How the Fed under Kevin Warsh may impact markets

The Sandbox Daily (5.27.2026)

Welcome, Sandbox friends.

Today’s Daily discusses:

the new Fed under Kevin Warsh

Let’s dig in.

Blake

Markets in review

EQUITIES: Dow +0.36% | S&P 500 +0.02% | Russell 2000 -0.02% | Nasdaq 100 -0.09%

FIXED INCOME: Barclays Agg Bond +0.08% | High Yield -0.06% | 2yr UST 4.037% | 10yr UST 5.011%

COMMODITIES: Brent Crude -1.98% to $84.88/barrel. Gold -1.06% to $4,486.8/oz.

BITCOIN: -1.26% to $75,119

US DOLLAR INDEX: +0.04% to 99.21

CBOE TOTAL PUT/CALL RATIO: 0.82

VIX: -4.23% to 16.29

Quote of the day

“Embrace uncertainty. Some of the most beautiful chapters in our lives won’t have a title until much later.”

- Bob Goff

How the Fed under Kevin Warsh may impact markets

For the first time in eight years, the Federal Reserve has a new Chair. Kevin Warsh is bringing a distinct philosophy, a hawkish record, and an ambitious agenda for change.

Why does all this matter?

The Federal Reserve plays a central role in financial markets and the economy, and its importance has only grown in recent decades. From the 2008 Global Financial Crisis to the inflationary period of the past several years, investors follow every Fed decision carefully.

So, when leadership changes occur at the Fed, they naturally capture the attention of investors and the broader public. At the same time, it’s important to understand what the Fed does and does not control when it comes to long-term investing.

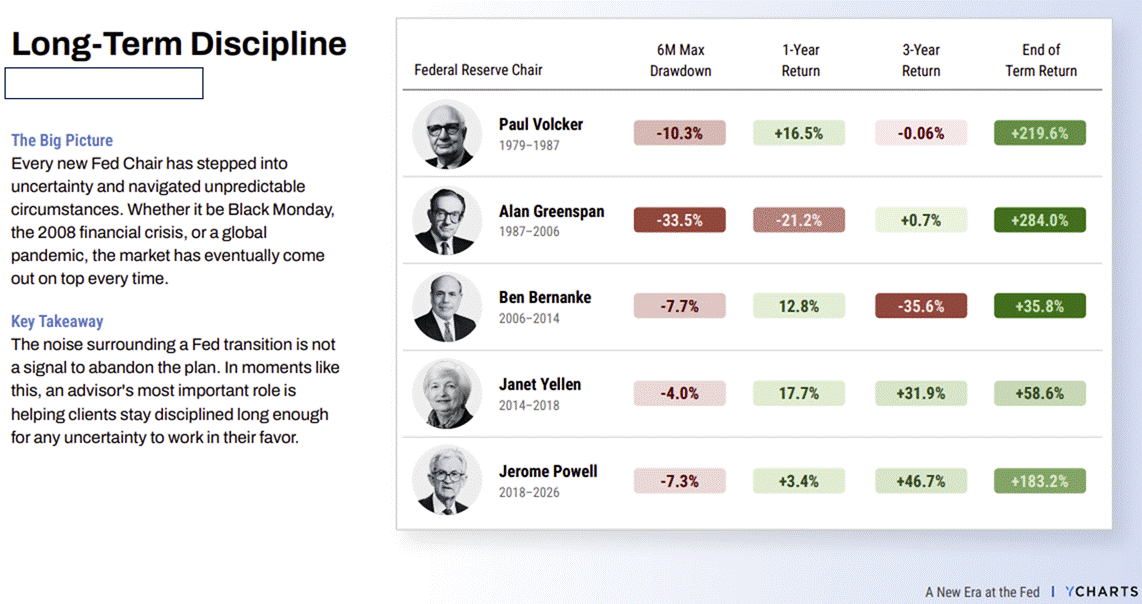

The economy has grown under many Fed leaders

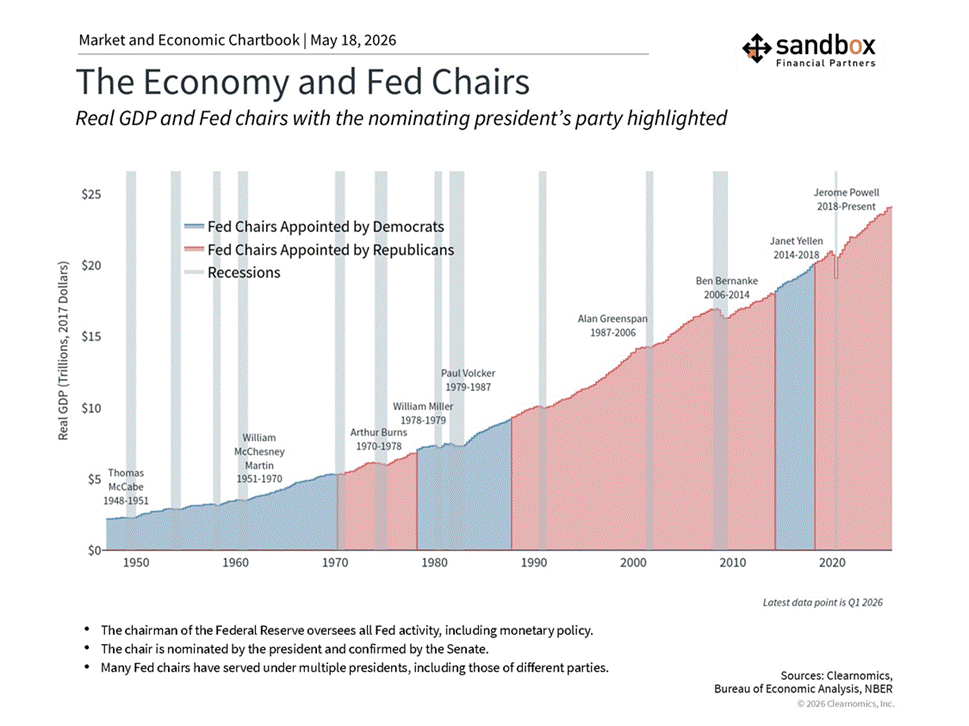

Fed leadership transitions happen infrequently so it’s helpful to zoom out for some perspective.

The Chair of the Federal Reserve is nominated to a four-year term, while members of the Board of Governors serve rotating 14-year terms. The primary reason for this structure is to separate monetary, regulatory, and supervisory decisions from politics. This is often referred to as “Fed independence,” a concept that has been tested and debated across history.

It’s important to remember the U.S. economy has grown across the tenures of different Fed chairs, regardless of which president nominated them.

Each navigated unique economic challenges, from stagflation in the 1970s to the Global Financial Crisis, the pandemic, and the recent inflation surge.

In between, there have been numerous market and economic cycles which forced the Fed to react to new circumstances, in some cases by using their policy tools in new ways.

The Federal Reserve Reform Act of 1977 established a “dual mandate” to promote maximum employment and stable prices (i.e. inflation), which ideally should result in predictable long-term growth expectations as well as borrowing costs for consumers, businesses, and the government.

However, despite how the market often views the Fed, the central bank does not control all aspects of the economy. Many of their tools, such as the Federal Funds Rate, are often viewed as blunt instruments that work with what economists refer to as “long and variable lags.”

Economic shocks, technological change, demographics, and global events all play significant roles. For instance, the Fed can react to rising gasoline prices and the impact of AI on the job market, but they cannot control them directly.

What this means for investors is that while the Fed plays an important role, and interest rates do influence many parts of the economy and financial markets, focusing too much on each Fed decision can result in missing the forest for the trees.

Kevin Warsh believes in a more focused Fed

Like all government institutions, the Fed is imperfect and does not have a crystal ball as to where the economy might go next.

Instead, in making their decisions, they use the same public and private economic data on which all economists rely. So, it’s natural that there are frequent criticisms of the Fed in terms of specific policy decisions and as an institution.

As with all aspects of investing, it’s often important to set politics aside to better distinguish what the Fed might do from what we believe they ought to do.

In his recent Senate testimony, Warsh stated that he favors “a clearer, cleaner match between the Fed’s powers and responsibilities,” suggesting a preference for a more focused central bank.

He also emphasized that “monetary policy independence is essential” and that policymakers must act in the nation’s interest.

In the past, Warsh was seen as an “inflation hawk,” meaning that his policy preference would be to err on the side of higher interest rates to prevent inflation from rising, as well as promoting reform at the Fed.

A new framework?

When it comes to investing, there are at least three important implications based on Warsh’s public views and past actions.

1st, it will take time to fully understand how Warsh’s current views will impact policy in this inflationary environment, especially if they come into conflict with the White House’s preference for lower rates. He may need to address this as soon as his first press conference since high oil prices will weigh on upcoming Fed decisions.

That said, this would not be the first time there has been a conflict between the executive branch and the Fed since, naturally, elected officials prefer lower interest rates to boost the economy.

Famously, conflicts arose between President Ronald Reagan and Fed Chair Paul Volcker, and most recently between Donald Trump and Jerome Powell. This has occurred even when the Fed Chair is one appointed by the president.

2nd, while Warsh believes the Fed has overstepped on various historical policy initiatives, he has not argued for wholesale changes of the core of the institution.

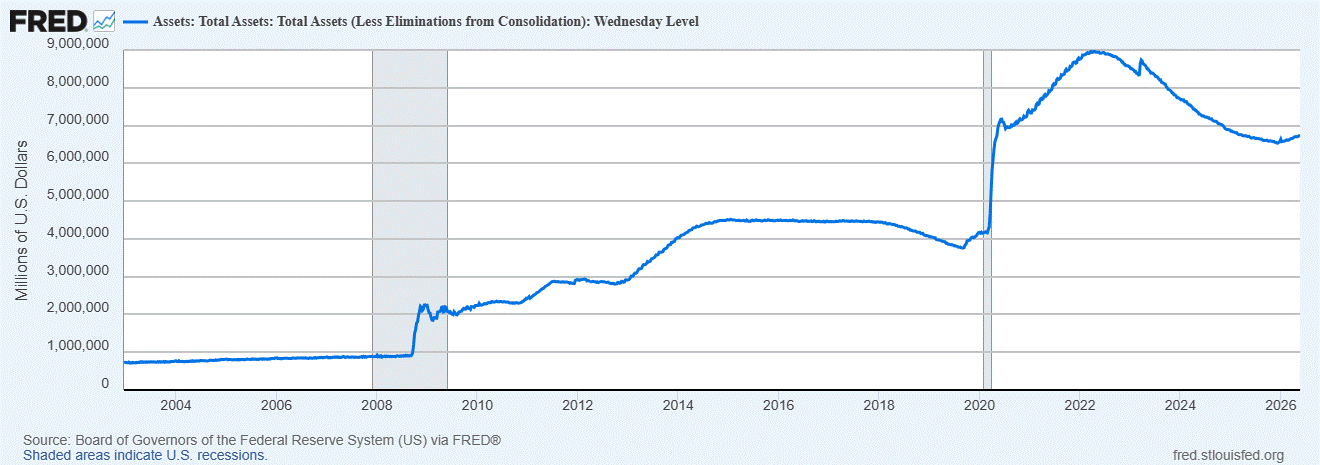

Specifically, Warsh believes that crisis-era actions such as the expansion of the Fed’s balance sheet were appropriate, since, after all, he was in the room when many of those decisions were made.

Instead, he does believe that the Fed should “retrace its steps” once conditions normalize and the crisis is over.

In other words, the Fed’s balance sheet, which remains sizable at $6.7 trillion, is not where it ought to be now that the 2008 financial crisis and the pandemic are long over.

In theory, shrinking the balance sheet should tighten financial conditions, since this involves either selling or reinvesting less each month in Treasury securities and mortgage-backed securities.

This is often known as “quantitative tightening,” the opposite of the easing done during crisis periods.

3rd, Warsh believes that Fed policy, especially since the pandemic, has contributed to the growth of the federal deficit and national debt.

Just as with the Fed’s balance sheet, he argues that while spending may be justified in recessions, it should be symmetric and monetary policymakers should steer clear of fiscal commentary.

Of course, the Fed does not directly control federal spending, and it’s unclear what the new Fed Chair would do differently to influence budgets passed by Congress. To the extent the Fed does weigh in on the size of the budget deficit, it would either be with guidance or by controlling interest rates.

What to expect in 2026

For now, the new Fed Chair inherits a particularly challenging economic environment.

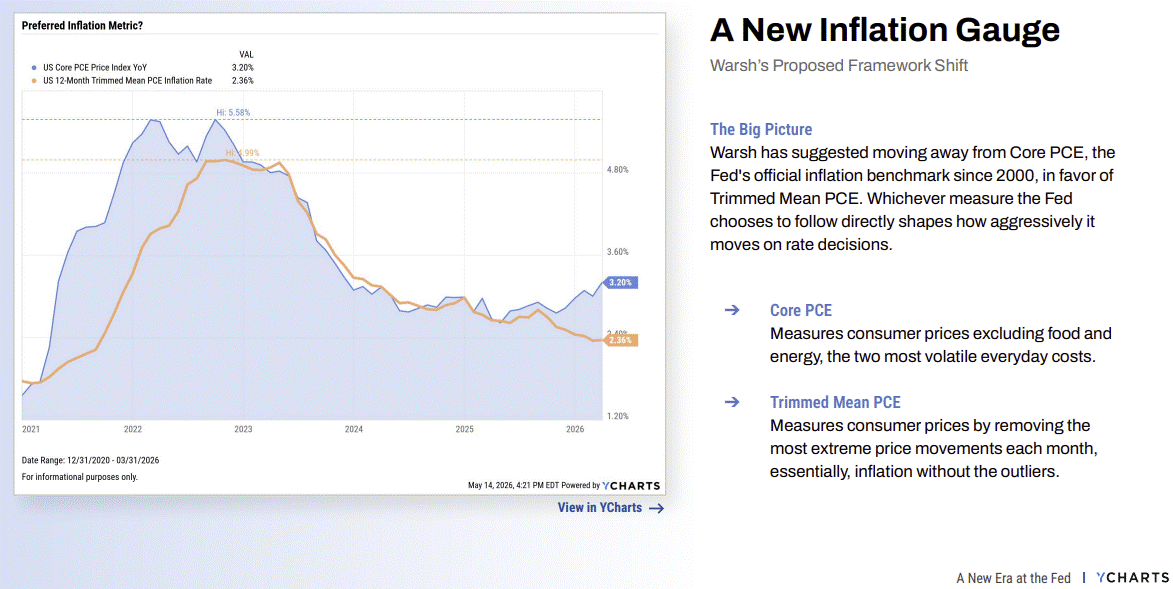

Inflation has accelerated in recent months due to higher oil and gasoline prices, driven by the war in Iran. Headline CPI was 3.8% year-over-year as of April 2026, with Core CPI at 2.8%, both still above the Fed’s 2% target.

On inflation, Warsh has floated the idea of moving away from Core PCE in favor of Trimmed Mean PCE.

At the same time, job growth has stalled over the past year.

This creates a difficult policy backdrop.

While many at the Fed and in markets had previously been expecting further rate cuts, Fed Funds Futures now reflect the possibility that the Fed may need to consider a rate increase by early 2027.

These market expectations should be taken with a grain of salt, as they shift frequently based on new economic data and global events. Still, they highlight the uncertain path ahead for monetary policy.

Bottom line

The most important takeaway is that markets and the economy have performed well across many different Fed leadership transitions and policy environments.

Changes at the top of the Fed naturally generate uncertainty, but they rarely alter the long-term fundamentals that drive financial markets.

Earnings growth, productivity, demographics, and innovation are ultimately the most important drivers of long-run returns.

Thus far, markets have generally responded favorably to Warsh’s nomination, viewing him as a known quantity with familiarity of the Fed and monetary policy.

Sources: YCharts, Clearnomics, Federal Reserve Bank of St. Louis

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures (click here)

Please see our SEC Registered firm brochure (click here)

Please see our SEC Registered Form CRS (click here)