Investors feeling gratitude this holiday season, plus market internals, seasonality, Intel, and Michigan (go blue !)

The Sandbox Daily (12.2.2024)

Welcome, Sandbox friends.

After a week off with family, friends, celebrating 40, and watching Michigan beat Ohio State again, we are back and feeling refreshed for the year-end push!

This Thanksgiving, we gave heartfelt thanks for the moments of togetherness and reflected on the love and support of our family and friends. It’s a time to pause, it’s a time to reflect, and above all, it’s a time to give thanks for the blessings that enrich our lives.

Oh yeah, and GO BLUE!

Today’s Daily discusses:

feeling gratitude this holiday weekend

market internals confirm price

seasonality favors year-end push higher

Gelsinger out at Intel before completing turnaround plan

Let’s dig in.

Blake

Markets in review

EQUITIES: Nasdaq 100 +1.12% | S&P 500 +0.24% | Russell 2000 -0.02% | Dow -0.29%

FIXED INCOME: Barclays Agg Bond +0.01% | High Yield -0.04% | 2yr UST 4.186% | 10yr UST 4.192%

COMMODITIES: Brent Crude +0.10% to $71.91/barrel. Gold -0.71% to $2,662.1/oz.

BITCOIN: -2.48% to $95,358

US DOLLAR INDEX: +0.62% to 106.388

CBOE TOTAL PUT/CALL RATIO: 0.86

VIX: -1.26% to 13.34

Quote of the day

“If you do not change direction, you may end up where you are heading.”

- Lao Tzu

Investors feeling gratitude this holiday season

After a historic year, investors have much to be thankful for this holiday season.

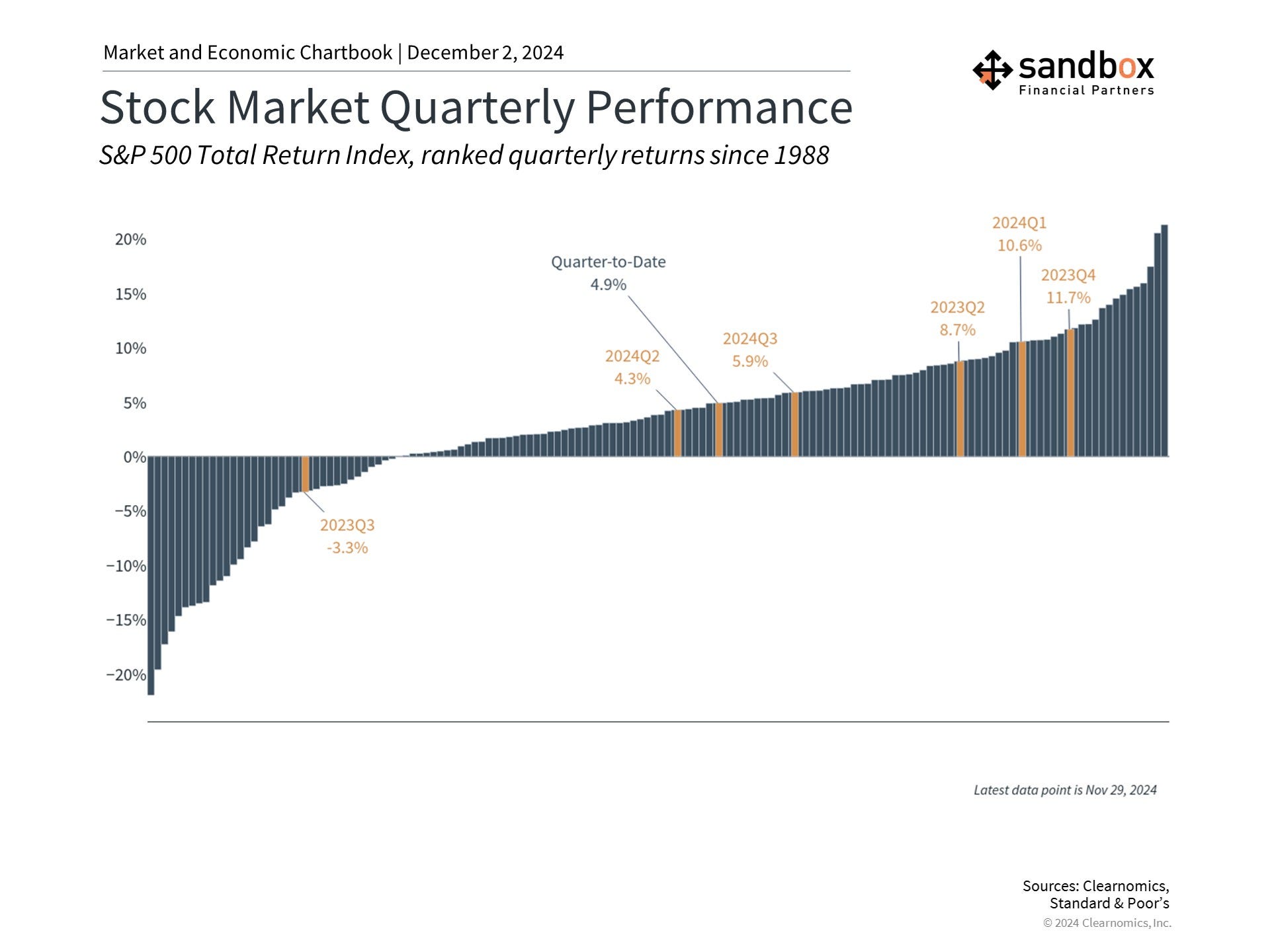

Despite periods of uncertainty around Federal Reserve monetary policy, the U.S. presidential election, and geopolitical conflicts, the stock market has delivered exceptional returns in 2024. With only a few weeks left in the year, the S&P 500 has gained +27% with dividends year-to-date, the Dow +19%, and the Nasdaq +27%. International stocks have also performed well, with Emerging Markets advancing +9% and Developed Markets +5%. Economic growth has exceeded expectations, with inflation returning to pre-pandemic levels, unemployment still low, and GDP growing steadily.

The U.S. stock market, in particular, has demonstrated impressive strength in 2024. This is due to robust corporate earnings, better-than-expected economic conditions, and improving investor confidence. With the exception of one quarter (3Q23), the last two years have experienced steady positive market returns.

While AI and technology stocks have led the way (and gained all the mainstream media headlines), many other sectors have contributed this year as well.

In fact, nearly all parts of the market are positive year-to-date, while ten of the eleven S&P 500 sectors have generated double-digit total returns.

The strong bull market since the end of 2022 does mean that valuations are no longer as attractive. The forward price-to-earnings ratio for the S&P 500 is now 22.2, nearing both recent highs in 2021 and the dot-com peak of 24.5.

Rather than a reason to avoid the stock market, stretched valuations are a reminder to hold a properly constructed portfolio.

Owning stocks, or any risk asset, needs to be balanced within and across asset classes, such as bonds or commodities or alternatives, to achieve portfolio goals.

The end of the year is a perfect time to review your asset allocation, especially after this year’s market movements.

Source: Clearnomics, J.P. Morgan Guide to the Markets

{kind=link}

Market internals confirm price

As the stock market continues to make one new all-time high after another – 54 new all-time highs for the S&P 500 in 2024, as of today’s close – it’s important to look towards market breadth as confirmation in the strength of the underlying market.

With more stocks pushing higher and participation expanding, it’s no surprise to see the NYSE Advance-Decline Line is at all-time highs.

An Advance-Decline Line is calculated by taking the difference between Advancing stocks and Declining stocks on a given day, and then adding that result to the prior day's already existing A-D line. And, when the world’s most important universe of stocks is pushing higher time and again, it becomes an informative measure of market breadth that confirms the price action we’re seeing among the major index averages.

Intuitively, if more stocks are going up than down, then we should likely see an absence of activity in the New Lows lists. And that’s precisely what is happening now.

While the 52-week New Lows list has been gathering dust much of the year – much like Ohio State’s recent win total against Michigan, or their program’s lack of championship hardware in general – even the more short-dated New Lows lists have witnessed a marked slowdown, which currently measures… 0%.

In fact, no matter what size, style, or sector you look at, the New Lows list is nothing more than tumbleweeds across all time frames.

If the general trend is higher, we should be looking at our shopping lists for stocks to buy, not sell.

Source: Walter Deemer, Grant Hawkridge, Bloomberg, All Star Charts

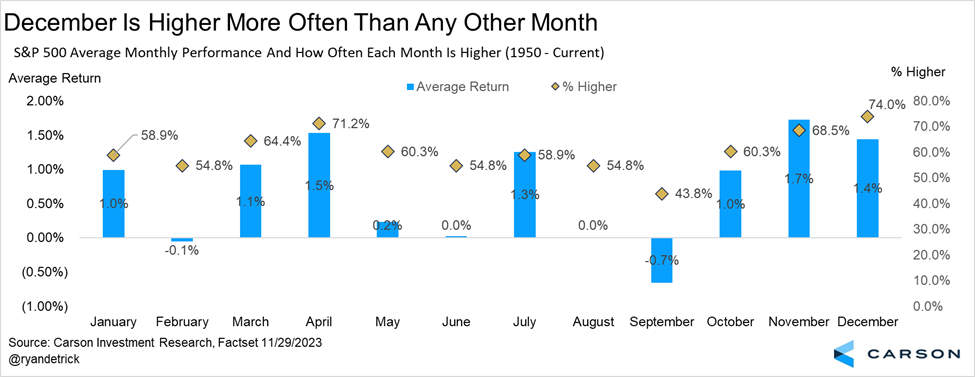

Seasonality favors year-end push higher

The S&P 500 heads into December with seasonal winds at its back – looking to add further gains to its already robust performance in 2024.

Since 1950, the S&P 500 in December has been higher 74% of the time, with an average monthly return of +1.4%.

Source: Ryan Detrick

Gelsinger out at Intel before completing turnaround plan

Pat Gelsinger has retired as CEO of Intel (INTC) while also stepping down from its board of directors after nearly four years running the company. Gelsinger started with Intel in 1979 and worked most of his professional career with the company, with the exception of serving as CEO for VMware from 2012-2021.

Once the bedrock of Silicon Valley’s global dominance in chips, Intel is a shell of its former self. Gelsinger’s tenure ended somewhat unceremoniously and was marked by turbulence in recent months.

To wit:

August 2024: Intel laid of 15,000 employees and suspended its dividend which had been in place since 1992

September 2024: Intel reportedly was approached by Qualcomm for takeover bid

October 2024: company reported $16.6B loss in Q3

November 2024: Intel was removed from the Dow Jones Industrial Average and received $600M less than initially expected from the finalized CHIPS Act

Intel’s stock has been cut in half and then some since Pat Gelsinger took over as the company’s CEO.

Many are hoping to see the next CEO has the technical and manufacturing chops for this turnaround story.

Source: Intel, Yahoo Finance

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures at the Sandbox Financial Partners website: