Fewer C-Suites mention "recession," plus bear market in diversification, delinquencies, and Nvidia's stock split

The Sandbox Daily (6.10.2024)

Welcome, Sandbox friends.

Apple ($AAPL) debuted Apple Intelligence at the WWDC keynote address today and is integrating ChatGPT into the iPhone via Siri, Norway’s sovereign wealth fund (“Government Pension Fund Global”) will use its 0.98% stake in Tesla ($TSLA) to vote against Elon Musk’s proposed hefty CEO compensation package, and Berkshire Hathaway ($BRKB) purchases over 2.5 million shares of Occidental Petroleum ($OXY) to add to its existing 28% stake in the company.

Today’s Daily discusses:

fewer “recession” mentions for 7th straight quarter

bear market in diversification

one clear sign that monetary policy is restrictive

Nvidia’s stock split and the mixed historical impact of corporate splits

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 +0.39% | S&P 500 +0.26% | Russell 2000 +0.25% | Dow +0.18%

FIXED INCOME: Barclays Agg Bond -0.08% | High Yield +0.09% | 2yr UST 4.885% | 10yr UST 4.467%

COMMODITIES: Brent Crude +2.71% to $81.79/barrel. Gold +0.06% $2,326.4/oz.

BITCOIN: -0.16% to $69,549

US DOLLAR INDEX: +0.24% to 105.136

CBOE EQUITY PUT/CALL RATIO: 0.58

VIX: +4.26% to 12.74

Quote of the day

“Be more concerned with your character than your reputation, because your character is what you really are, while your reputation is merely what others think you are.”

- John Wooden, Former UCLA Men's Basketball Head Coach

Fewer “recession” mentions for 7th straight quarter

As the economy continues to run at trend growth and signs of an economic slowdown have not materialized, fewer and fewer C-Suites across America have mentioned the term “recession” during their earnings announcements.

In fact, the 29 callouts of the term “recession” during Q1 earnings season marks the 7th sequential quarter of fewer mentions – well below the 5-year average of 83 and 10-year average of 60.

Source: FactSet

Bear market in diversification

Broadly diversified portfolios have trailed the U.S. large-cap stock index in 13 of the last 15 years, a stretch seen only once before in almost a century of data, per Cambria.

Meb Faber, respected in many circles as a fund manager, thought leader, and podcaster, had this to say about the futility of diversification over recent years:

“If your neighbor has all their money in the S&P, then you look like a moron.”

Source: Cambria Funds, Bloomberg

One clear sign that monetary policy is restrictive

Plenty of evidence exists that shows monetary policy is restrictive, which continues to be a lively debate from policymakers, economists, investment strategists, and everyone in-between.

One clear sign that shows policy is restrictive is the recent uptick in delinquency rates across consumer loans.

Led by credit cards, the consumer delinquency rate rose for the 10th consecutive quarter, climbing 7 bps to 2.68% (top pane below), the most since Q3 2012. The delinquency rate on cards was the most since Q4 of 2011 (middle pane).

FDIC reported a “material deterioration” in credit card portfolios.

The good news is that the rate of increase in delinquencies has slowed.

The other good news? Delinquencies are trending higher, but it’s coming off a historically low base and remain in line with pre-pandemic levels.

Source: Ned Davis Research

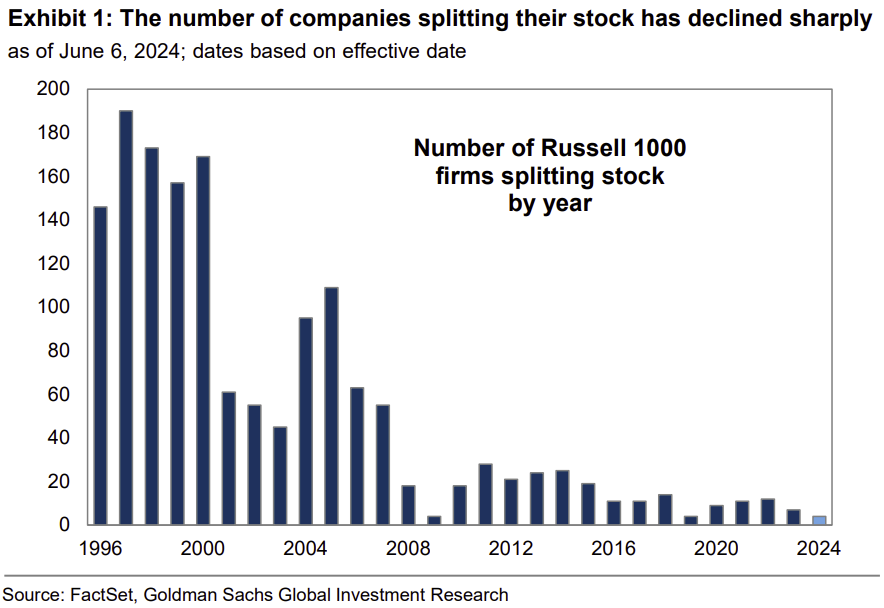

Nvidia’s stock split and the mixed historical impact of corporate splits

Nvidia ($NVDA) began trading today after its previously announced 10-for-1 stock split.

A stock split is a decision by a company’s board to increase the number of outstanding shares in the company by issuing new shares to existing shareholders in a set proportion. Stock splits come in multiple forms, but the most common are 2-for-1, 3-for-2, or 3-for-1 splits. In Nvidia’s case, this meant existing shareholders received 10 shares for each 1 share they previously held (10-for-1).

It’s important to note a stock split does not change a company’s value, but rather adjusts its share price lower as an offset to the increase in share count – which often manufactures renewed interest from retail investors who find a lower stock price more appealing for purchase. The increased activity of retail investors in recent years incentivizes corporates to increase the accessibility of their shares.

From time to time, stock splits are followed by a bump in stock performance – but not always. Let’s dive into those numbers, but first a brief history of stock splits.

Roughly 15% of Russell 1000 firms split their stock each year during the late 1990s Tech Bubble, but that has declined to an average of just 1% since 2017. Four Russell 1000 stocks have completed stock splits so far this year: $WMT, $COO, $TPL, $ODFL. Many of the mega-cap technology stocks have also split their stocks in recent years, including AAPL (2020), AMZN (2022), TSLA (2020, 2022), and GOOGL (2022).

Based on 46 Russell 1000 stock splits since 2019, share prices typically rose by 4% in excess of the equal-weight S&P 500 return in the week after the announcement, but prices did not evidence a clear reaction in subsequent weeks or months around the effective date.

The Yahoo! Finance team performed a similar analysis but used the S&P 500, a slightly longer time horizon, and focused on absolute returns (not relative).

“On average, stocks rise 25% in the 12 months following the announcement of their split compared to an average return of 12% from the S&P 500 in the same time frame, per analysis from Bank of America.”

Last week, Nvidia topped $3 trillion in market value, surpassing Apple. Microsoft is also a member of the exclusive $3 trillion club. Those three stocks now account for more than 20% of the value of the S&P 500 index.

Source: Goldman Sachs Global Investment Research, Yahoo Finance, Hartford Funds, Nvidia

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.