Fed pause a reason for optimism? plus dividend yields, orange juice prices, and market valuation

The Sandbox Daily (5.30.2024)

Welcome, Sandbox friends.

Today’s Daily discusses:

the Fed pause a reason for optimism?

dividend yield attractiveness has fallen

why are orange juice prices soaring?

market valuation in line with history

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 +1.00% | S&P 500 -0.60% | Dow -0.86% | Nasdaq 100 -1.06%

FIXED INCOME: Barclays Agg Bond +0.47% | High Yield +0.40% | 2yr UST 4.927% | 10yr UST 4.548%

COMMODITIES: Brent Crude -1.97% to $81.95/barrel. Gold -0.05% to $2,362.8/oz.

BITCOIN: +1.77% to $68,425

US DOLLAR INDEX: -0.31% to 104.778

CBOE EQUITY PUT/CALL RATIO: 0.68

VIX: +1.33% to 14.47

Quote of the day

“Our life is the sum total of all the decisions we make every day, and those decisions are determined by our priorities.”

- Dr. Myles Munroe, Bahamian Evangelist

The Fed pause a reason for optimism?

Even as the Federal Reserve maintains rates at a “higher-for-longer” level, markets can still perform well during periods of Fed pauses – i.e. after the final rate hike and before the 1st rate cut.

Over the last six rate-cutting cycles, markets returned an average of +9.2% during these pause periods.

As long as economic growth remains on trend, there’s no reason the current pause should be meaningfully different.

Source: iCapital

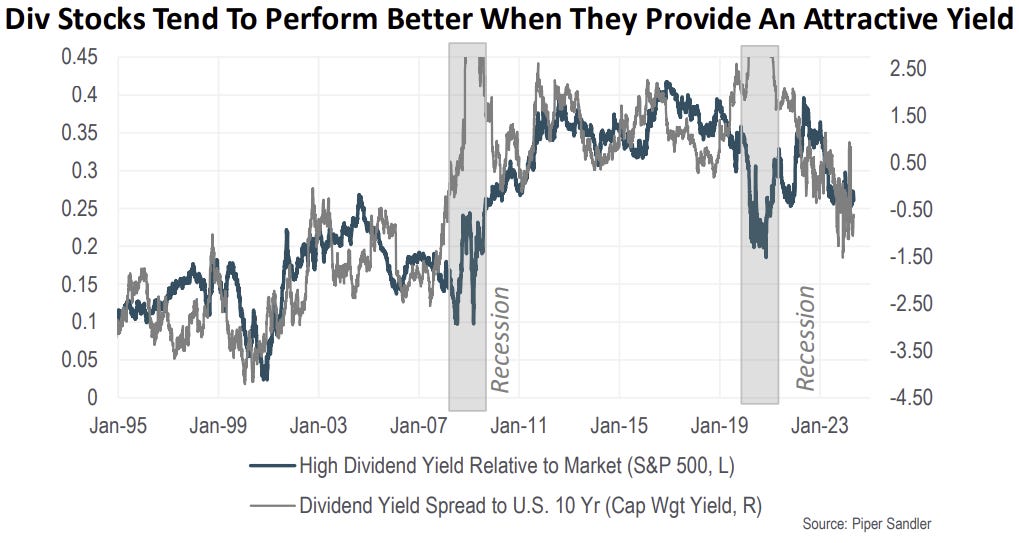

Dividend yield attractiveness has fallen

For investors seeking income, there is once again a risk-free alternative to dividend yield. The days of zero-interest rate policy (ZIRP) and the hunt for yield are long gone, leaving high dividend paying stocks low in demand.

The surge in interest rates over recent years means that less than 10% of the S&P 500 pays a dividend yield above the 10-year Treasury rate.

Over time, high dividend yielding stocks tend to outperform in periods where the dividend is increasingly attractive vs. Treasury yields.

Fed rate cuts would likely cause high dividend yielding stocks to be incrementally more attractive relative to bonds.

Source: Piper Sandler

Why are orange juice prices soaring?

Orange juice prices have gone vertical in recent months, climbing to fresh all-time highs amid persistent supply constraints.

The benchmark frozen concentrated orange juice futures, traded on the Intercontinental Exchange in New York, closed at $4.92 per pound on Tuesday. That’s nearly double the price registered a year ago.

Crippling shortages from two key regions have raised fears of a price rise that will hit consumers and likely reshape the global orange juice industry over the coming years.

Orange juice futures – which allow industry players to hedge against swings in prices – have been on a tear since the end of 2022 when a hurricane, then a cold snap, devastated acres of orange groves in Florida, the main growing region in the United States, the world’s 2nd-biggest producer.

But the rally has accelerated sharply this month as the prospect of a dismal harvest in Brazil has panicked the market. The world’s largest producer, Brazil, reported a meager outlook for 2024 production volumes, with some estimates showing this year’s harvest could be down ~24% from last year as the South American country’s main orange-producing areas, Sao Paulo and Minas Gerais, deal with an unprecedented heatwave.

Source: Jay Kaeppel, CNBC

Market valuation

Since 1937, whenever the 10-year U.S. Treasury rate is between 4% and 5% – as it has been for most of the time since August 2023 – the most prevalent market multiple for the S&P 500 index is 18x forward earnings or more – occurring 68% of the time.

What’s more, 49% of the time do we find the median P/E multiple is 20/x forward earnings when rates oscillate between 4% and 5%.

Too many people have said the stock market must come down because the 10-yr rate is hovering around these general levels. History would say otherwise.

Source: Fundstrat

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.