How stocks perform past peak inflation, plus producer prices, China, rate hikes breaking things, and initial jobless claims

The Sandbox Daily (5.11.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

stock performance past inflation peak

wholesale prices (PPI) for April point to easing inflation pressures

Chinese consumer prices slump to a two-year low

rapid rate increase always break something

initial jobless claims jump

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 +0.31% | S&P 500 -0.17% | Dow -0.66% | Russell 2000 -0.84%

FIXED INCOME: Barclays Agg Bond +0.30% | High Yield -0.16% | 2yr UST 3.899% | 10yr UST 3.382%

COMMODITIES: Brent Crude -1.14% to $75.54/barrel. Gold -0.87% to $2,019.3/oz.

BITCOIN: -3.09% to $26,841

US DOLLAR INDEX: +0.59% to 102.077

CBOE EQUITY PUT/CALL RATIO: 0.68

VIX: -0.06% to 16.93

Quote of the day

“Investing is not entertainment – it's a responsibility – and investing is not supposed to be fun or 'interesting.' It's a continuous process, like refining petroleum or manufacturing cookies, chemicals or integrated circuits. If anything in the process is 'interesting,' it's almost surely wrong.”

- Dr. Charles Ellis

Stock performance past inflation peak

The Consumer Price Index (CPI) peaked at +9.1% in June 2022 and the most recent reading shows YoY inflation growth at +4.9%. We are nearly a year removed from peak inflation having seen the headline number come down 10 consecutive months.

If peak inflation is truly behind us, what does that mean for stock prices?

While every cycle is different, looking at past inflation peaks can provide some insights on the outlook for stocks. Using history as a guide, returns fared much better in the year following peak inflation than in the year prior. Both the median and average returns are negative in the year leading up to the peak, while both the median and average returns are positive the year after peak CPI (but in line with long-run overall averages).

Source: LPL Research

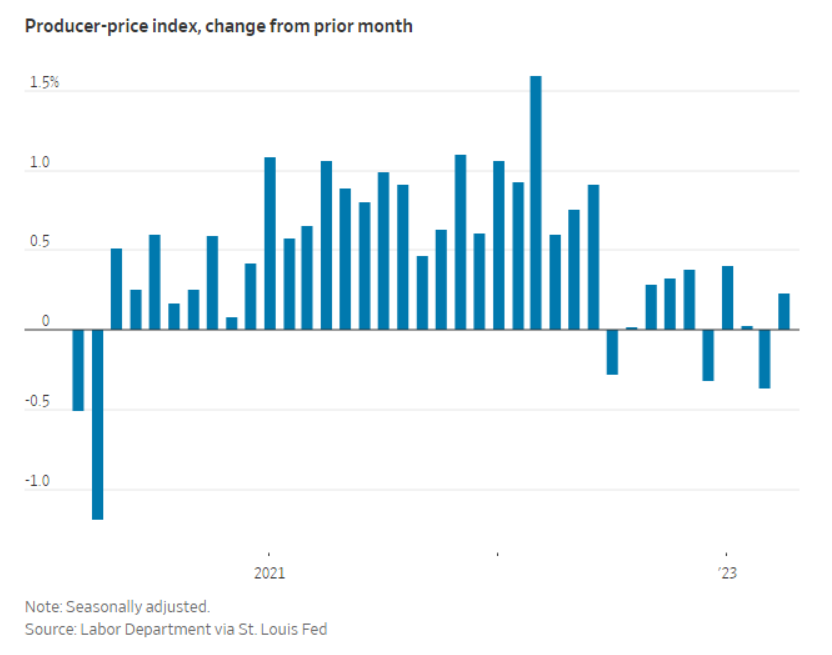

Wholesale prices (PPI) for April point to easing inflation pressures

The Labor Department released its latest Producer Price Index (PPI) for April, tracking inflation from the standpoint of manufacturers and wholesalers. April's PPI (producer prices) confirms what the CPI (consumer prices) showed Wednesday morning, with wholesale prices rising just +0.2% in April.

Headline PPI rose just +2.3%, down from +2.7% in March and the lowest reading since January 2021. The cycle peak was +11.7% back in March 2022, with the index down 12 of the last 13 months.

The PPI differs from the CPI in that it measures prices that producers pay for the goods and services they need.

“This morning’s PPI release indicates that prices are inching lower, a significant indicator for a market concerned about an elevated trend in prices paid,” said Quincy Krosby, chief global strategist at LPL Financial.

Source: Bureau of Labor Statistics, Ned Davis Research, Wall Street Journal

Chinese consumer prices slump to a two-year low

China’s consumer prices barely grew in April while a separate report showed that borrowing slumped –providing further evidence of the economy’s tepid recovery and fueling market expectations of more central bank stimulus.

Consumer inflation weakened to a two-year low of +0.1% in April – it’s the lowest rate since February 2021.

Source: Reuters

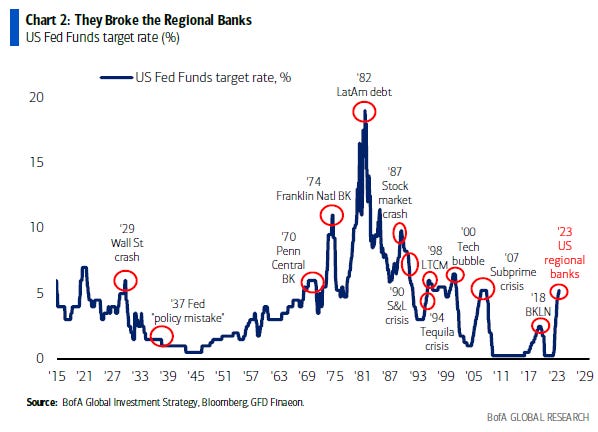

Rapid rate increase always break something

Taking rates from 0% to 5% in 15 months.

Fed hiking cycles always break something.

Source: Bank of America Global Research

Initial jobless claims jump

Initial claims for unemployment insurance jumped last week to 264,000, its highest level since October 2021. It was the fourth increase in the past five weeks and the most since early March. The continued increase in filings was reflected in a 6,000 bump-up in the 4-week average of claims to 245,250, its highest level since November 2021.

Although the level of initial claims is still relatively subdued – running well below the pre-pandemic historical average of 350,000 per week – the upward trend since the cyclical low in September 2022 shows that labor demand has softened and labor market conditions have started to ease.

Additionally, continuing claims increased to 1.813 million, hovering near their highest level since December 2021.

The upward trend in both indicators since their cyclical lows last year is another sign of less tightness in labor markets.

Source: Ned Davis Research, Bloomberg

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.