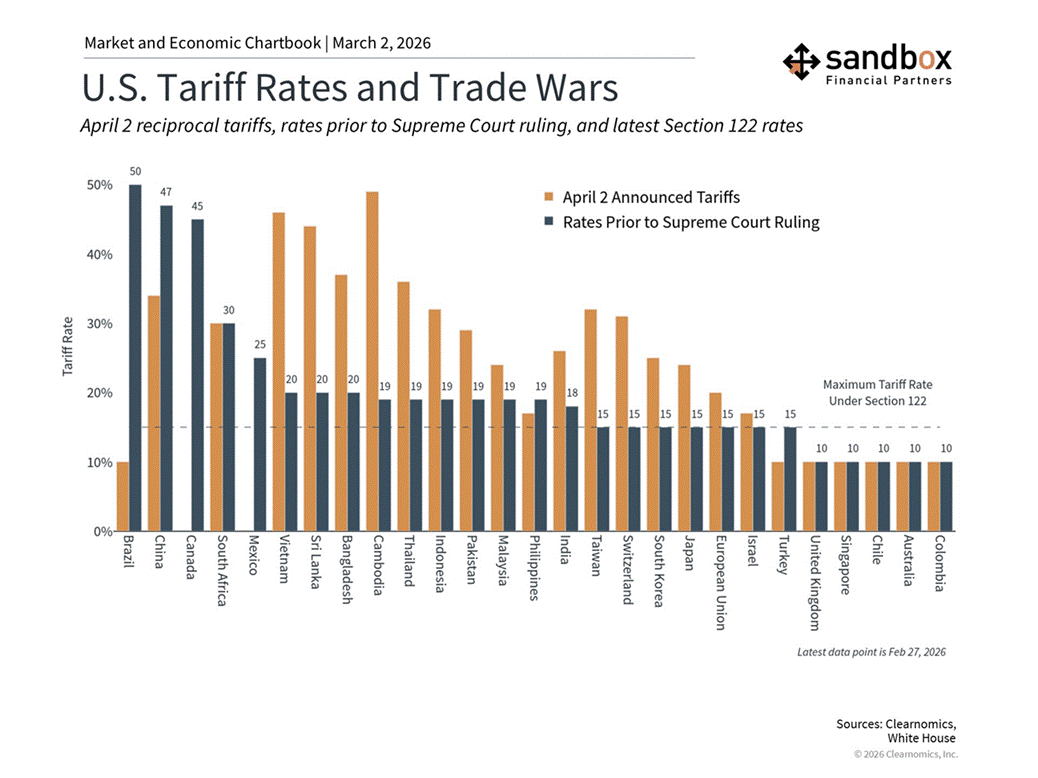

• On February 20, the Supreme Court ruled against the administration’s use of IEEPA-based reciprocal tariffs, prompting a pivot to alternative trade laws.

• On February 28, the U.S. and Israel launched military strikes against Iran, including the compound of Iran’s Supreme Leader who has been reported to be killed.

A Supreme Court ruling reshapes trade policy

The most significant policy development in February was the Supreme Court’s ruling on February 20th against the administration’s tariffs, which were originally enacted based on the International Emergency Economic Powers Act (IEEPA) to impose reciprocal tariffs against most trading partners.

Following the Supreme Court decision, the White House quickly adjusted tariffs based on another law, Section 122 of the Trade Act of 1974, which allows the President to impose tariffs of up to 15% for 150 days. These new import duties went into effect on February 24.

For investors, the key takeaway is that while the legal framework for tariffs has shifted, the policy direction has not. Trade uncertainty will continue to generate headlines and contribute to market volatility.

However, as history has shown, markets tend to adjust to new trade realities over time, especially as companies adapt their supply chains and pricing strategies.

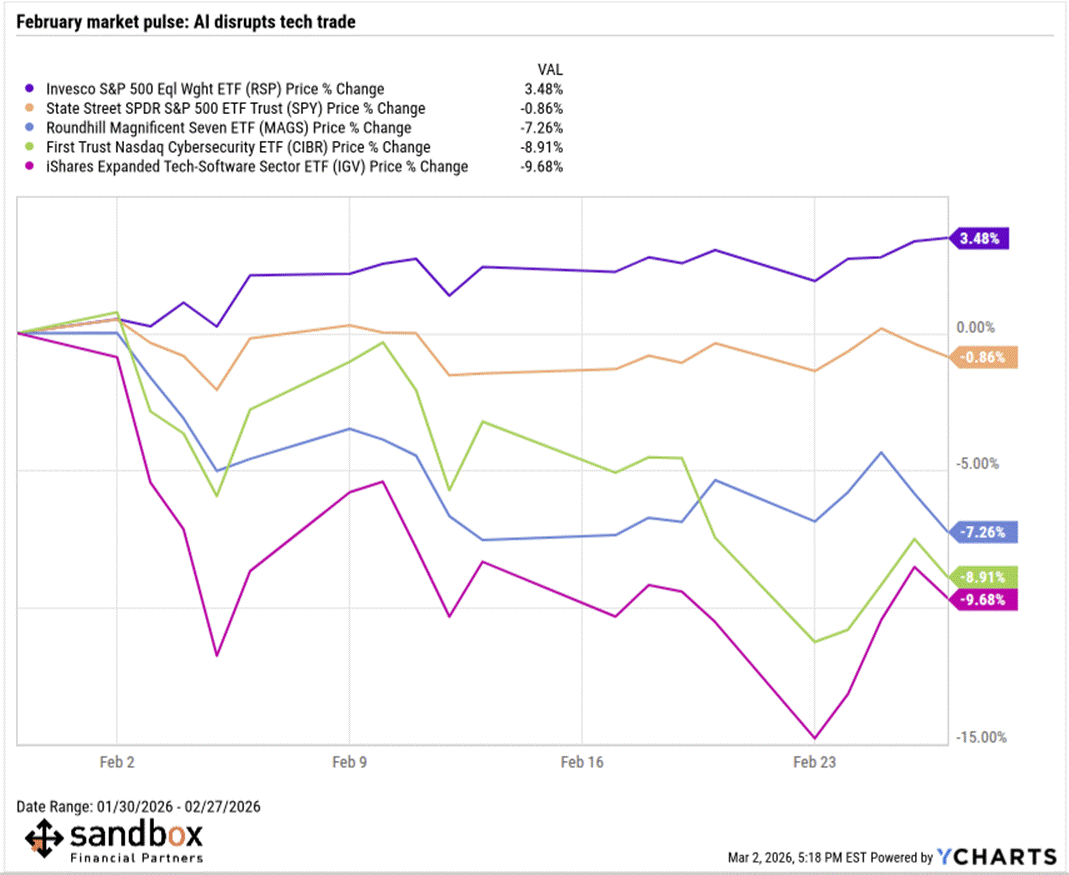

AI disrupts tech trade

AI continued to dominate market conversations in February, but the narrative shifted from high valuations to a debate about the pace and degree of disruption on existing business models.

Some investors worry that AI agents could compress software margins, accelerate white-collar displacement through automation, and disrupt traditional business models faster than expected.

These concerns have contributed to a notable market rotation.

Investors have been diversifying away from mega-cap technology stocks and toward sectors perceived as harder to displace – including energy, materials, and industrials. This shift, sometimes described as a move toward “heavy assets, low obsolescence” (HALO) companies, helps explain why Tech underperformed while other parts of the market rallied.

Growth cooled while the labor market sent mixed signals

According to the Bureau of Economic Analysis, real GDP increased at an annual rate of 1.4% in the fourth quarter of 2025, down from 4.4% in the prior quarter and below market expectations of 2.5%. The slowdown was partly due to the record-long government shutdown and a deceleration in consumer spending. However, business investment grew 3.7% on an annualized basis, driven by record-setting investments in AI data centers. For all of 2025, real GDP grew 2.2%, which remains healthy by historical standards.

Perhaps more concerning is the state of the labor market. While the unemployment rate edged down to 4.3% in January, annual benchmark revisions from the Bureau of Labor Statistics (BLS) painted a much weaker picture – roughly 900,000 jobs that were thought to be added from April 2024 to March 2025 were revised out of the data. In reality, the economy created just 181,000 jobs in 2025, translating to ~15,000 additions per month.

This has led some economists to describe the current environment as one of “jobless growth,” a situation where the economy expands but job creation fails to keep pace. The divergence between GDP growth and employment has been widening since mid-2022, and it raises questions about the underlying quality and breadth of the current expansion.

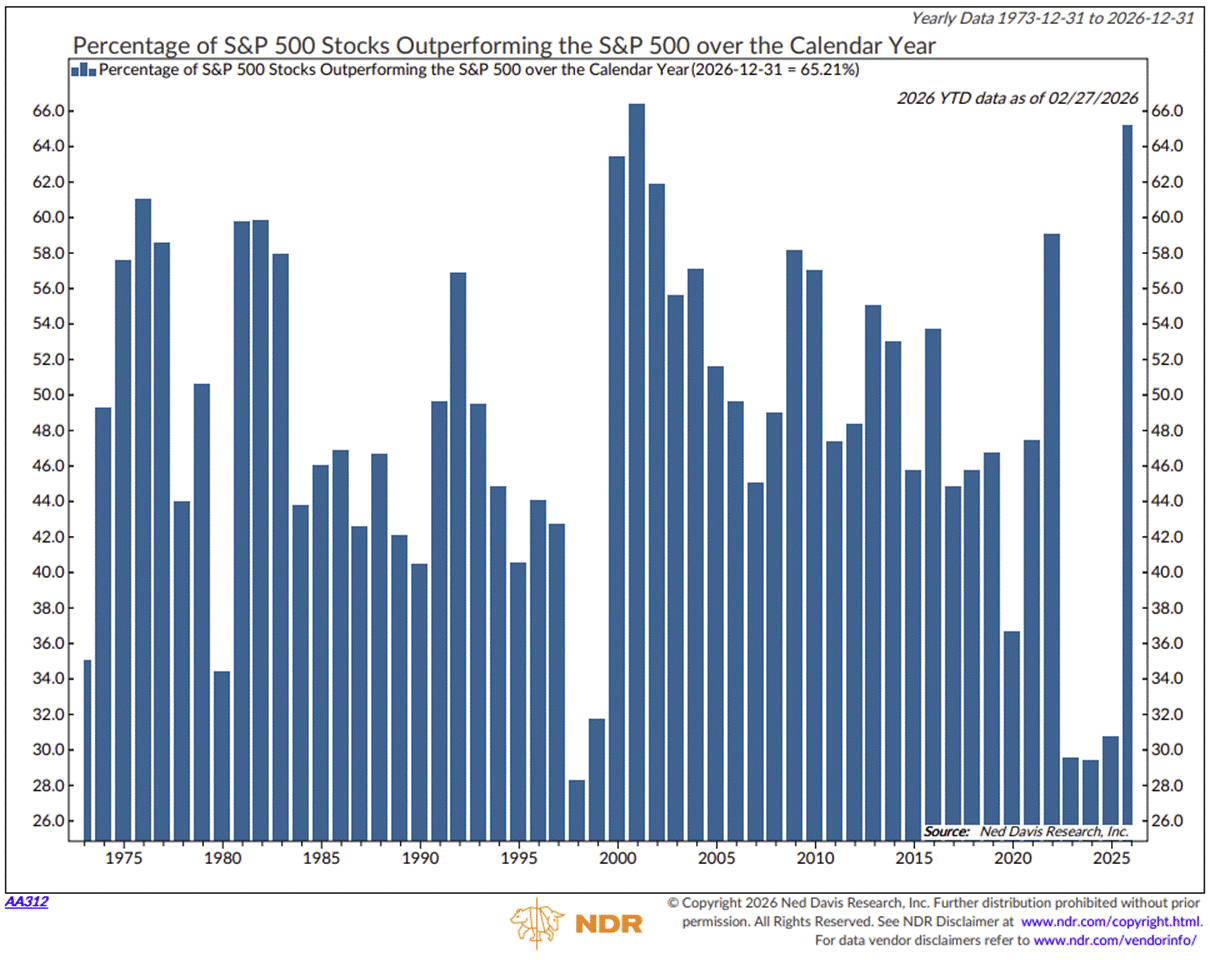

International stocks, mid/small caps lead the way

One of the most notable developments in February was the continued outperformance of asset classes beyond U.S. large-cap growth stocks.

This broadening of market returns is significant for diversified investors. After several years where only a small number of large U.S. technology companies drove the majority of market gains, the shift toward international stocks, mid- and small-caps, and cyclical sectors suggests that investors are finding opportunities across a wider range of assets.

Within the S&P 500, roughly 2/3rds of index constituents are outperforming the index itself year-to-date, an indication of widespread participation not seen since the early 2000s.

U.S.-Israeli forces conduct joint military operations in Iran

Another significant geopolitical development is unfolding in real time as joint U.S.-Israeli military operations culminated in strikes across Iran and the death of Iran’s Supreme Leader Ayatollah Ali Khamenei.

This triggered widespread retaliation from Iran and counterstrikes across the region. Iran has launched missiles and drones at Israel and Gulf nations hosting U.S. bases, with civilian infrastructure in places like Dubai and Abu Dhabi also hit. Casualties are mounting on both sides.

The Strait of Hormuz, through which ~14 million barrels per day flowed in 2025 (about 1/3rd of global seaborne crude exports), is the main concern. Tanker traffic has virtually stopped as companies exercise caution, with vessels backing up and Iran’s Revolutionary Guards issuing passage warnings (no formal closure confirmed). Duration matters most – a brief halt is digestible, but sustained conflict could pressure global supplies heavily.

The big question now is whether tensions de-escalate or spiral. President Trump suggested the conflict could last weeks but also hinted at potential talks, while Iranian officials publicly rejected negotiations. Global reactions remain divided, with Western allies largely backing the U.S. and China and Russia condemning the strikes.

Bottom line?

While AI and trade policy uncertainty continue to generate headlines, the broadening of market leadership is a positive development for long-term investors.

Sources: Clearnomics, YCharts, Bloomberg, Ned Davis Research, Chartr

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures (click here)

Please see our SEC Registered firm brochure (click here)

Please see our SEC Registered Form CRS (click here)