Fed raises rates by 0.75%, plus the Dow's best October ever, ADP employment report, sector performance, Twitter's new biz model, and inflation-linked savings bonds get a reset

The Sandbox Daily (11.2.2022)

Welcome, Sandbox friends.

Today’s Daily discusses the Federal Reserve’s decision to raise short-term interest rates by another 0.75%, the best October for the Dow Jones ever, the ADP private payrolls report for October, sector performance since the rate hiking cycle began, Twitter's new business model, and rate reset on inflation-linked U.S. Series I savings bonds.

Let’s dig in.

Markets in review

EQUITIES: Dow -1.55% | S&P 500 -2.50% | Russell 2000 -3.36% | Nasdaq 100 -3.39%

FIXED INCOME: Barclays Agg Bond -0.17% | High Yield -0.91% | 2yr UST 4.631% | 10yr UST 4.115%

COMMODITIES: Brent Crude +0.84% to $95.57/barrel. Gold -0.54% to $1,642.0/oz.

BITCOIN: -1.36% to $20,234

US DOLLAR INDEX: +0.56% to 111.967

CBOE EQUITY PUT/CALL RATIO: 1.14

VIX: +0.19% to 25.86

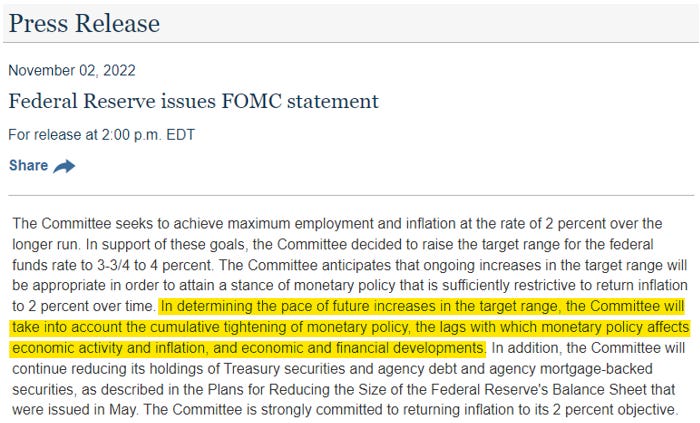

Fed raises target interest rate by another 0.75%

As widely expected, Federal Reserve Chairman Jerome Powell announced today the Fed’s unanimous decision to lift the target for the benchmark federal funds rate to a range of 3.75% to 4.00%, its highest level since 2008. Chair Powell stated interest rates will go up more than expected, and the path there could involve smaller hikes, while also noting it would be appropriate to slow the pace of increases “as soon as the next meeting or the one after that.”

The Fed made one major adjustment (highlighted) to their monetary policy statement that most certainly caught the market’s attention:

Sam Ro had this to say in response to the tweak in the Fed’s language and forward guidance:

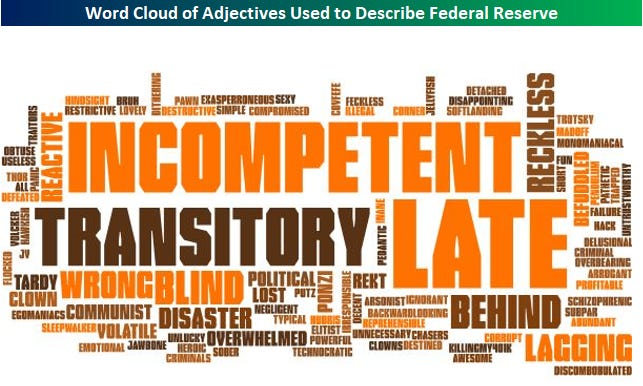

Of course, the Fed is behind the inflation curve and desperately trying to stomp out the persistence of higher prices – leading many prominent voices in Wall Street to suggest the Fed has lost their credibility. In fact, Bespoke Investment Group recently polled their subscribers to describe the Federal Reserve in one word. These answers highlight this deteriorating credibility narrative.

Source: Federal Reserve, Bloomberg, Sam Ro, Bespoke Investment Group

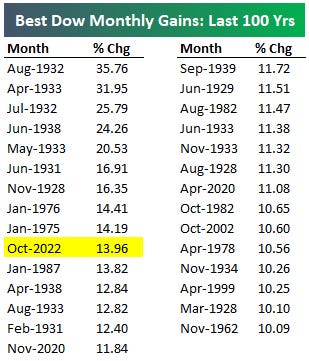

The best October for the Dow ever

The Dow Jones Industrial Average began trading on May 26, 1896, and it just had the best October return ever, returning +13.96%. This was the best monthly gain since January 1976 and its 10th best month of the last 100 years.

So, what does the huge month mean for stocks? Looking at all the +10% monthly gains for the Dow going back to World War II showed that future strength is quite possible, if not likely. Up more than +10% on average six months later and up close to +16% a year later should comfort investors.

Couple this good news with the fact that these next six months in a midterm year have been higher 18 of the last 18 times, which is another feather in the cap of the bulls.

Source: Carson Group, Bespoke Investment Group

ADP private payrolls show signs of easing

ADP private payrolls increased 239,000 in October, the most in three months, and above the consensus of 195,000. Nearly 90% of it, however, was concentrated in leisure/hospitality, which added 210,000 net new jobs. Payrolls in most other industries declined from the prior month, as businesses have started to pull back on hiring.

Notably, manufacturing, which tends to be more cyclical and interest rate sensitive than other industries, cut 20,000 jobs, down for the second consecutive month. Additionally, jobs in some services industries have already been declining for three or more successive months. Information payrolls, a reflection of the challenges in the tech sector, fell 17,000 last month, the second most since July 2020.

Annual pay growth eased slightly, but continues to run much higher than earlier in this cycle. Pay growth for job changers moderated for the 3rd consecutive month to +15.2% YoY, but is still about double the pay growth for job stayers which was little changed at +7.7% YoY. These trends suggests that while Fed tightening may have started to ebb labor demand, the Fed’s job is not yet done, as strong pay growth may keep inflation pressures elevated for longer.

Source: ADP National Employment Report, Ned Davis Research, Bloomberg

Sector performance since rate hikes began

The S&P 500 is down a little more than -12% since the close on March 16th after Fed Chair Powell hiked rates off the zero bound for the first time of this cycle. Including today’s rate hike, the Federal Reserve has hiked the fed funds rate 375 basis points thus far in 2022.

Looking at the S&P 1500, which includes large-caps, mid-caps, and small-caps, the average stock in the index is down -7.1% since the close on March 16th after the first rate hike. As shown below, Real Estate stocks (REITs) have been hit the hardest by the rate hikes with the average stock in the sector down -20.6%. Communication Services stocks are down the second most with an average decline of -18.4%. On the upside, we’ve seen two sectors average gains since the Powell rate hike cycle began: Energy (+24.8%) and Consumer Staples (+5.6%).

Source: Bespoke Investment Group

Twitter's new business model

On Tuesday, self-titled Chief Twit Elon Musk tweeted "Power to the people! Blue for $8/month" – all but confirming that a subscription model, in which users could pay $8 per month for a verified blue checkmark, is likely coming. As details emerge on what the new Twitter will look like, it’s interesting to explore what it might mean for business metrics on a go forward basis.

If every single currently-verified user signed up to pay, but no others, that would be worth a paltry $40mm a year to Twitter. If the company successfully convinced 10% of their 229m monthly active users to pay the proposed $8/month fee, Twitter would generate $2.3bn in revenue — a much more substantial sum, but still less than half of the $4.5bn they made in ad revenue last year. Even in a leaner version of Twitter, it's hard to see a future without ads.

Source: Chartr

Rate on U.S. Series I savings bonds resets to 6.89%

The U.S. Treasury’s popular inflation-linked Series I savings bonds will now yield 6.89% over the next six months, down from a record 9.62%.

I bond rates reset every six months at the beginning of May and November, with the rate pegged to a fixed rate (0.40%) and to a Consumer Price Index inflation-linked variable rate (6.49%), which is obviously the larger, more substantial component of the I bond savings rate. Investors had flooded into these Series I savings bonds to get the 9.62% rate before it expired on Friday, buying about 1 billion dollars worth of the bonds on Friday alone and crashing the Treasury Direct website, which is the only place to buy them. For context, the total issuance of I bonds from 2018 through 2020 equaled the amount purchased last Friday alone! Investors want to lock in these high rates before CPI rolls over meaningfully.

The new 6.89% rate is still the third-highest rate since I bonds debuted in 1998.

Source: TreasuryDirect

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.