Future Proof, plus submerging markets and a brief recap of the trading week

The Sandbox Daily (9.8.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

Future Proof in Huntington Beach, CA

submerging markets

a brief recap to snapshot the week in markets

*** Editor’s note: The Sandbox Daily will be lightly posting content Monday-Wednesday next week while we are in Huntington Beach, California. Expect the full newsletter to return on Thursday, September 14th.

Let’s dig in.

Markets in review

EQUITIES: Dow +0.22% | S&P 500 +0.14% | Nasdaq 100 +0.14% | Russell 2000 -0.23%

FIXED INCOME: Barclays Agg Bond +0.05% | High Yield -0.04% | 2yr UST 4.989% | 10yr UST 4.261%

COMMODITIES: Brent Crude +0.58% to $90.44/barrel. Gold +0.01% to $1,942.6/oz.

BITCOIN: -0.12% to $25,893

US DOLLAR INDEX: -0.02% to 105.056

CBOE EQUITY PUT/CALL RATIO: 0.81

VIX: -3.89% to 13.84

Quote of the day

“One of the funny things about the stock market is that every time one person buys, another sells, and both think they are astute.”

- William Feather

Future Proof, here we come!

We are heading out west to Huntington Beach, California for the 2nd installment of Future Proof, a wealth management conference consisting of speaking panels, live podcasting, and product and service demos from the industries’ most well-respected thought leaders, independent research firms, technology developers, and service providers. All events are held outdoors along the beach on Pacific Coast Highway. The conference experience is like no other.

Below is the Future Proof promotional poster highlighting all the influential speakers at this year’s event.

Last year was so much fun – learning from the brightest minds in finance, meeting others in an intimate setting, and sharing ideas both new and old – that we are running it back for Year 2.

If you are attending Future Proof, please say hi!

More information can be found at the Future Proof website.

Source: Future Proof

Submerging markets

The majority of stock market indexes are in uptrends. Emerging Markets, however, are not in an uptrend – they’ve been rangebound all of 2023 and remain stuck below last summer’s highs.

Here is a chart of the MSCI Emerging Markets Index ETF (EEM) that shows a boat lost at sea:

Two things stand out:

1) In a year in which the U.S. dollar index has meaningfully come off the boil, emerging markets have surprisingly not caught a bid.

2) China’s market, which comprises 30% of the geographical exposure of the Emerging Markets index, has not taken a leadership role in the way many investors expected after the Chinese Communist Party abandoned their zero-COVID policy late last year.

Why be overweight a market segment that isn’t going up while the rest of the market is? Why make things more complicated than they need to be?

Source: BlackRock

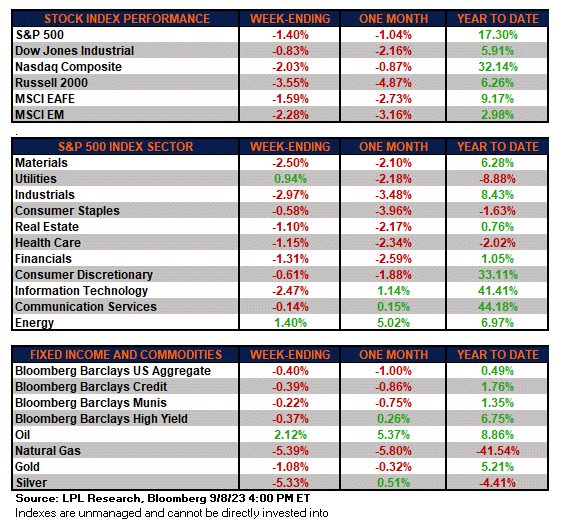

The week in review

Talk of the tape: Soft-landing expectations are the key driver of the bullish narrative. Disinflation traction cited as another tailwind. Consumer resilience, although showing some signs of fatigue, continues to be a higher-profile bright spot. The 2H23/2024 earnings rebound and record amount of money market assets on the sidelines flagged as some of the other bullish drivers.

The backup in interest rates, liquidity headwinds, the lagged effects of policy tightening, and extended valuations are talking points among the bearish narrative. The higher-for-longer Fed another overhang as markets reprice Fed Funds Rate expectations for year-end 2023 and 2024. Seasonal headwinds shouldn’t be dismissed. Geopolitical scrutiny on select tech names surfaced this week with startling news out of China, while the recent macro data reported from China confirm the risk to global growth.

Stocks: The major market indexes pulled back this week as investors continue to weigh the Fed’s next moves amid a resilient economic landscape. China’s crackdown on government use of Apple’s iPhone this week roiled markets, with the stock shedding hundreds of billions in market cap; Apple represents 11.4% of the Nasdaq 100, 7.5% of the S&P 500, and 3.6% of the Dow Jones Industrial Average.

Bonds: The Bloomberg Aggregate Bond Index ended the week lower, struggling to maintain its footing as investors believe the Fed could maintain its hawkish sentiment longer than anticipated. Credit spreads, or the additional compensation for owning more risky corporate debt, continue to shrug off bad news.

Commodities: Crude oil ended the week positive as commodities struggled. The recent rally in energy is underpinned by tightening supply expectations following Saudi Arabia and Russia’s decision to extend their production cuts until December, at the same time world oil demand is scaling at record highs according to the International Energy Agency. Meanwhile, precious metals (gold and silver) finished the week lower.

Source: Dwyer Strategy, LPL Research

That’s all for today.

Have a great weekend and see you next week!

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.