Growth vs. Value, plus job losses, financial conditions, gold, and sentiment

The Sandbox Daily (3.20.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

Growth vs. Value

Estimates of labor market sacrifices to achieve inflation target

Disinflationary trends

Gold prints fresh 52-week high

Sentiment washes out (again)

Let’s dig in.

Markets in review

EQUITIES: Dow +1.20% | Russell 2000 +1.11% | S&P 500 +0.89% | Nasdaq 100 +0.34%

FIXED INCOME: Barclays Agg Bond -0.40% | High Yield -0.27% | 2yr UST 3.966% | 10yr UST 3.483%

COMMODITIES: Brent Crude +1.79% to $73.77/barrel. Gold +0.47% to $1,999.6/oz.

BITCOIN: -0.84% to $27,808

US DOLLAR INDEX: -0.54% to 103.306

CBOE EQUITY PUT/CALL RATIO: 0.65

VIX: -5.33% to 24.15

Quote of the day

“That men do not learn very much from the lessons of history is the most important of all the lessons that history has to teach.”

-Aldous Huxley

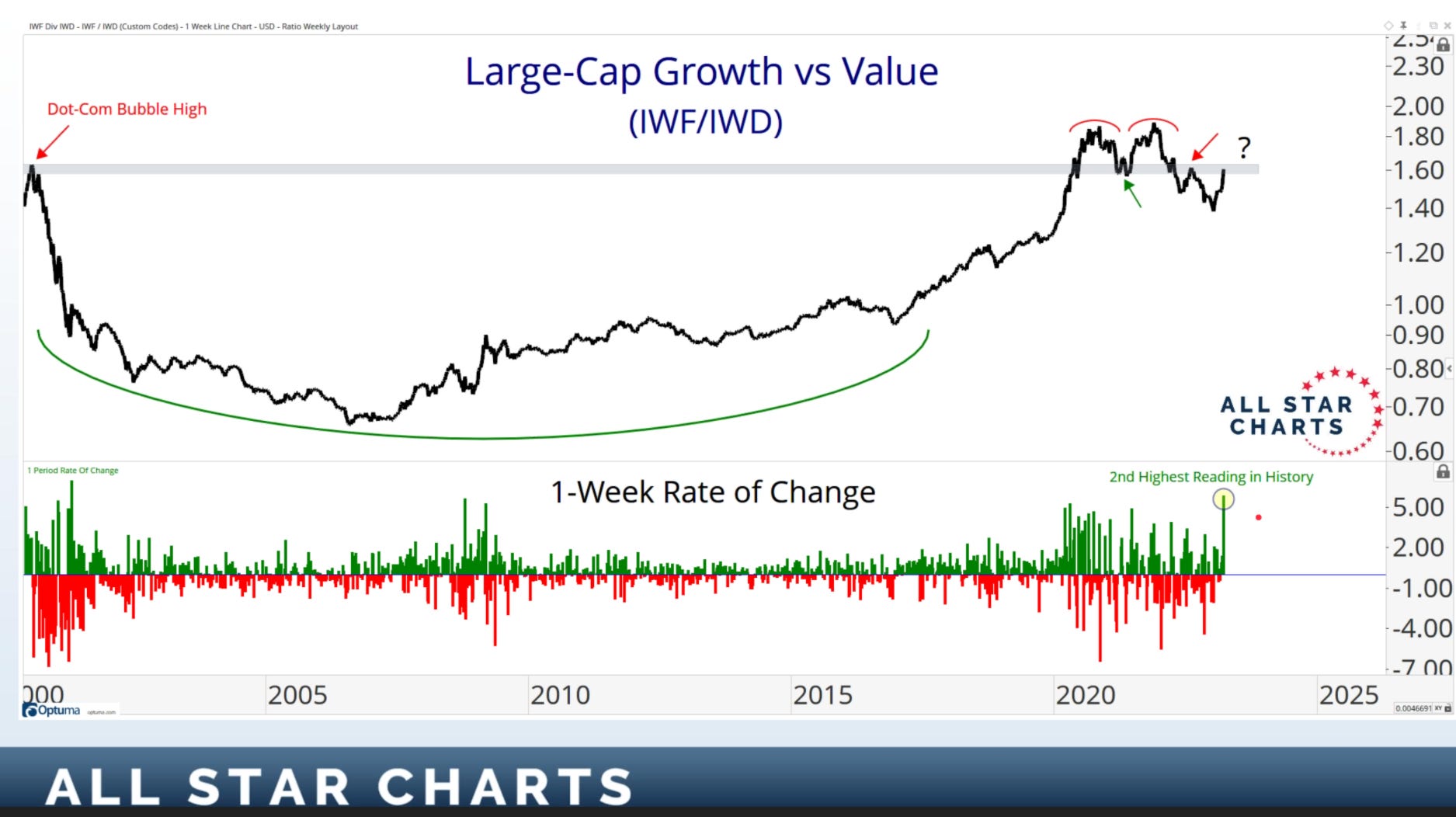

Growth vs. Value

Fallout from bank failures and mergers continue to roil markets, causing major price swings across most asset classes. Stock and bond volatility measures (VIX and MOVE, respectively) confirm as much.

Of particular note, the move in Large-Cap Growth against Large-Cap Value just registered its 2nd-largest weekly gain in history. This should be no surprise given the recent disastrous price action across the Financials sector and its significant presence in the Value bucket. In fact, one must go back to the dotcom bubble crash in 2001 to find a week where growth outperformed value more than it did last week.

Below is a ratio chart of Large-Cap Growth to Large-Cap Value; by taking the price of one security and dividing it by the price of another, we can easily identify relative strength and evaluate the merits of that investment by observing the trend.

We want to pay close attention to extreme rate of change (ROC) readings such as this, as they are evidence of momentum thrusts. Momentum thrusts tend to occur at turning points and can signal either the exhaustion of an old trend or the initiation of a new one. Considering the ratio fell steadily throughout 2022, it is unlikely that this signals exhaustion.

Zooming into more recent price action, Growth vs. Value has shown an impressive bounce off the January lows but remains below a key level (red horizontal line) that was a swing low in May 2022 (red upward pointing arrow) and resistance in November 2022 (red downward pointing arrow).

Source: All Star Charts, Thrasher Analytics

How many jobs must be sacrificed to tame inflation?

RSM research indicates that the Federal Reserve, facing persistent inflation, will for now have to accept a de-facto inflation target of 3% to avoid the destruction of millions of jobs that would accompany achieving a 2% target.

To reduce inflation to acceptable levels – using the personal consumption expenditures price index, the Fed’s key inflation metric – would mean the loss of 2.5 million to 6.1 million jobs. The unemployment rate, as a result, would have to rise to between 5.1% and 7.3%.

The Federal Reserve faces a difficult proposition: how to achieve price stability while maintaining financial stability during a modest banking crisis in the face of a labor market that remains incredibly resilient.

Source: RSM

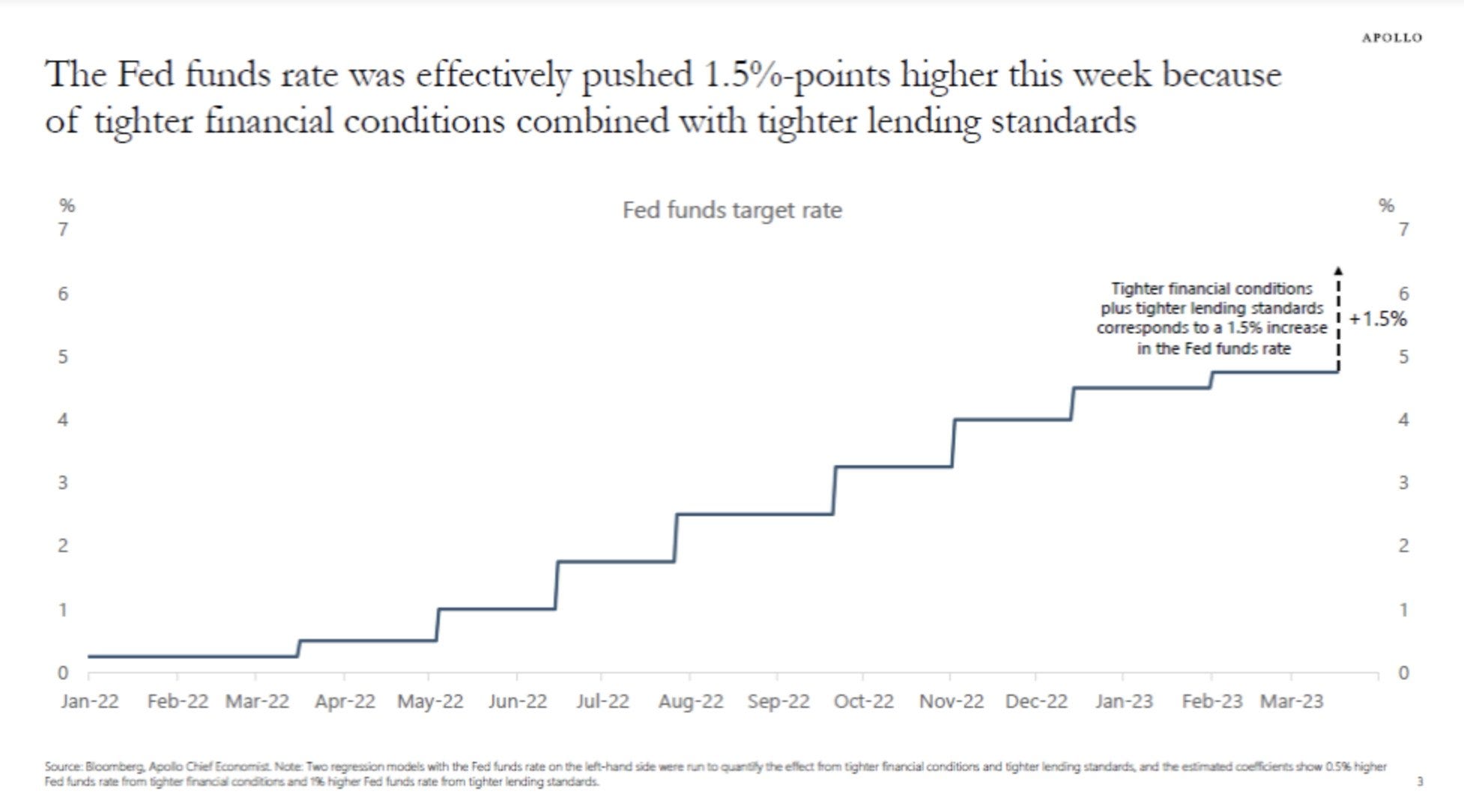

Disinflationary trends

Monetary conditions have tightened to a degree where the risks of a sharper slowdown in the economy have increased.

Torsten Slok, chief economist at Apollo Global Management, wrote in a note over the weekend that the recent tumult in the banking sector is already tightening financial conditions. The events this past week are equivalent to a significant rate hike – a 1.5% increase in the Fed Funds Rate.

Source: Apollo Global Management

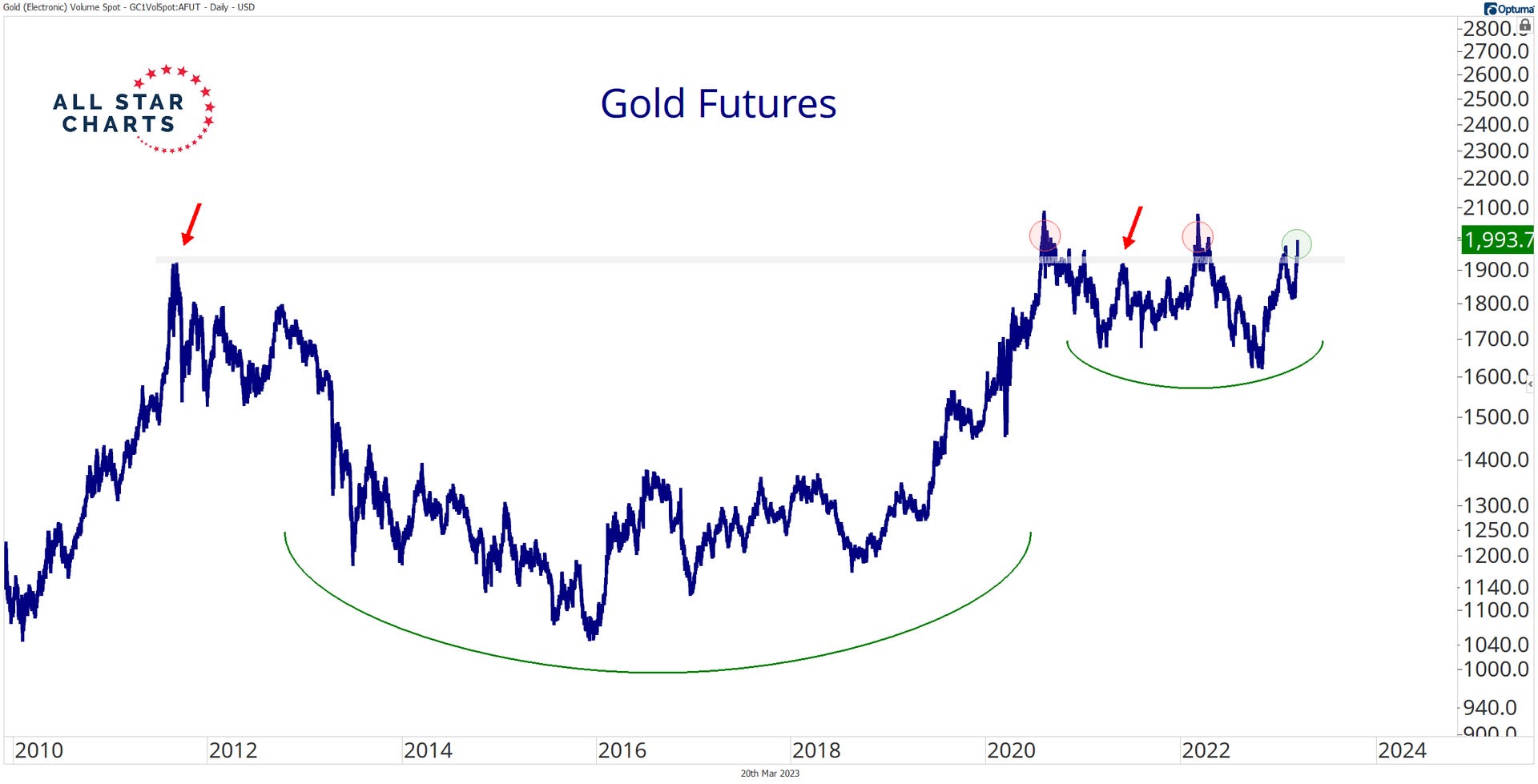

Gold prints fresh 52-week high

Prices of precious metals are rising again, with gold leading the way.

Gold closed out last week with another strong performance, absorbing overhead supply at a critical level—the former 2011 highs. Those former highs mark the peak of the last secular bull market for gold, and last week’s breakout signifies a significant uptick in demand for the traditional safe haven asset.

Gold is breaking out to new all-time highs in currencies all around the world. Meanwhile, gold priced in U.S. dollars is approaching fresh all-time highs of its own; on an absolute basis, gold is still stuck in a multi-year range between $1,680/oz and $2,060/oz. The next upside objective will be the 2020/2022 all-time highs, which are around $2,070/oz – and to be clear, gold is approaching the top end rapidly.

It’s hard to ignore the impressive upside follow-through across the precious metals space. It will be worth watching other precious metals, namely silver, for confirmation of the move in gold.

Source: All Star Charts, Grindstone Intelligence

Less than one in five investors are bullish on the market

Recent bank turmoil and the pullback in the S&P 500 index has taken a toll on retail investor sentiment, and for the first time since September, less than 20% of investors are bullish on the market (green bars below).

The American Association of Individual Investors (AAII) reported bullish sentiment fell 5.6% to just 19.2%, the lowest percentage of bulls since September 2022. Bearish sentiment increased for the 4th time in the last weeks, rising to 48.4% from 41.7%, the highest reading this year.

The spread between Bulls and Bears is at -29%, the most negative since last October. Active managers responded, quickly reducing their equity exposure to 41.9% from the previous week of 60.1%.

Source: American Association of Individual Investors, Charlie Bilello, Dwyer Strategy

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.