Happy New Year and the technical backdrop supporting equities in 2024

The Sandbox Daily (1.3.2024)

Welcome, Sandbox friends.

Hello and Happy New Year! Wishing everyone a wonderful and productive 2024!

Today’s Daily discusses the technical backdrop that remains supportive of additional equity gains over the coming year:

Breadth expands beyond the Magnificent 7

historic momentum

breadth thrust regime

Zweig Breadth Thrust

strength begets strength

looking down the cap stack

running with the bulls

Let’s dig in.

Markets in review

EQUITIES: Dow -0.76% | S&P 500 -0.80% | Nasdaq 100 -1.06% | Russell 2000 -2.66%

FIXED INCOME: Barclays Agg Bond +0.05% | High Yield -0.27% | 2yr UST 4.335% | 10yr UST 3.922%

COMMODITIES: Brent Crude +3.47% to $78.52/barrel. Gold -1.17% to $2,049.4/oz.

BITCOIN: -4.87% to $42,896

US DOLLAR INDEX: +0.26% to 102.469

CBOE EQUITY PUT/CALL RATIO: 0.65

VIX: +6.36% to 14.04

Quote of the day

“We cannot solve our problems with the same thinking we used when we created them.”

- Albert Einstein

Respecting the technical backdrop as we embark upon 2024

Over the holidays, I stepped away from the endless barrage of e-mails, reporting, analysis, and charts that usually consume my time and efforts – instead, shifting my attention to my wife and kids and the natural beauty of the Florida Keys.

This annual ritual allows me to be fully present with my family.

Turning off the spigot also provides an opportunity to collect my thoughts at a high level as to what the new year may bring us.

And over the last two weeks, time and time again, I kept revisiting the incredible technical strength that carried the markets to/near all-time highs in November and December 2023.

It was impossible for me to ignore. No more Magnificent 7; this was the everything rally.

The reason for this market strength can largely be distilled down to two basic developments:

The disinflationary impulses of 2023 should not be ignored, and the probabilities favor more disinflation to come in 2024, mainly via housing and auto. This leads to a more accommodative Fed, which brings me to my next point.

At the December 13th FOMC meeting, the Federal Reserve tweaked its policy statement to suggest that additional rate hikes are no longer likely, while simultaneously hinting that significant rate cuts are on the way this year. This “pivot” points toward a Fed downshifting from the most aggressive monetary policy in decades, maybe ever. We’re transitioning in the cycle from monetary policy grounded in the inflation war to now just managing the business cycle.

Given the stock market is a discounting mechanism, equities rallied strongly as it priced in the two developments listed above.

Will the market continue to move in a straight line up from here? Of course not! But, when we take a step back and observe the behavior of market participants and take a weight-of-the-evidence-approach, we should always be asking ourselves each week and each month: are we net buyers of stocks or net sellers?

I discussed this, and much more, with my friends J.C. Parets and Steve Strazza from All Star Charts on The Morning Show last week while in the Keys – yup, couldn’t step away entirely while on vacation. Hit play at the 40:31 mark.

So, what exactly do I mean by respecting the technical backdrop?

Let’s walk through a few charts together, however there are dozens of others that would qualify as well.

Breadth expands beyond the Magnificent 7

The recent march to new highs across various equity indices and sectors pushed the percentage of stocks in the S&P 500 Index (SPX) trading above their respective 50-day moving averages to an extreme level back in late December.

The percentage of stocks that traded above their 50-dma was at 90.84%, the highest reading in ~13 months.

Prior initial readings of 90% or more have historically been bullish for the market over the intermediate term; however, the short-term outlook was much more inconsistent.

Since March of 1990, the forward 12-month returns for the SPX following the initial move to 90% were positive 18 out of 19 times (95% win ratio), with a median gain of +15.57% one year later.

Source: Dwyer Strategy

Historic momentum

Overbought conditions are one characteristic of bull markets, especially around the formation of new uptrends.

In mid-December, the proportion of stocks showing up as “overbought” (daily RSI > 70) reached its highest level on record, with just two prior instances (June 2003 and June 2020) triggering the same signal.

This does make the market susceptible to a short-term pullback/consolidation move, but it is important to emphasize an overbought signal is often bullish as it signifies strong momentum, most notably when the indicator flashes at the beginning of a new trend versus the end of a maturing one.

Source: Steve Strazza

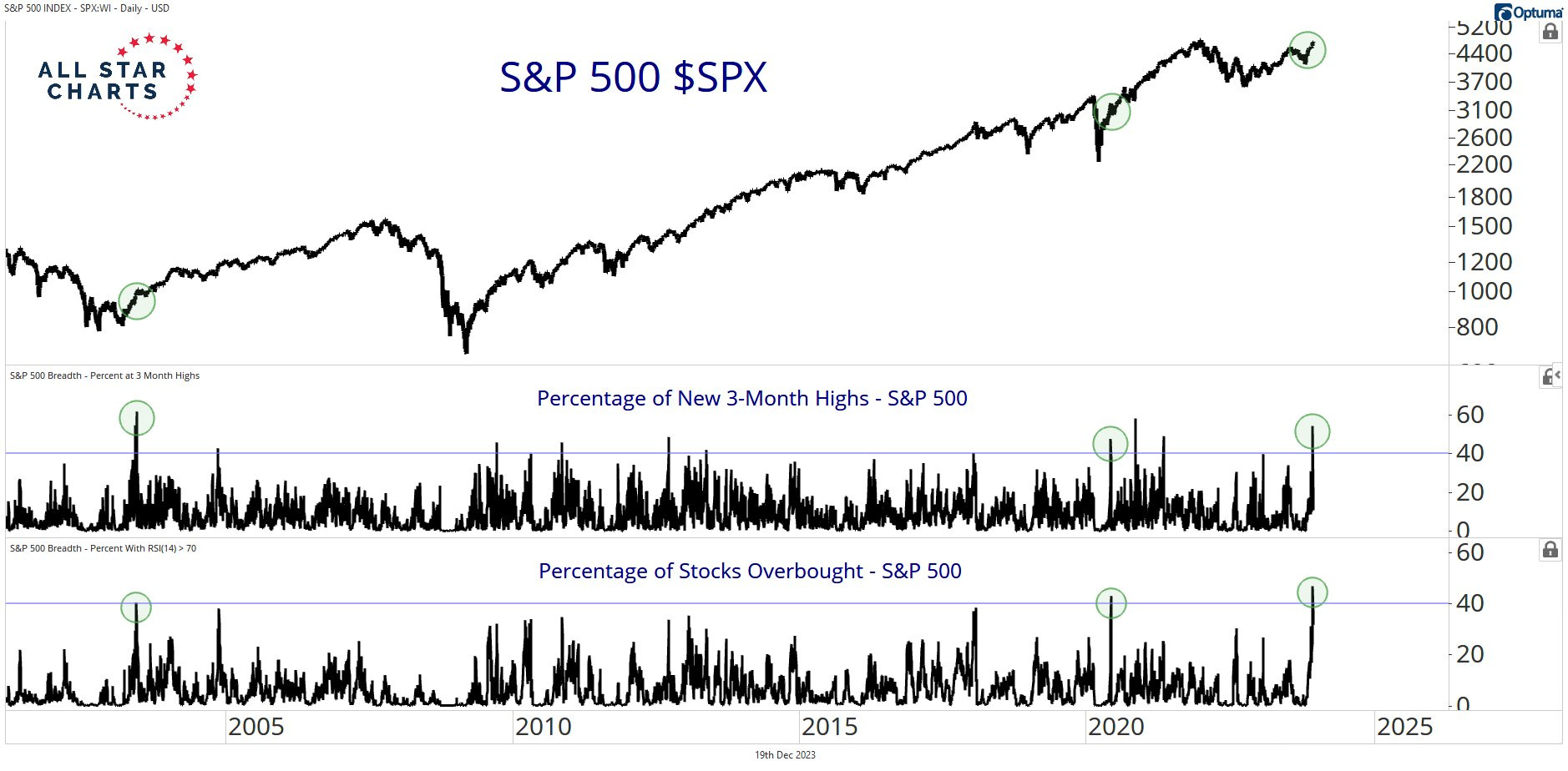

Breadth thrust regime

In fact, when you overlay breadth and momentum together, these thrusts flashed in tandem together for just the 3rd time in the last 20 years.

Below, we are looking at the percentage of stocks making new 3-month highs eclipsing the 40% barrier, while simultaneously measuring the percentage of stocks flashing overbought conditions.

Suffice it to say, the sheer buying pressure we witnessed in November and December was historic.

Source: Alfonso Depablos

Zweig Breadth Thrust

A breadth thrust is a technical indicator which determines market momentum, often signaling the start and/or persistence of uptrends.

A rare and very bullish breadth indicator – the Zweig Breadth Thrust (ZBT) – triggered on Friday, November 3rd.

A ZBT occurs when the 10-day exponential moving average of the NYSE Percentage of Up Issues rises from below 40% (indicating an oversold market) to above 61.5% within 10 days.

In plain English, the Advance-Decline numbers suddenly go from not so good to REALLY good in a short amount of time.

ZBT’s are a very rare occurrence and possess a good track record of coming in the vicinity of major lows – higher 12 months later after every signal since World War II.

And one thing we know from experience is that breadth thrusts are NOT evidence of exhaustion.

In fact, it’s quite the opposite. We regularly see clusters of breadth thrusts near the beginning of new uptrends, and early in Bull Markets.

Source: Carson Group, McClellan Financial Publications, SentimenTrader

Strength begets strength

The S&P 500 index finished up +24.23% in 2023.

What happens next after a +20% calendar-year rally?

More often than not, the S&P 500 follows through with more strength – higher 22 of 34 instances (65% win ratio) resulting in a median gain of +11.4% the subsequent year.

Source: Mike Zaccardi

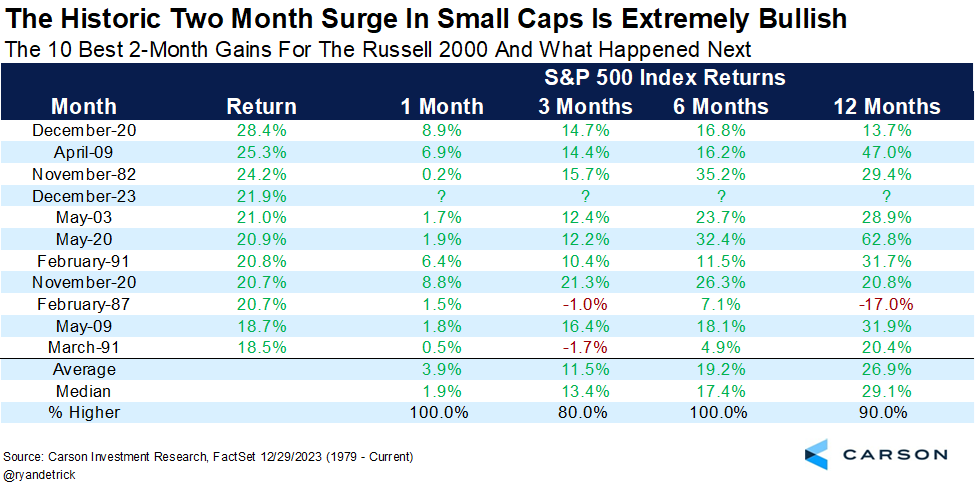

Strength down the cap stack

The Russell 2000 Index, the notable equity laggard for much of 2023, saw a surge of buyers flood into the space in November and December.

The small-cap index gained +21.9% during the final two months of 2023, its 4th best 2-month gain on record.

Let me repeat that. The R2000 gained +21.9% in two months - wow !!

Looking to history as a guide, what comes next?

Reviewing the previous ten best 2-month periodic gains showed the Russell 2000 Index higher a year later 9 times of 10 for a median gain of +29.1%.

Source: Ryan Detrick

Running with the bulls

Also, if we are to incorporate sentiment into our exercise, then what were the market gods signaling to us in December when a bull was found running loose on the tracks at Newark Penn Station?

Source: NJ.com

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.