Global recalibration, plus December seasonality, a healthy U.S. consumer, and Batman

The Sandbox Daily (12.16.2024)

Welcome, Sandbox friends.

This is the final full trading week in 2024. We’re watching the Dow’s skid in the red reach eight consecutive trading sessions, the December (and final) FOMC meeting and presumed interest rate cut on Wednesday, triple witching on Thursday (stock options, index options, and index futures all expire simultaneously), and the Fed’s preferred inflation gauge (PCE) on Friday.

Today’s Daily discusses:

global “recalibration”

December seasonality on alert

a healthy U.S. consumer

BATMMAAN

Let’s dig in.

Blake

Markets in review

EQUITIES: Nasdaq 100 +1.45% | Russell 2000 +0.64% | S&P 500 +0.38% | Dow -0.25%

FIXED INCOME: Barclays Agg Bond +0.09% | High Yield +0.19% | 2yr UST 4.253% | 10yr UST 4.403%

COMMODITIES: Brent Crude -0.95% to $73.78/barrel. Gold -0.20% to $2,670.4/oz.

BITCOIN: +3.23% to $106,168

US DOLLAR INDEX: -0.12% to 106.871

CBOE TOTAL PUT/CALL RATIO: 0.84

VIX: +6.37% to 14.69

Quote of the day

“You never know the value of a moment until it becomes a memory.”

- Dr. Suess

Global “recalibration”

2024 has been a solid year for the global economy, with real GDP expected to rise by more than 3%. Despite continued resiliency in the U.S. economy, investors have observed uneven growth in Europe and China.

Global growth should remain robust in 2025.

With three-quarters of the world’s central banks now in easing cycles – up from one-quarter a year ago – easier monetary policy should help boost the expansion next year.

Central Banks around the world are easing off their aggressive stance, as policymakers have (mostly) lowered inflation within sight of their targets. Now, each is attempting to delicately steer their economies towards the so-called soft landing.

Keep rates too high for too long and risk excessive damage – such as a spike in unemployment – by unnecessarily self-inducing economic recession.

Instead, officials are responding to the data – as they should – and are lowering rates to remove their restrictive monetary biases.

The pivot has important ramifications as it eases global financial conditions. Manufacturing, housing, and automobile sales can all shake free from their own localized comas. C-Suites, after preparing for Jamie Dimon’s economic “hurricane,” can greenlight CapEx plans that were shelved over the last few years. The credit creation cycle can thaw.

And this pivot is happening everywhere.

Source: Ned Davis Research

December seasonality on alert

While history doesn’t always repeat itself, it often tends to rhyme. We can use seasonal trends as a potential roadmap of the markets' path.

With just two weeks of trading days remaining on the calendar, this is the moment that markets start ratcheting higher into year-end – at least according to history.

Below you can see that the first half of December is often the lull for equities before rallying strong the final two weeks, with small- and mid-caps outpacing their large-cap counterparts.

This is welcome news because most stocks outside large-cap tech have struggled thus far in December.

Source: Piper Sandler

A healthy U.S. consumer

With Q3 earnings season nearly complete, reflecting back on company results, management commentary, and how the recent data aligns with intermediate trends help the investor draw macroeconomic lessons from micro-level insights.

One meaningful takeaway has emerged as we look towards 2025: the U.S. consumer remains a source of strength.

Company commentary generally indicated that consumer spending remains resilient. Goldman Sachs produces a quantitative assessment of sentiment around the consumer on earnings calls, and this proprietary measure improved to its highest level in nearly three years.

Pressures on lower-income consumers – including more limited borrowing capacity, underperforming income growth, or rising delinquencies – presented a modest headwind to consumer spending. However, some of the more negative anecdotes from companies exposed to lower-income consumers likely overstate any deterioration in the financial health of lower-income households.

Source: Goldman Sachs Global Investment Research

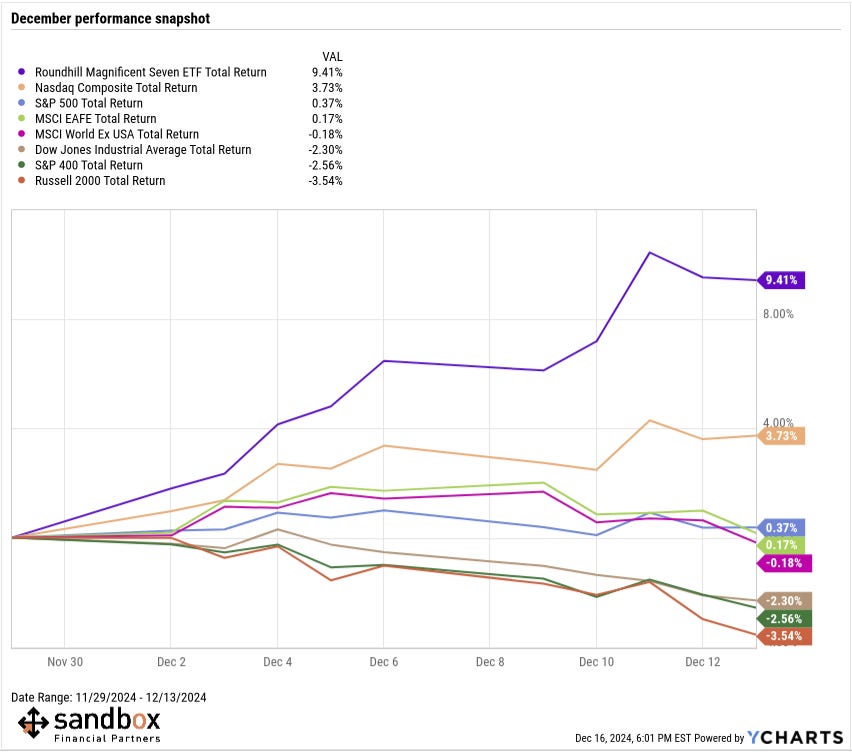

BATMMAAN

The financial media loves acronyms.

For years, it was RMDs, CAGR, GAAP, EPS, Adjusted EBITDA.

More recently, it’s been FIRE, HENRY, and DINKs.

And don’t sleep on the BRICs, GRANOLA, FAANG, and the Mag 7.

Now… BATMMAAN ??!?!

Broadcom, the newest member of the trillion-dollar market cap club, is the latest Belle of the Ball after its better-than-expected earnings report last week Thursday.

On Friday, AVGO gained more than 24% for their largest single-day percentage gain on record – adding $206B in market cap. The rally spilled over into Monday’s session, now up more than 50% in December.

Bernstein’s Semiconductor analyst, Stacy Rasgon, called Broadcom’s stock a “robust AI story [that’s] finding its own ‘Nvidia moment’.”

Source: Chartr

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures at the Sandbox Financial Partners website: