Fed forecasts, investors warm up to risk, and cash comes off the sidelines

The Sandbox Daily (6.20.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

Fed’s forecasting abilities since the pandemic

investors warm up to risk

cash coming off the sidelines

NYC office occupancy hits 50% for 1st time since pandemic

consumer sentiment improves

housing starts surge

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 -0.09% | S&P 500 -0.47% | Russell 2000 -0.47% | Dow -0.72%

FIXED INCOME: Barclays Agg Bond +0.18% | High Yield -0.27% | 2yr UST 4.687% | 10yr UST 3.721%

COMMODITIES: Brent Crude -0.37% to $75.81/barrel. Gold -1.17% to $1,948.2/oz.

BITCOIN: +5.75% to $28,232

US DOLLAR INDEX: +0.01% to 102.537

CBOE EQUITY PUT/CALL RATIO: 0.46

VIX: -2.18% to 13.88

Quote of the day

“Stocks are the only thing that people are happy to buy when the price goes up.”

- Warren Buffett, Berkshire Hathaway

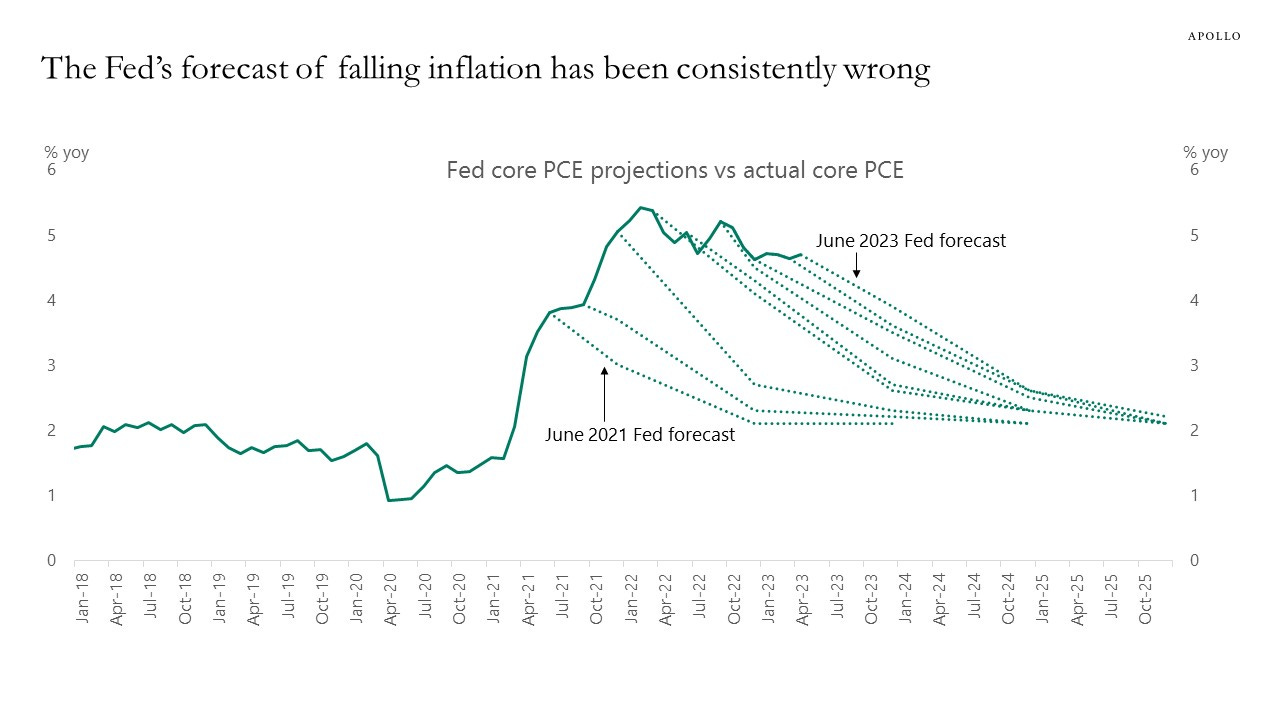

Fed’s forecasting abilities called into question

The latest Federal Open Markets Committee (FOMC) forecast from the Federal Reserve predicts that core inflation within a year will fall below 3%.

This has been the forecast for every Fed meeting over the past two years. And this forecast has been consistently wrong.

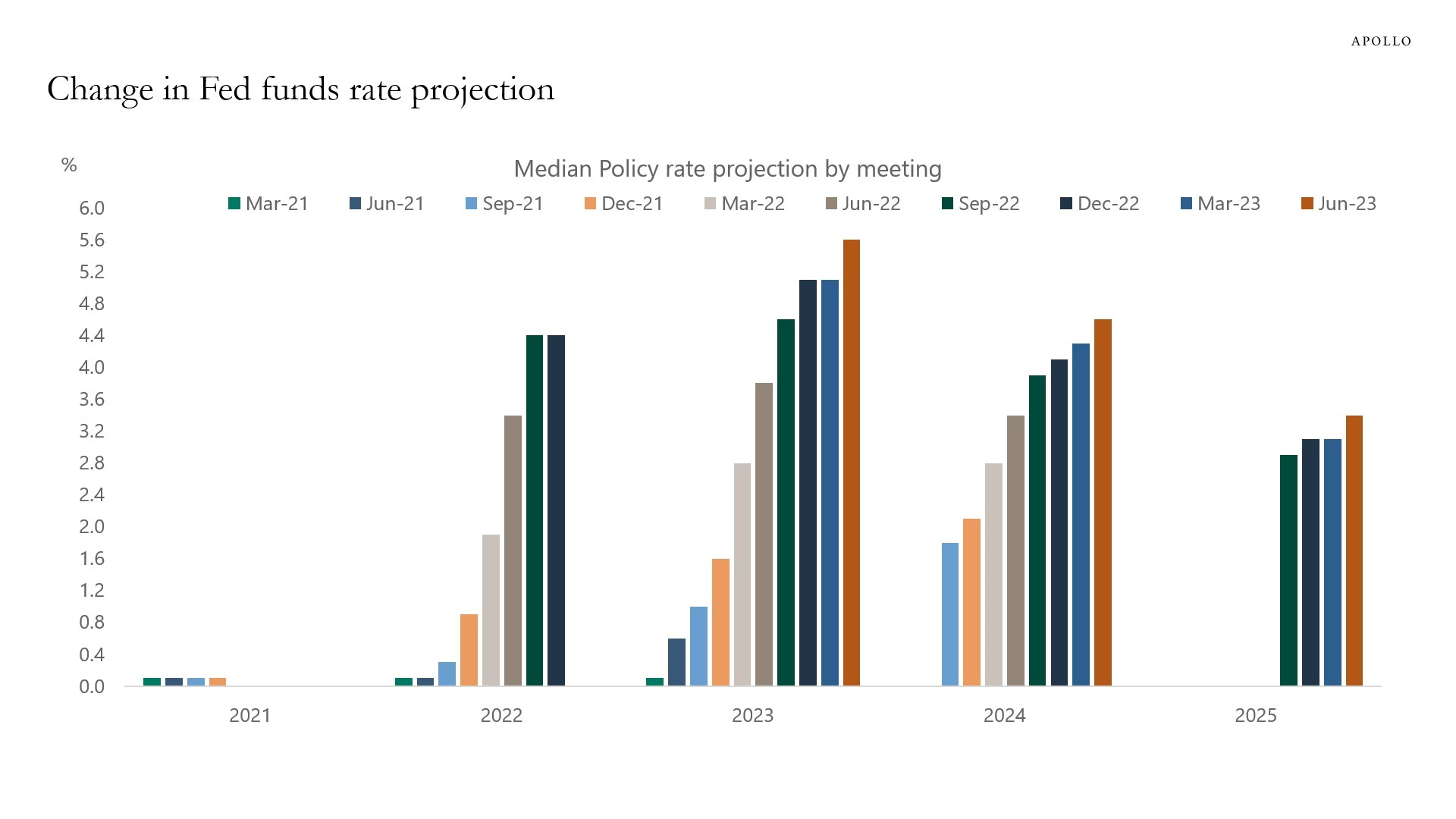

What about interest rates – has the Fed done a better job anticipating the future of the Fed Funds Rate, their primary tool to set monetary policy?

In March 2021, the FOMC believed that the Fed Funds Rate by the end of 2023 would be 0%, and today they think it will be 5.6%.

The late great Dr. Martin Zweig, a renowned investor and student of the markets, coined the phrase “don’t fight the Fed” in 1970 as he believed in the strong correlation between monetary policy and stock market returns.

Perhaps in this environment, economists and investors alike should be flexible with incorporating these future inflation and Fed Funds Rate projections into their market outlooks.

Source: Global Apollo Management

Investors warm up to risk

High-beta stocks are reaching new 52-week highs relative to low-volatility stocks this week.

One of the easiest metrics for gauging risk appetite is the High Beta (SPHB) vs. Low Volatility (SPLV) ratio. When this ratio is trending higher, it is because investors are favoring riskier stocks over their alternatives. On the flip side, low-volatility stocks outperform in uncertain times due to their defensive attributes.

The ratio of high beta (SPHB) vs. low volatility (SPLV) has been rising in a nearly vertical line since early May, reclaiming a critical level marked by its former highs from earlier this year.

As long as SPHB/SPLV holds above its breakout level, it would indicate a risk-on tone for the market and could support higher stock prices.

Source: All Star Charts

Cash coming off the sidelines

After seven consecutive weeks of inflows, money market funds experienced outflows of $33.52 billion.

Much of that cash made its way into U.S. equities, which drew their biggest weekly net buying since mid-February 2021. Investors allocated $18.85 billion to U.S. equity funds.

Source: Reuters, Goldman Sachs Global Investment Research

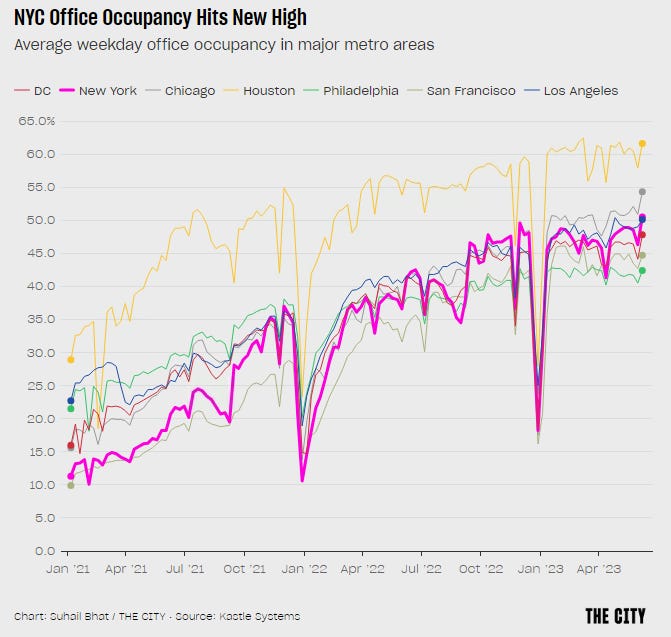

NYC office occupancy hits 50% for 1st time since pandemic

Office occupancy in the New York area exceeded 50% for the week beginning June 1. The increase in New York mirrored gains in the rest of the country.

Monitoring the return-to-office movement has major implications for commercial real estate, specifically office properties, which some estimate could be down by 30-40% from pre-pandemic levels.

Source: The City

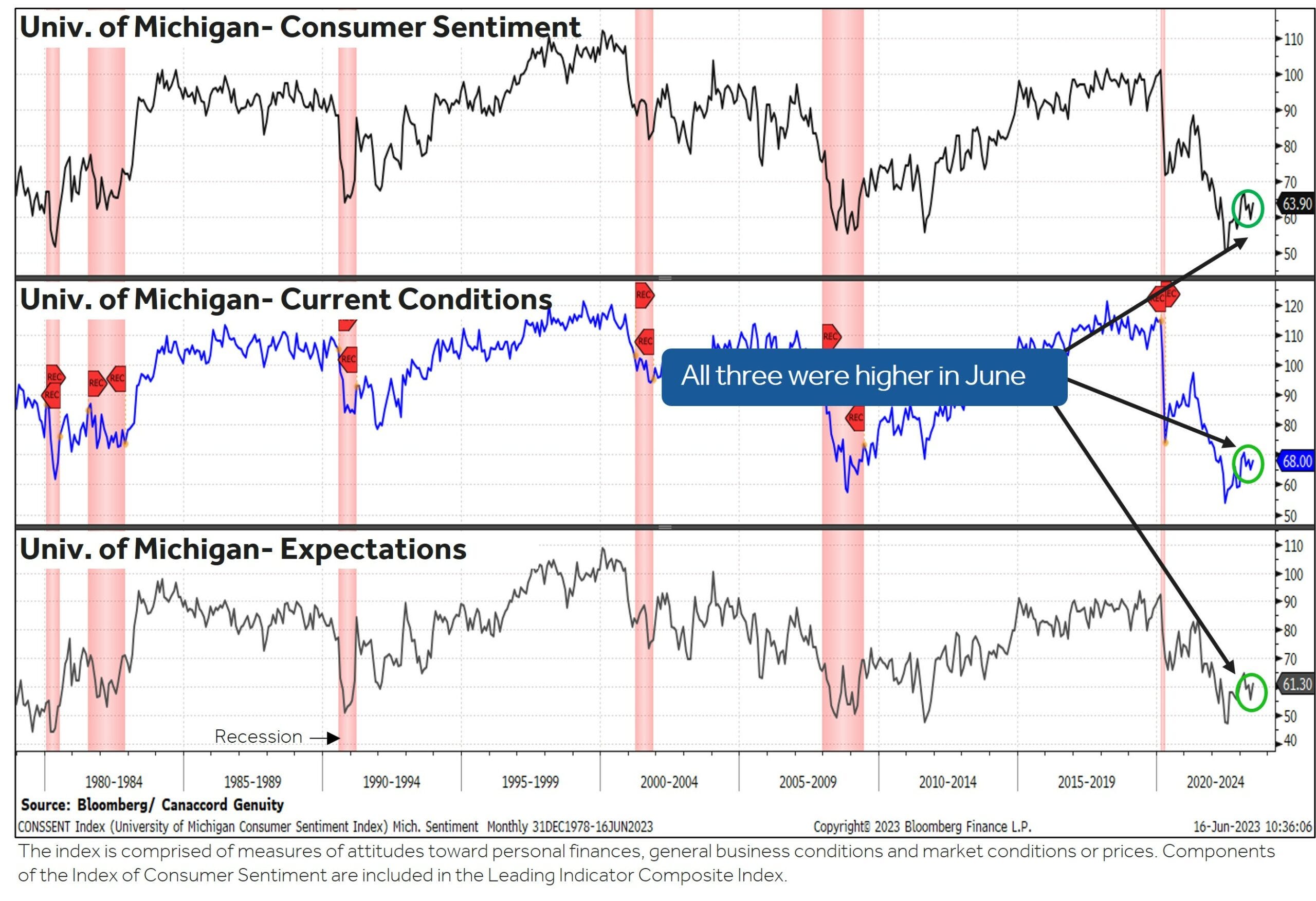

Consumer sentiment improves

The Reuters/University of Michigan Consumer Sentiment Index increased to 63.9 in the June preliminary reading, the highest level in four months and above forecasts of 60.

The latest figure reflects greater optimism on the back of the recent debt ceiling resolution and the disinflation narrative of 2023.

Consumer sentiment is now 27.8% above its historic record low one year ago, the biggest year-over-year gains since November 2012.

Source: Dwyer Strategy, Ned Davis Research

Housing starts surge

Privately owned U.S. housing starts surged 21.7% in May to a seasonally adjusted annualized rate of 1.631 million units, the highest level since April 2022 and way higher than the consensus expectations of 1.39.

It was the biggest monthly gain since October 2016, and the 8th largest gain on record.

Previous jumps of this magnitude have been followed, on average, by at least a partial reversal in the subsequent three months, which is a risk for the near-term. Nevertheless, both the 3-month and the 6-month averages of starts picked up in May, indicating a near-term trend improvement in construction activity.

This housing report, in conjunction with a solid beat on building permits, corroborates Federal Reserve Chair Jerome Powell’s comments last week that the housing market has shown signs of stabilizing. Homebuilders, which are responding to limited inventory in the resale market, have grown more upbeat as demand is firming, materials costs retreat, and supply-chain pressures ease.

Monitoring continuation of these upward trends into the 2nd half of 2023 may indicate if residential housing construction activity has bottomed.

Source: Trading Economics, Bloomberg

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.