Fed Chair Jerome Powell's curtain call

The Sandbox Daily (4.28.2026)

Welcome, Sandbox friends.

Today’s Daily discusses:

Powell’s curtain call

Let’s dig in.

Blake

Markets in review

EQUITIES: Dow -0.05% | S&P 500 -0.49% | Nasdaq 100 -1.01% | Russell 2000 -1.15%

FIXED INCOME: Barclays Agg Bond -0.04% | High Yield -0.14% | 2yr UST 3.834% | 10yr UST 4.342%

COMMODITIES: Brent Crude +2.74% to $111.20/barrel. Gold -1.78% to $4,610.3/oz.

BITCOIN: -0.70% to $76,441

US DOLLAR INDEX: +0.12% to 98.62

CBOE TOTAL PUT/CALL RATIO: 0.86

VIX: -1.05% to 17.83

Quote of the day

“The longer you wait to take that chance in your life, the shorter the future is going to be when you arrive there.”

- Daniel Arsham

Powell’s curtain call

At tomorrow’s Federal Open Markets Committee (FOMC) meeting, expect the Federal Reserve to stay on hold – with little change in tone relative to March – amid the ongoing uncertainties from the Iran conflict, in line with market expectations.

Nobody expects the Fed to do anything anytime soon, as long as there is a high degree of uncertainty over conflict resolution in the Middle East. In the meantime, inflation readings will remain elevated, while the unemployment rate remains historically low.

That’s a recipe for the FOMC to sit on its hands.

After Kevin Warsh’s testimony during his recent confirmation hearing, the market broadly sees policy on hold through 2026 – with the next interest rate cut expected sometime in 2027.

I’d refrain from fading this pricing given it broadly reflects the current distribution of risks. It will likely take sustained evidence of labor market tightening before market expectations materially shift in favor of more rate cuts, something President Trump is desperately seeking.

Beyond the FOMC statement and policy decision, the more noteworthy headlines tomorrow will center on Fed Chair Jerome Powell’s legacy.

Now that the Department of Justice has dropped its criminal probe against Jerome Powell and with Senator Tillis clearing the way for Kevin Warsh’s confirmation, Wednesday’s press conference will almost assuredly be Powell’s last as Fed Chair.

Powell’s term as Chair ends on May 15, 2026 after eight years leading the central bank, although his term as a member of the Fed’s Board of Governors technically runs until January 31, 2028. Powell remains undecided if he stays after vacating his Chair seat.

Powell will undoubtedly be asked to reflect on his time as Fed Chair.

Here is a brief account of Powell’s tenure:

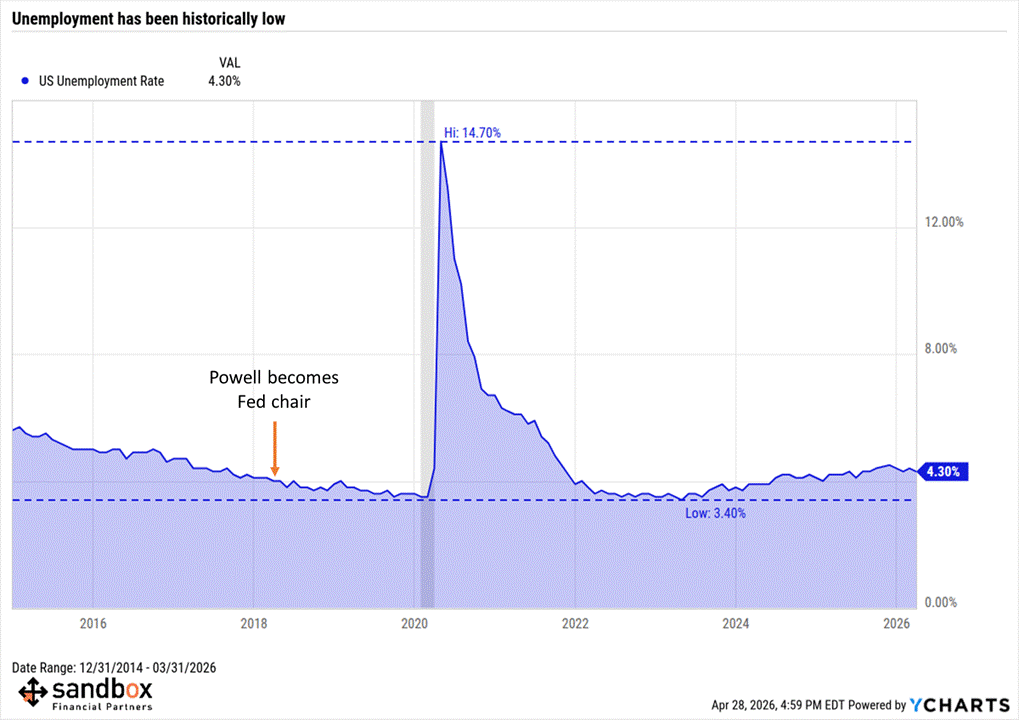

The good: unemployment has been historically low, outside a once-in-a-lifetime pandemic spike

Under Powell’s 1st two years as Fed Chair, unemployment was notably low.

That changed in April 2020, when the onset of the pandemic pushed the figure up to 14.7%, the highest since at least 1948, when the modern unemployment rate was first published – largely driven by business closures, furloughs, and layoffs.

Unemployment has since cooled, and has hovered around the low 4% range for the past few years – a number that’s historically low but still a touch higher than when Powell took over.

Labor force participation has also weakened, reaching its lowest rate since the 1970s in March, excluding the pandemic.

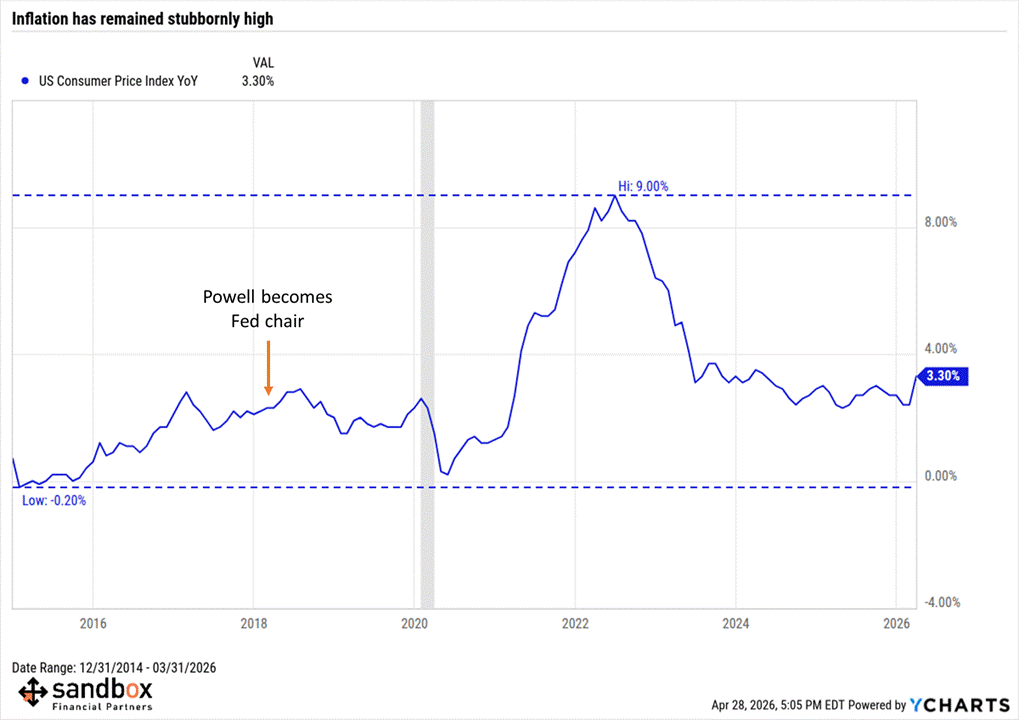

The bad: inflation has remained stubbornly high

Inflation has remained stubbornly high during Powell’s time as Chair, with a rapid rise in 2021 and 2022 driven by highly accommodative twin monetary and fiscal policies from the pandemic as well as otherworldly consumer demand.

The chaos of the last few years has added to inflationary trouble on the supply side as well. Inflation was boosted by supply chain disruptions and dislocations caused during covid-19, further exacerbated by the start of the Russia-Ukraine war and high oil prices.

The year-on-year CPI inflation rate rose from 1% in late 2020 to its peak of 9% in June 2022. It cooled down to the low 2% range at the start of 2026, but reaccelerated in March this year due to the Iran war.

In hindsight, it’s easy to armchair quarterback and say the Fed acted too slowly in response to early inflationary impulses despite the difficulties of a chaotic and historic economic reopening. Perhaps some of the collateral damage could have been contained but it’s shortsighted to believe it could have been avoided.

The market fallout ensued after the FOMC carried out its fastest interest rate hiking cycle in history once it began tightening.

Right or wrong, inflation will dog the perception of Powell’s legacy in the years to come.

The great preserver: stressing Fed independence

Tensions over the last year between the White House and the Fed have brought the topic of Fed independence sharply into focus.

This is because there can be a natural friction between elected officials and the Fed, since they each have unique goals and incentives.

For instance, the President and Congress often prefer lower interest rates to spur economic growth and help fund the federal budget. In contrast, the Fed may need to make difficult choices around issues such as inflation and financial stability, based on longer-term considerations.

Preservation of independence was a common theme during Kevin Warsh’s hearing as many elected officials believe it to be paramount for economic and market structure going forward.

Powell’s unwillingness to bend to President Trump’s (very public) threats and sham lawsuit beautifully preserved the appearance of independence to even Powell’s most ardent critics.

Job well done here.

Oh yeah, one final thought.

Expect a parting shot at the President. I’d set the odds at -250.

Source: YCharts

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures (click here)

Please see our SEC Registered firm brochure (click here)

Please see our SEC Registered Form CRS (click here)