🚨 Important reminder for us all: stocks bottom first 🚨

The Sandbox Daily (4.30.2025)

Welcome, Sandbox friends.

Today’s Daily discusses:

stocks bottom first

Let’s dig in.

Blake

Markets in review

EQUITIES: Dow +0.35% | S&P 500 +0.15% | Nasdaq 100 +0.13% | Russell 2000 -0.63%

FIXED INCOME: Barclays Agg Bond -0.09% | High Yield -0.53% | 2yr UST 3.619% | 10yr UST 4.175%

COMMODITIES: Brent Crude -1.76% to $63.12/barrel. Gold -0.97% to $3,301.3/oz.

BITCOIN: -0.37% to $94,607

US DOLLAR INDEX: +0.44% to 99.674

CBOE TOTAL PUT/CALL RATIO: 0.88

VIX: +2.19% to 24.70

Quote of the day

“It's a terrible thing, I think, in life to wait until you're ready. I have this feeling now that actually no one is every ready to do anything. There is almost no such thing as ready. There is only now.”

- Hugh Laurie

Stocks bottom first

One conversation after another, the same general question continues to pop up: why are markets rising on falling economic data and historic measures of uncertainty?

Remember, the stock market is a discounting mechanism – meaning its price reflects expectations about the future direction of economic activity, not necessarily historical events or even present conditions.

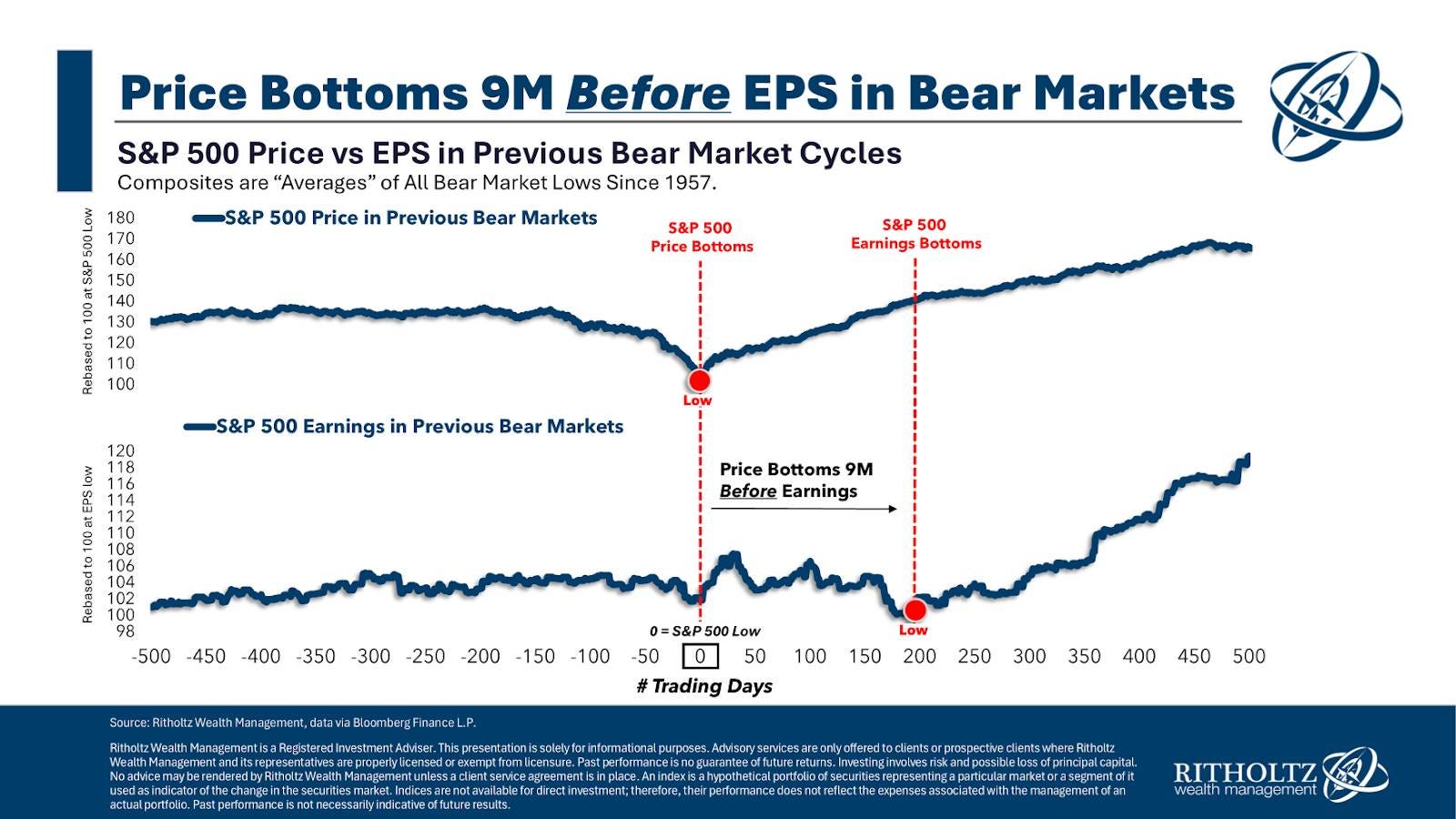

Stocks usually bottom before earnings-per-share growth (EPS), jobs, and gross domestic product (GDP) start to improve.

The market is always forward-looking in which stocks sniff out better times ahead and rally in the face of bad news. It stops going down while GDP, employment, and earnings continue to weaken.

We’ve seen this play out over cycles time and again. Reference the chart below – notice how the light blue line (S&P 500 index) troughs first.

Below, we review each of these four measures: stocks, economic growth (GDP), jobs, and earnings.

Stocks moving higher

Throughout 2025, U.S. stocks have taken their drubbing. That ground is well covered here.

International markets, on the other hand, tell a different story – beneficiaries of capital flight and dollar weakness.

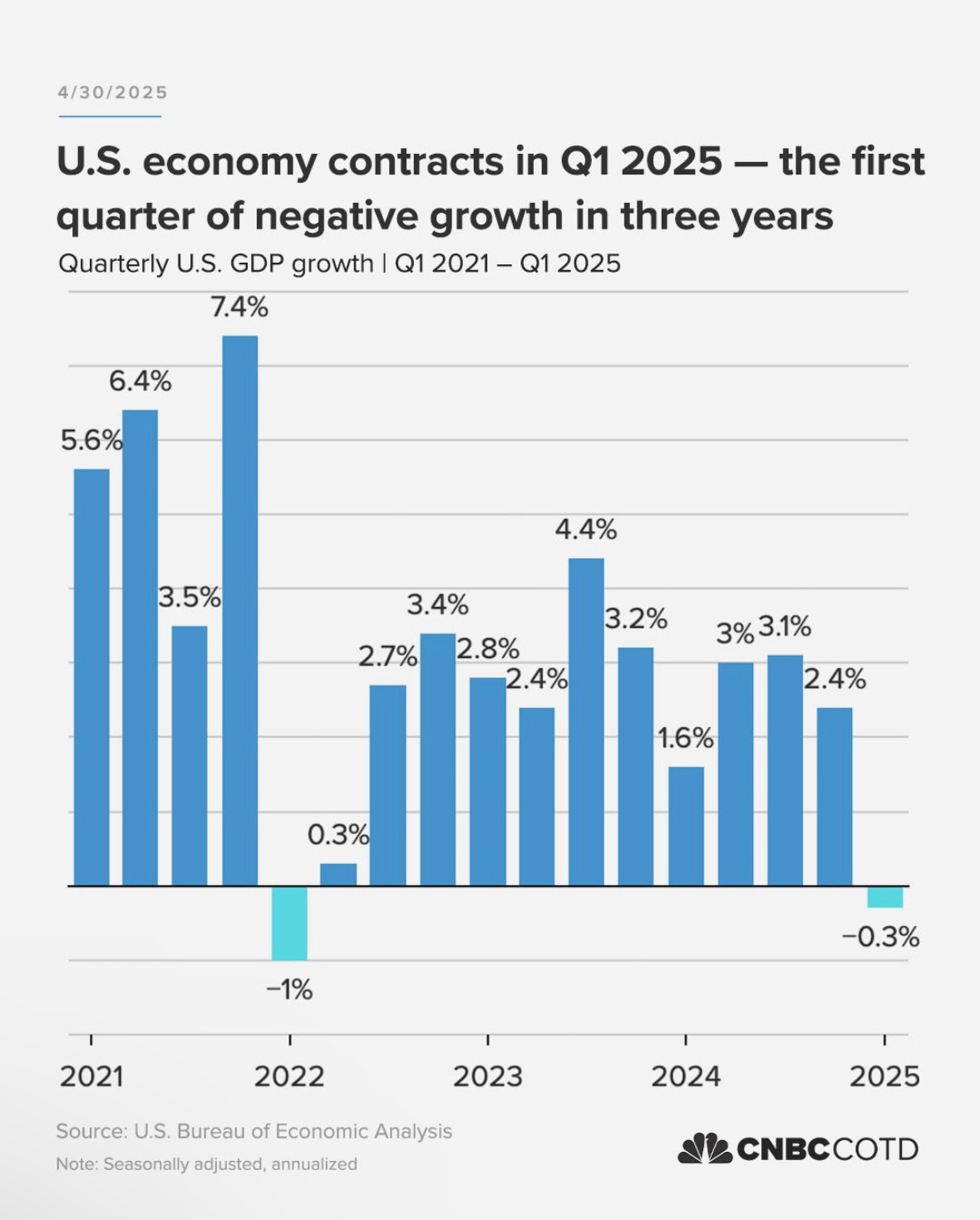

GDP contracting

This morning, we learned that U.S. real GDP fell at a worse-than-expected -0.3% annualized rate in Q1, posting its first decline in three years.

In short, the U.S. economy is going in reverse as we see some real evidence of President Trump’s abrupt policy shifts taking hold.

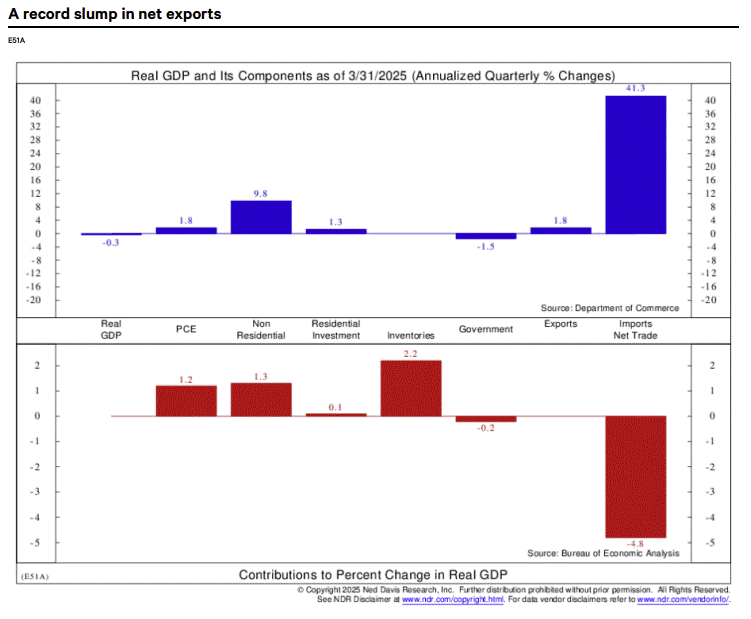

Net Exports were the red herring, as Imports soared 41.3% as expectations of hefty tariffs from the Trump administration front-loaded a surge in orders.

As a quicker refresher, U.S. Exports add to economic growth while foreign Imports detract.

As such, we are exactly halfway to the textbook definition of a recession – two consecutive quarters of negative GDP growth.

Labor market rebalancing

Today’s ADP payrolls report and yesterday’s Job Openings and Labor Turnover (JOLTS) report both show ongoing moderation in the labor market. We get the key report on Friday when the Bureau of Labor Statistics releases the April nonfarm payrolls report (consensus +130k).

ADP private sector employment growth decelerated significantly in April, marking the slowest pace of job creation in nine months.

"Unease is the word of the day," ADP chief economist Nela Richardson said in the release. "Employers are trying to reconcile policy and consumer uncertainty with a run of mostly positive economic data. It can be difficult to make hiring decisions in such an environment."

Yesterday, the JOLTS report showed that job openings fell 3.9% in March to a below-consensus 7.2 million, a six-month low. This is near the lowest level since December 2020 and is basically in line with the pre-pandemic level.

The Fed is closely watching the progress of labor demand/supply rebalancing, and taken together, the recent trends show the labor market has certainly continued to move toward better balance.

It’s yet another confirmation that labor market conditions have eased, green-lighting the Fed to cut rates further should their other policy goals (stable prices) continue to show their own moderation.

Earnings estimates falling

The final frontier, corporate earnings, remain the big mystery.

With many companies pulling their forward guidance, or providing two paths of guidance (business as usual vs. continued tariff overhang), the forward path of corporate profits remains murky at best.

While estimates have been falling all year, many feel there’s further to go. Only time will tell.

Using history as a guide, our friends at Ritholtz have shown that on average stocks have bottomed in price roughly nine months before earnings do. In other words, the market can push higher while the street continues taking down their earnings forecasts.

Quite the mental pretzel.

Sources: Michael Cembalest, YCharts, CNBC, Ned Davis Research, Yahoo Finance, Advisor Perspectives, Ritholtz Wealth Management

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures at the Sandbox Financial Partners website: