Hot 3rd quarter GDP print, plus small-caps and saving for $1,000,000

The Sandbox Daily (10.26.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

strong consumer spending drives 3rd quarter GDP growth

tough going for the little guy

how to save for $1,000,000

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 +0.34% | Dow -0.76% | S&P 500 -1.18% | Nasdaq 100 -1.89%

FIXED INCOME: Barclays Agg Bond +0.67% | High Yield +0.35% | 2yr UST 5.042% | 10yr UST 4.847%

COMMODITIES: Brent Crude -1.94% to $88.38/barrel. Gold +0.16% to $1,987.2/oz.

BITCOIN: -1.73% to $34,147

US DOLLAR INDEX: +0.08% to 106.610

CBOE EQUITY PUT/CALL RATIO: 0.90

VIX: +2.43% to 20.68

Quote of the day

“Don't overlook the basics. Don't ignore the foundation. How long can a tree remain standing without the roots?”

- James Clear, Atomic Habits

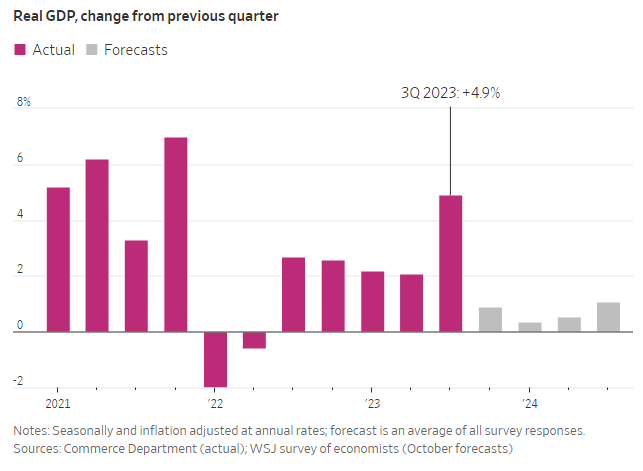

Strong consumer spending drives 3rd quarter GDP growth

Recession? I don’t know her.

Despite the ongoing headwinds that caused many economists and market watchers to forecast recession in 2023 – higher interest rates, protracted high inflation, geopolitical events, an earnings recession, labor strikes, and more recently, the vacancy of the U.S. speakership – the rocket ship that is the U.S. economy continues forge ahead.

The U.S. economy’s report card showed that GDP in the 3rd quarter expanded at a 4.9% annualized rate (inflation-adjusted). Of course, there are warning signs under the headline number – business investment stalled while American saved less – but this is an economy that is growing, not contracting.

Consumer spending – the primary growth engine of our economy and outlined in the chart below (personal consumption = consumer spending) – has continued to defy expectations and chug along. It grew +4.0% in Q3, way up from +0.8% in Q2.

Economists expected that high prices and persistent inflation would stop people from spending. But in September, U.S. retail sales crushed expectations while the labor marked added 366k jobs, once again confounding the experts.

Whether consumers can keep the party going in the last 3 months of the year, which are crucial for retailers given the holiday shopping period, remains to be seen.

Bottom line: The resilient economy likely reflects longer-than-expected policy lags, likely due to the substantial fiscal stimulus to households and businesses in response to the pandemic. But, while this has blunted the speed of the policy transmission mechanism, it has not eliminated it. With excess savings coming down, tighter bank lending standards, and higher interest rates pushing up interest expenses to both households and businesses, one should expect aggregate demand and real GDP growth to slow in the coming quarters. See the gray bars in the 1st chart above regarding forward market expectations.

Source: Wall Street Journal, Bloomberg, Dwyer Strategy, Ned Davis Research

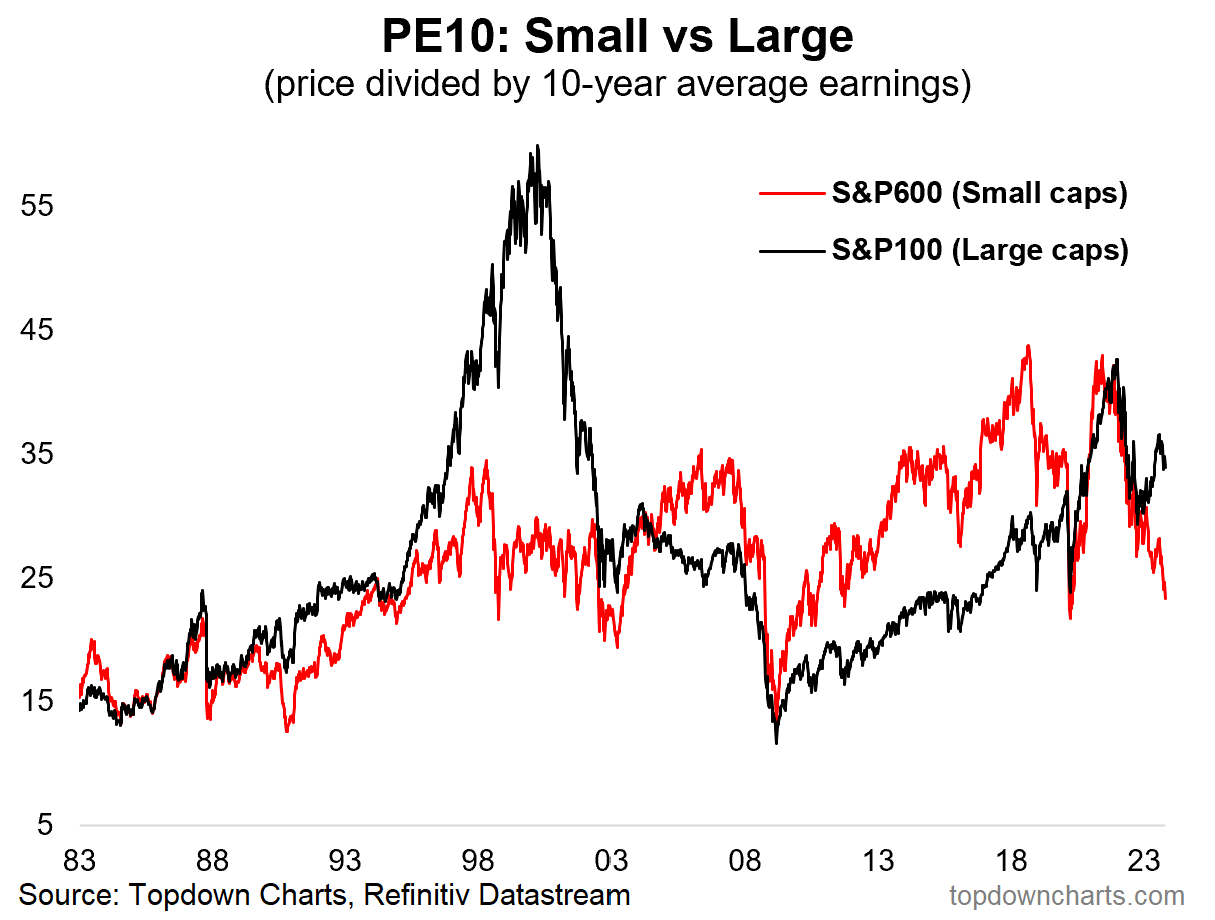

Tough going for the little guy

The Russell 2000 Index (U.S. small-cap stocks) is back to ground zero – the 2018 highs, the pre-COVID highs, the June 2022 lows, the October 2022 retest, and the regional-banking crisis lows.

The $163-$172 cloud for the iShares Russell 2000 ETF (IWM) seems to possess the gravitational pull of a black hole. Well-traveled ground for this bunch – see below.

After nearly two years of sideways price action, small-cap stocks are once again testing this critical polarity zone that has acted as a resistance-turn-support level for years.

As long as the Russell 2000 holds above those prior-cycle highs, stocks are unlikely to experience further downside. Instead, the bottoming process that’s been taking place since last year would continue. However, if the bulls lose this level, we could anticipate increased volatility and another leg lower for risk assets.

From a valuation perspective, small-caps relative to large-caps are nearly as cheap now as the depths of the 2020 COVID crash.

The downside risks are notable (lack of pricing power, higher cost of capital, more cyclically-oriented – to name a few), so one should expect this relative valuation discount to persist for some time.

Something to keep in mind about small-caps, though: the entire universe of the Russell 2000 by market capitalization is smaller than Apple (AAPL).

With the small-cap Russell index down -17% since late July, the combined market cap of all Russell 2,000 stocks has fallen to just $2.4 trillion today – that’s ~$200 billion less than Apple's (AAPL) market cap of just over $2.6 trillion.

Source: Topdown Charts, Bespoke Investment Group

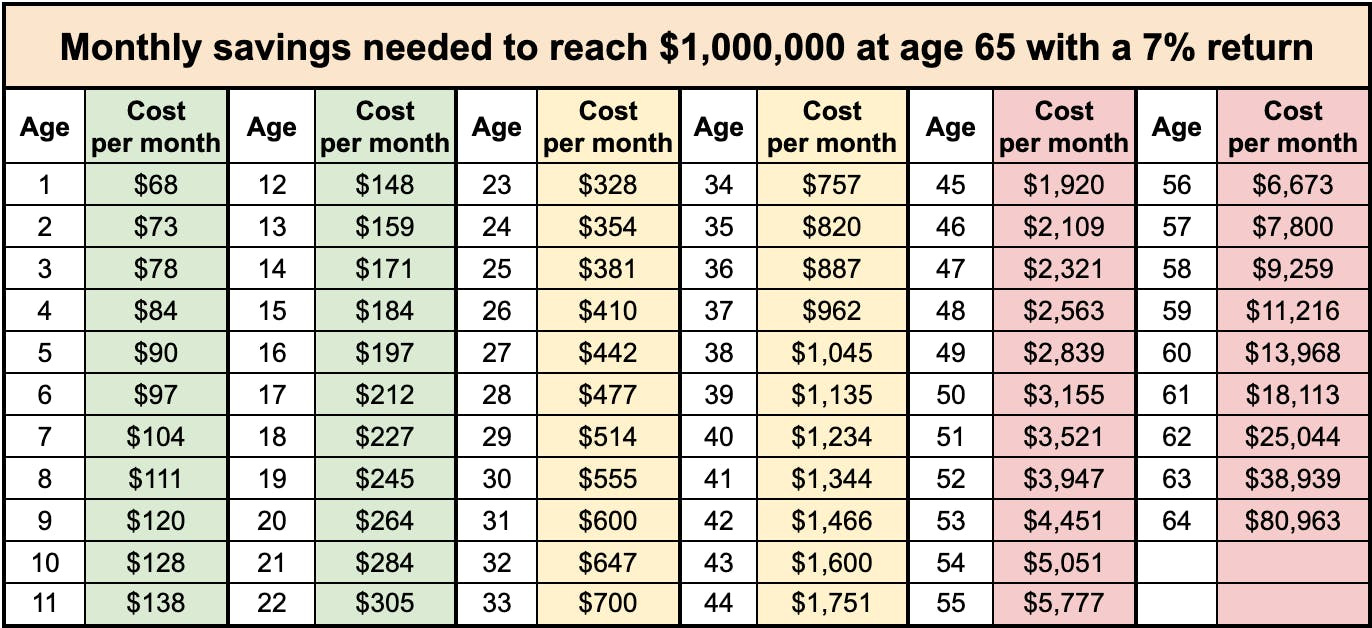

Saving trumps all else

This table below shows you the monthly savings rate by age required to reach $1,000,000 assuming a 7% portfolio return.

The lesson?

Save early AND often.

Time and compounding will do the rest.

Unfortunately, life, or investing for that matter, doesn’t work out in a neat, straight line with a red bow. However, understanding the basic concept of compounding is one of the most powerful personal finance insights one can ever learn.

An investor can only compound their money AFTER it has been saved, so always pay attention to your savings rate!

Source: Brian Feroldi

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.