Global stocks surge 📈 after United States, China pause tariff war 🤝

The Sandbox Daily (5.12.2025)

Welcome, Sandbox friends.

Today’s Daily discusses:

global stocks surge after U.S., China pause tariff war

Let’s dig in.

Blake

Markets in review

EQUITIES: Nasdaq 100 +4.02% | Russell 2000 +3.42% | S&P 500 +3.26% | Dow +2.81%

FIXED INCOME: Barclays Agg Bond -0.34% | High Yield +0.99% | 2yr UST 4.002% | 10yr UST 4.475%

COMMODITIES: Brent Crude +1.53% to $64.89/barrel. Gold -3.14% to $3,238.6/oz.

BITCOIN: -2.46% to $102,037

US DOLLAR INDEX: +1.45% to 101.795

CBOE TOTAL PUT/CALL RATIO: 0.77

VIX: -16.03% to 18.39

Quote of the day

“Now and then it's good to pause in our pursuit of happiness and just be happy.”

- Guillaume Apollinaire, French Poet and Playwright

Global stocks surge after United States, China pause tariff war

After talks in Switzerland this weekend, the United States and China agreed to a large reduction in tariffs on each other.

The U.S. is lowering its tariffs on China from 145% to 30%, while China is lowering its tariffs on the US from 125% to 10%. The new tariff rates will be in effect for 90 days while the two sides continue talking.

Along with tariff pauses on other trading partners, and a newly announced trade deal with the United Kingdom, markets are hopeful that a protracted trade war is now off the table.

What does this this mean to investors?

The U.S.-China agreement is a positive sign a broader deal can be reached

The latest tariff agreement between the United States and China is important because it removes a significant source of market uncertainty.

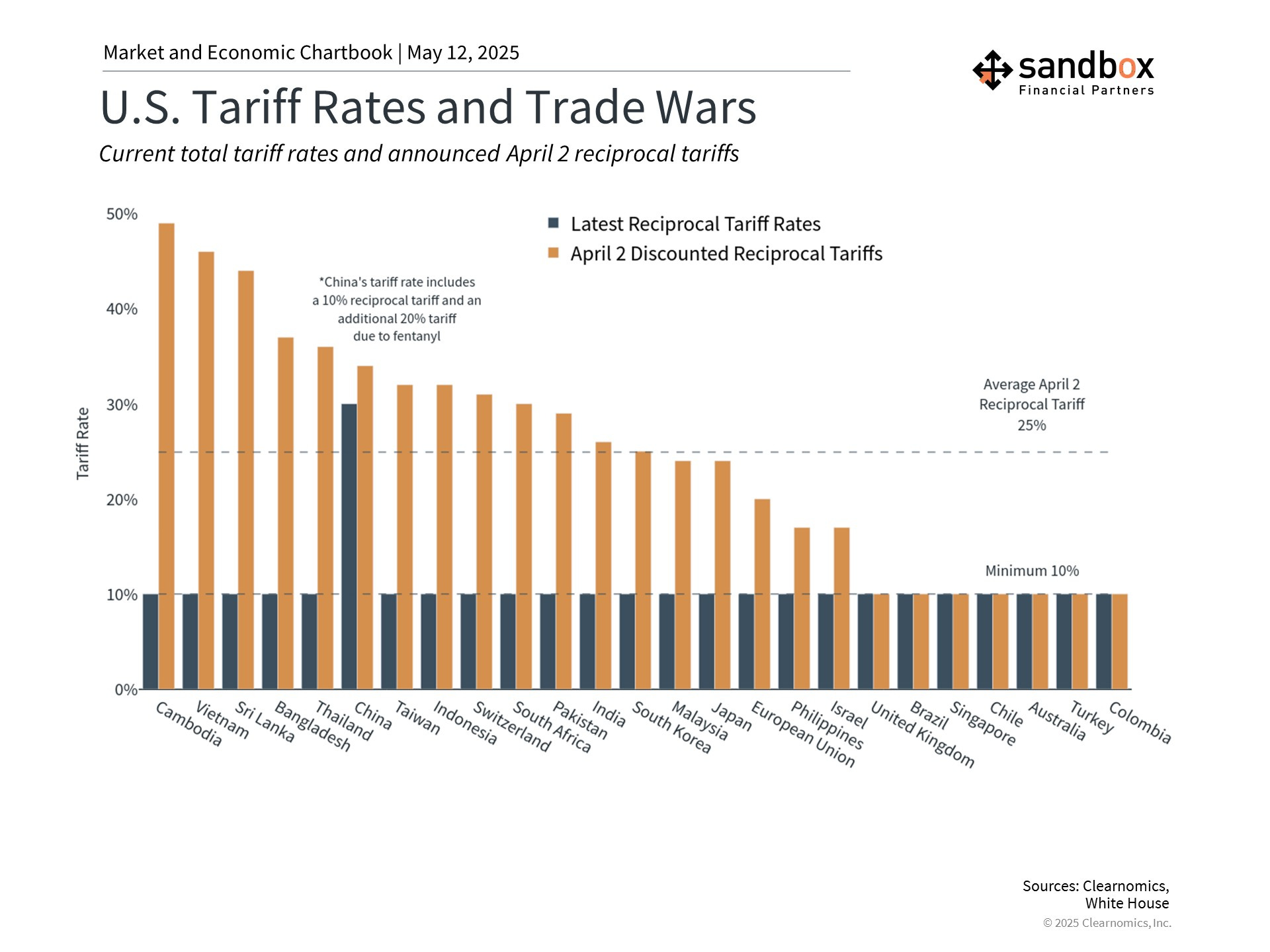

It sets the U.S. reciprocal tariff on Chinese goods to 10%, while maintaining the 20% tariff related to the fentanyl crisis put in place earlier this year.

While the situation is still evolving, this agreement paves the way for a longer-term trade deal between the world’s two largest economies and de-escalates tensions. So, while tariff rates are higher than in the past, the worst-case scenario is now less likely.

With the benefit of hindsight, recent events mirror the trade tensions in 2018 and 2019 during the first Trump administration. In both cases, the administration’s goal has been to achieve new trade deals by using tariffs as a negotiating tool, with the stated aim of closing the U.S. trade deficit with major trading partners. Five years ago, this resulted in the “Phase One” trade agreement with China, the USMCA (United States-Mexico-Canada Agreement), and other deals.

On top of rebooting trade relationships, there are many intertwined secondary objectives in these trade policies, including a focus on manufacturing jobs, protecting intellectual property, controlling immigration, and more.

Today, the key difference is that the administration has gone much further with tariff threats than many investors and economists had anticipated. Still, the recently announced trade deal between the U.S. and the U.K. is evidence that previous patterns may apply here as well.

The economy has been resilient despite trade uncertainty

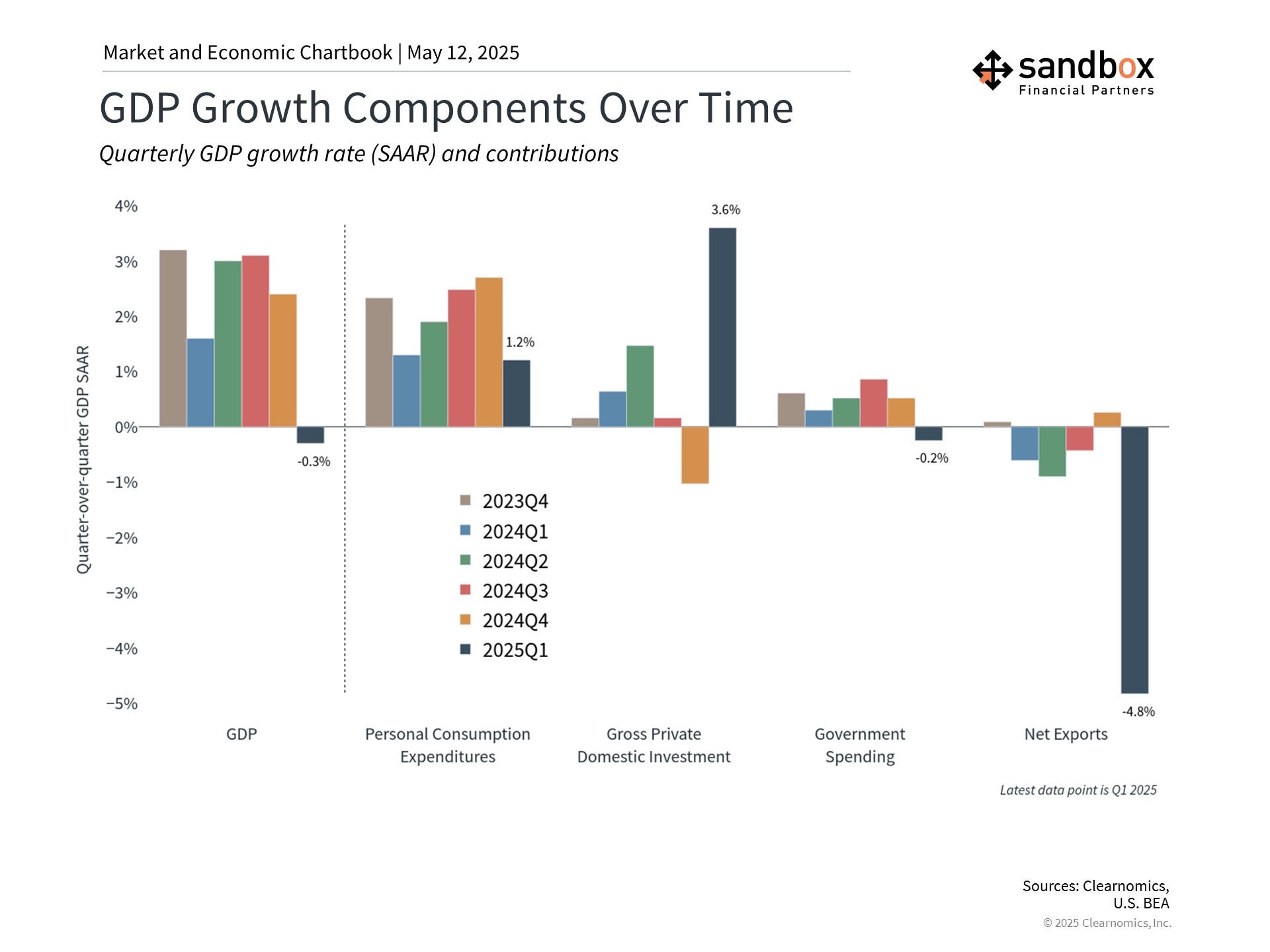

An important reason markets have focused so heavily on tariffs is the impact on inflation and economic growth. This was reflected in the first quarter’s GDP figure which showed a slight economic contraction as businesses stockpiled imported goods ahead of tariff deadlines. Greater clarity will likely help both consumers and businesses.

In this environment, what else could go right?

First, many economic indicators remain solid. The latest jobs report showed the economy added a net 177k jobs in April, while the unemployment rate held steady at 4.2%. The strong job market helps to offset concerns that tariffs and uncertainty will impact consumer spending.

Meanwhile, inflation continues its gradual deceleration toward the Fed's 2% target, with the latest Consumer Price Index (CPI) figure coming in at 2.4% year-over-year. This deceleration has been supported by falling oil prices which recently reached four-year lows. Cheaper oil, driven in part by tariff-related volatility, helps to lower costs for consumers and can be a boost to the economy, all things equal.

The recent U.S.-China agreement also reduces the pressure for immediate Fed policy changes. The Fed, which recently kept rates steady between 4.25% and 4.50%, appears to be taking a “wait-and-see” approach, rather than reacting to near-term trade, market, and economic news.

Market recoveries often occur when they’re least expected

While there are still many risks to the market, the last several weeks show how quickly the narrative can change.

By their very nature, markets anticipate worst-case scenarios. During times of negative headlines and market pullbacks, it’s difficult to imagine that the market will ever recover.

So, while understanding risks is always prudent, it should not come at the expense of long-term portfolio positioning.

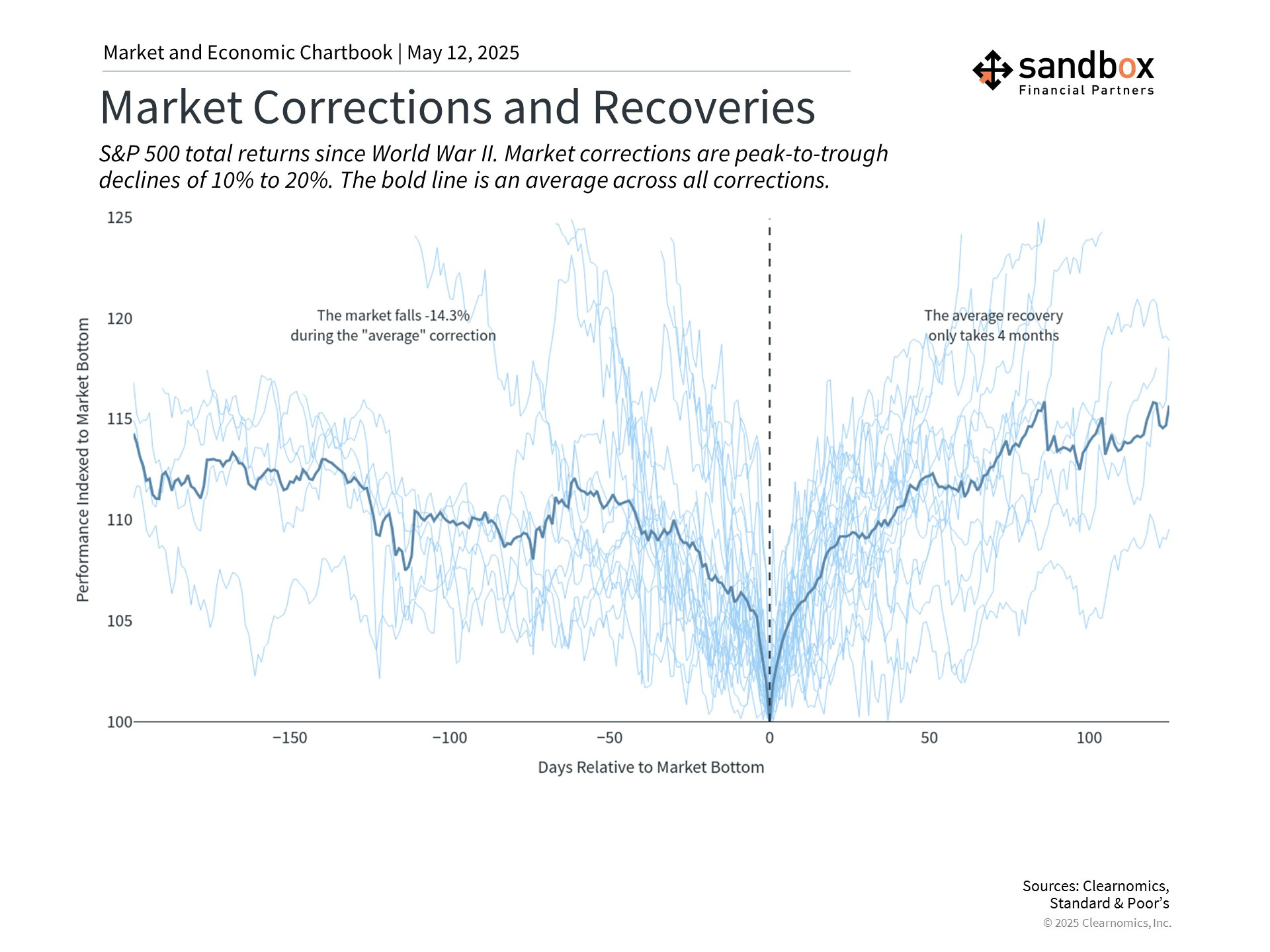

The chart below shows how market corrections have behaved since World War II. While the average correction experiences a decline of 14%, it often recovers in as little as four months.

Perhaps of greater significance, markets can often rebound when it’s least expected, as we’ve experienced following recent progress on trade negotiations.

Those who overreact to early signs of volatility may find they are not appropriately positioned.

Bottom line?

The latest U.S.-China trade announcement has lowered market uncertainty and recession concerns.

For long-term investors, this reinforces the value of maintaining perspective during periods of market turbulence rather than reacting to short-term volatility.

Sources: White House, Bloomberg, Clearnomics

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures at the Sandbox Financial Partners website: