Investors enter key jobs report with elevated equity positions, plus the Mag 7 and Tech's earnings dominance

The Sandbox Daily (9.5.2024)

Welcome, Sandbox friends.

Today’s Daily discusses:

investors enter key jobs report with elevated equity positions

earnings growth is slowing for the Mag 7

Tech’s earnings dominance

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 +0.05% | S&P 500 -0.30% | Dow -0.54% | Russell 2000 -0.61%

FIXED INCOME: Barclays Agg Bond +0.26% | High Yield +0.34% | 2yr UST 3.748% | 10yr UST 3.731%

COMMODITIES: Brent Crude -0.08% to $72.64/barrel. Gold +0.77% to $2,545.5/oz.

BITCOIN: -3.54% to $56,120

US DOLLAR INDEX: -0.27% to 101.085

CBOE EQUITY PUT/CALL RATIO: 0.73

VIX: -6.66% to 19.90

Quote of the day

“Rotation is the lifeblood of any bull market.”

- Ralph Acampora, Co-Founder of the CMT Association

Investors enter key jobs report with elevated equity positions

There is great anticipation for the August U.S. jobs report to be released on Friday 9/6 as it will be key for investors in terms of gauging U.S. recession risk as well as how the Fed may pursue the early stages of its rate cutting cycle. Naturally, many are wondering how investors are positioned ahead of this key data release.

Proxies used for the retail impulse all suggest that the strong accumulation by investors into equities that started in late 2022 has persisted throughout 2024.

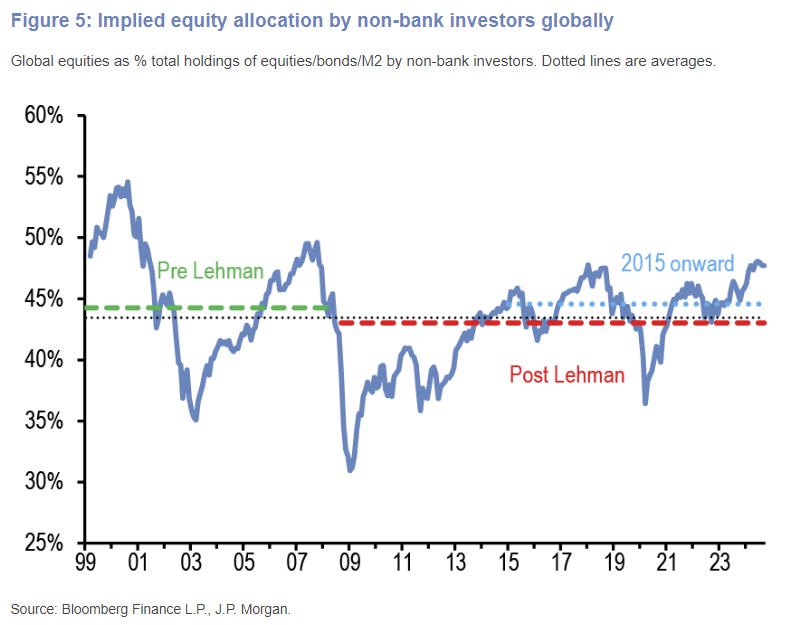

The chart below shows the implied allocations of non-bank investors to equities. At 46.5%, equity allocations are currently near the top-end of the post-GFC range and sit not far from the previous peak of 49.6% seen in October 2007.

Equity positioning still has never reclaimed the levels of ≥50% reached prior to the GFC, labeled below as “Pre-Lehman.”

In contrast to the positioning in stocks, the implied cash allocation has breached its previous historical low of 32.4% from August 2000.

Cash sitting extremely low by historical standards poses vulnerability to both equities and bonds going forward, unless buy-the-dip liquidity is sourced from the ~$6.2T of money market stock that remains on the sidelines.

Regarding large speculators, the Commitment of Traders (COT) report – a weekly publication produced by the Commodity Futures Trading Commission (CFTC) that shows the aggregate holdings of different asset managers and leveraged funds in the U.S. futures market – shows that equity positions as a share of open interest currently sits at 27%, near the upper end of its historical ranges but slightly lower from the recent peaks in mid-July of 31% that indicates some reduction in net longs.

This chart aggregates positions held in the S&P 500, Dow Jones, Nasdaq, and their respective mini futures contracts.

Source: J.P. Morgan Markets

Earnings growth is slowing for the Mag 7

The challenge we learned from Q2 earnings season is that several mega-caps are suffering from lofty expectations.

Sky-high EPS growth rates are difficult to repeat, especially by some of the largest and most profitable companies in the world. Six of the seven Mag 7 components are expected to see EPS growth slow in Q3 versus Q2. The exception is Tesla, which is expected to be less negative.

All but Telsa beat estimates in Q2. Four of the seven are expected to exceed consensus estimates of 16.8% for the S&P 500 in Q3.

Investors questioning the premium warranted for companies with superior, but decelerating, EPS growth could play into a pullback during the seasonally weak pre-election period.

Source: Ned Davis Research

Tech’s earnings dominance

Technology has been the most important driver of returns for the equity markets globally since the end of the Global Financial Crisis. The technology sector has generated 32% of the Global equity return and 40% of the U.S. equity market return since 2010.

Tech’s performance has far outstripped other major sectors, and with good justification. Earnings per share have surged while all industries together, outside of tech, have been relatively muted.

The constant introduction of new transformative technologies has attracted growing investor interest as well as competition and significant financial and human capital. This builds enthusiasm around the Tech narrative and drives stock prices higher, as long as earnings continue to underpin expectations.

Source: Goldman Sachs Global Investment Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.