Inflation down (again), Tesla up (again)

The Sandbox Daily (6.13.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

CPI continues disinflation trend

Tesla races higher

Goldman lowers their recession forecast

spike in investor enthusiasm

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 +1.23% | Nasdaq 100 +0.79% | S&P 500 +0.69% | Dow +0.43%

FIXED INCOME: Barclays Agg Bond -0.47% | High Yield +0.12% | 2yr UST 4.679% | 10yr UST 3.827%

COMMODITIES: Brent Crude +3.09% to $74.06/barrel. Gold -0.71% to $1,955.8/oz.

BITCOIN: +0.18% to $25,909

US DOLLAR INDEX: -0.34% to 103.306

CBOE EQUITY PUT/CALL RATIO: 0.52

VIX: -2.66% to 14.61

Quote of the day

“You don’t achieve happiness by getting rid of your problems – you achieve it by learning from them.”

- Ray Dalio, Principles

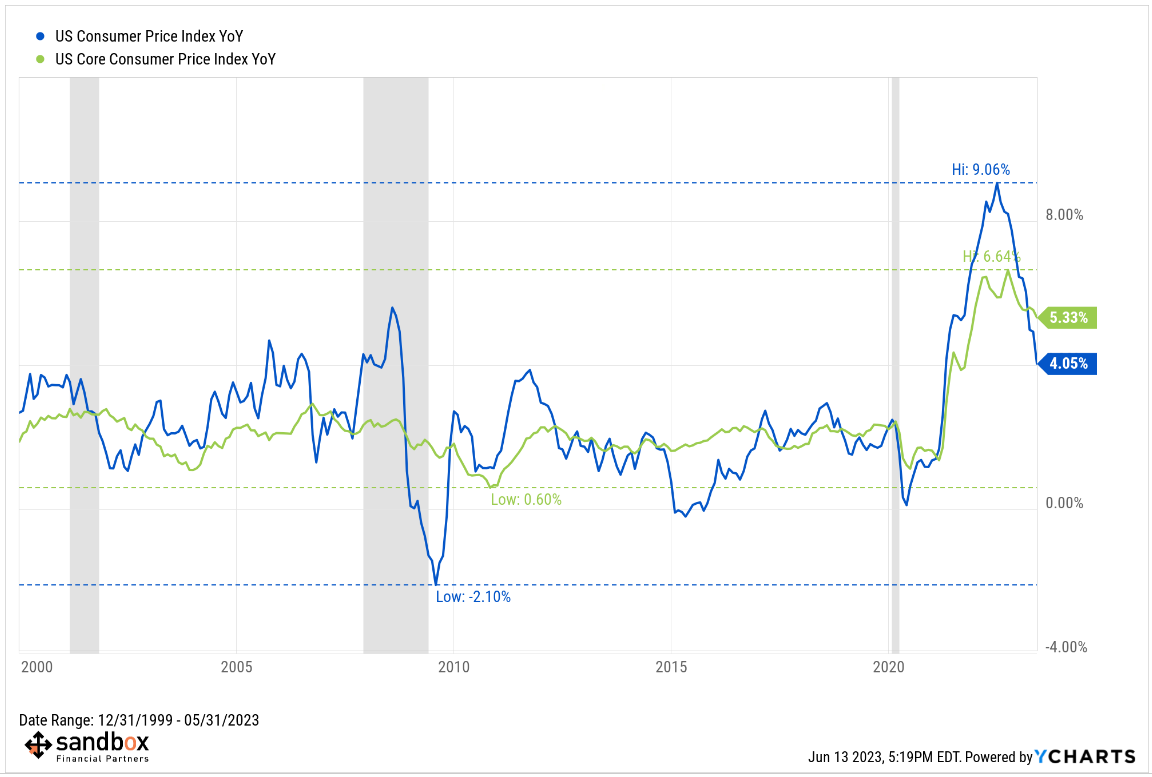

CPI continues disinflation trend

This morning, the U.S. Bureau of Labor Statistics released their Consumer Price Index (CPI) report for May. U.S. consumer prices held steady last month and came in line with market expectations.

Headline Inflation

CPI: +0.1% MoM, versus +0.1% estimate and prior month of +0.4%

CPI: +4.0% YoY, versus +4.1% estimate and prior month of +4.9%

Core Inflation

CPI ex-food and inflation: +0.4% MoM, versus +0.4% estimate and prior month of +0.4%

CPI ex-food and inflation: +5.3% YoY, versus +5.2% estimate and prior month of +5.5%

Headline CPI (+4.05%) moved down for 11th consecutive month in YoY rate of inflation and printed the slowest annualized increase since March 2021 (+2.62%). The table below shows the ramp up and subsequent ramp down in the YoY headline numbers. We are firmly off the cycle peak of +9.06% from last June.

Core CPI (ex-food & energy) moved down a few ticks to +5.33%. The lagging shelter category continues to be an issue and one of great contention; many Fed watchers would like to see other reputable, more high-frequency data incorporated into the FOMC’s analysis.

While prices are coming down, the rate at which its decreasing is slowing. The focus continues to be Core Services inflation (blue bar charts below).

Slower overall consumer price growth, but sticky core pressures, confirm that the path down to the Fed’s 2.0% inflation target will be bumpy.

While all of the core measures, particularly the super-core, are still running much hotter than the Fed’s liking, progress so far should be sufficient for a skip in rate hikes at tomorrow’s 2pm FOMC announcement. We can’t rule out another rate hike later in the year, but it is clear that the Fed is near the end of its tightening cycle. Given that monetary policy affects the real economy with a lag, many are expecting more of its constraining impact on growth to be felt in the 2nd half of 2023.

Source: Bureau of Labor Statistics, Ned Davis Research, Bloomberg

Tesla races higher

Tesla Inc. (TSLA) just registered its longest daily win streak since the stock came public almost 13 years ago. In a run that began back on May 25th, Tesla booked its 13th consecutive up-day today; the stock has returned more than 36% over that brief time.

The stock is up more than 130% from its year-to-date lows, putting it on the same leaderboard lists as other top stocks like Nvidia (NVDA) and Meta (META).

Here is the chart for Tesla, zoomed all the way out to its initial public offering (IPO) date, with the consecutive up-day indicator in the lower pane:

The previous record streak was in January 2021 after most of the gains of the post-COVID rally had been realized.

However, when we look back through history, there were a number of consecutive up-day extremes achieved in the early stages of new bull markets. This was the case in January 2013, October 2019, and April 2020.

Perhaps this kind of behavior is more consistent with the early stages of uptrends rather than the later ones.

Source: All Star Charts

Goldman lowers their recession forecast

The FOMC is likely to pause at its June meeting on Wednesday to let the haze clear before it considers another rate hike. The Fed leadership has signaled that it sees pausing as the prudent course because uncertainty about both the lagged effects of the rate hikes it has already delivered and the impact of tighter bank credit increases the risk of accidentally overtightening.

As such, Goldman Sachs believes that downside risks to the economy have already diminished and are lowering their estimation that the U.S. economy slips into a recession in the next 12 months from 35% to 25% (their general baseline for any given year).

Progress toward a soft landing remains on track, but there is further to go. Goldman cites three specifics.

1. The strongest evidence of progress comes from the labor market, where the jobs-workers gap, the quits rate, company reports of labor shortages, and wage growth have all fallen substantially.

2. Additionally, Core PCE inflation continues to show signs of deceleration; there’s much less reason for Fed officials to be as anxious as last summer because inflation psychology is normalizing and there are encouraging signs of cooling ahead.

3. Last, the tail risk of a disruptive debt ceiling fight has disappeared and the immediate risk of default and a credit rating downgrade are removed from the boil.

Source: Goldman Sachs Global Investment Research

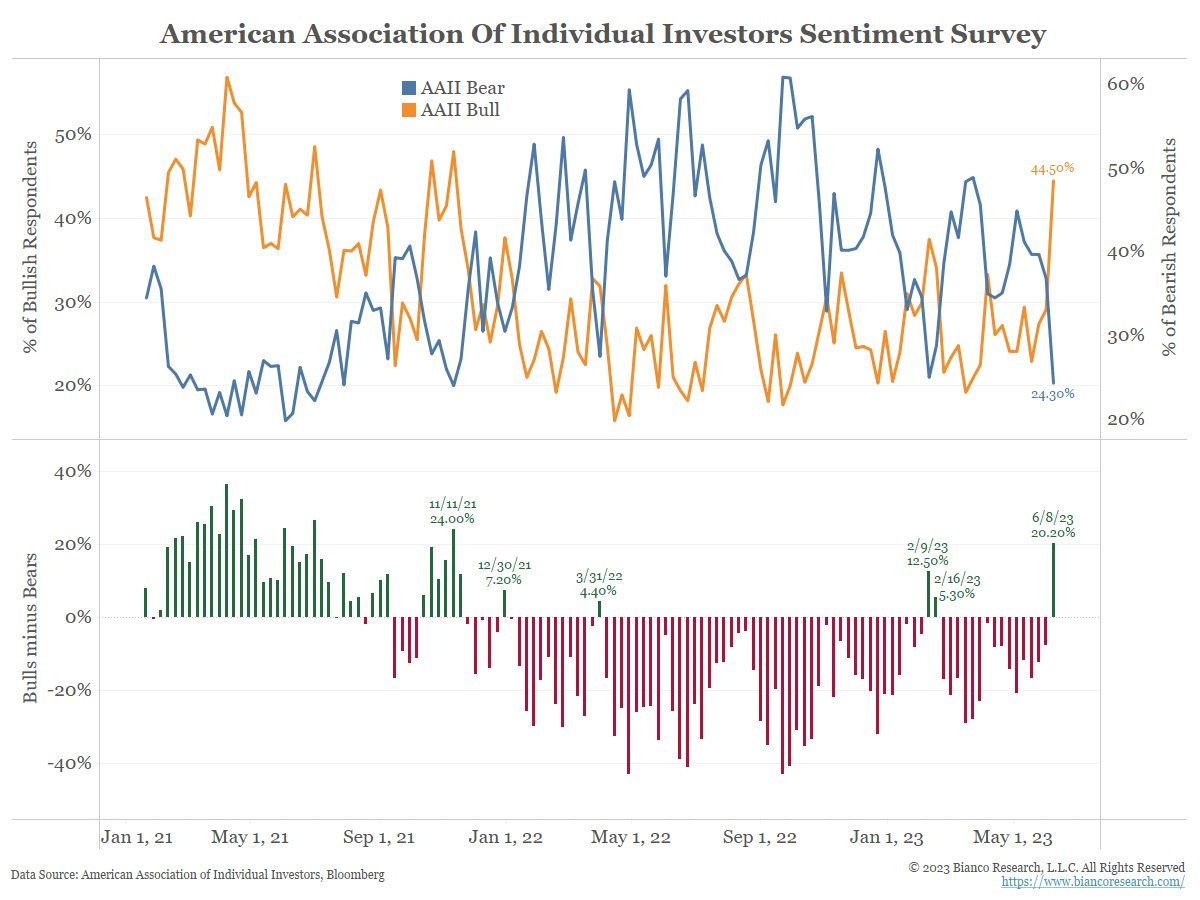

Spike in investor enthusiasm

For the first time since February, and for only the 3rd time in the last 14 months, bullish sentiment was above bearish sentiment. After all, the S&P 500 just put up its 4th consecutive weekly gain last week as market strength broadened out.

Last week’s net bullishness reading (bulls – bears) from the weekly survey conducted by the American Association of Individual Investors (AAII) jumped 20%.

This marked the highest net bullishness since November 2021, which was a few weeks before a 25% price decline.

Source: Bianco Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.