Is home ownership still within reach in today’s economy?

The Sandbox Daily (6.24.2025)

Welcome, Sandbox friends.

Today’s Daily discusses:

the great affordability crisis

Let’s dig in.

Blake

Markets in review

EQUITIES: Nasdaq 100 +1.53% | Russell 2000 +1.34% | Dow +1.19% | S&P 500 +1.11%

FIXED INCOME: Barclays Agg Bond +0.41% | High Yield +0.28% | 2yr UST 3.819% | 10yr UST 4.294%

COMMODITIES: Brent Crude -5.19% to $67.80/barrel. Gold -1.70% to $3,337.5/oz.

BITCOIN: +1.87% to $105,918

US DOLLAR INDEX: -0.46% to 97.964

CBOE TOTAL PUT/CALL RATIO: 0.95

VIX: -11.85% to 17.48

Quote of the day

“They laugh at me because I'm different. I laugh at them because they are the same.”

- Kurt Cobain

Is home ownership still within reach in today’s economy?

The most enduring post-pandemic challenge remains the great affordability crisis in the housing market.

Just one-in-five people in 2019 thought that home prices would rise by 20% or more over the subsequent 5 years, according to a New York Fed survey of consumers.

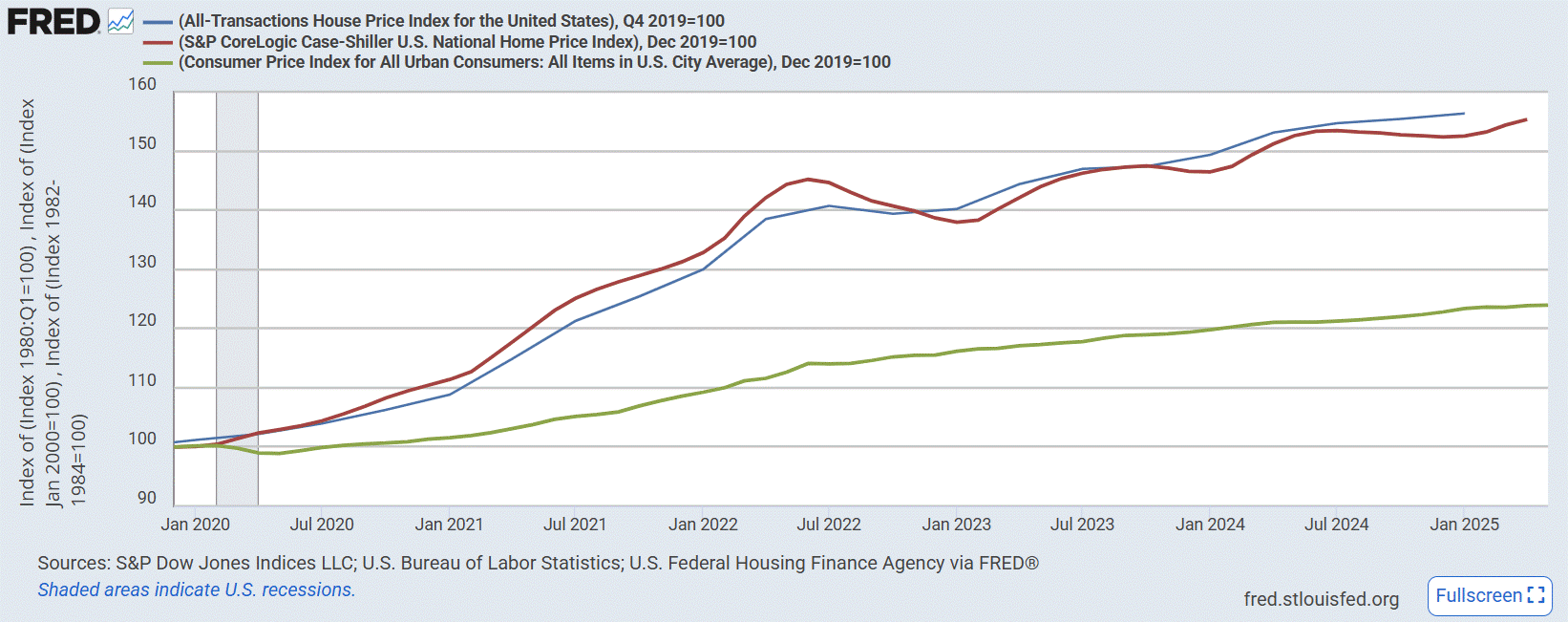

And yet, over that five-year time frame, nationwide home price indices would rise by roughly 55%, indicating how far the housing market moved relative to expectations.

In fact, home-related inflation (red line) rose by more than double the pace of broad-based inflation, as measured by CPI (green line).

Meanwhile, the 30-year fixed mortgage rate rose from 3.7% at year-end 2019 to 6.9% by 2024.

This combination of higher prices and elevated rates caused monthly mortgage costs to double for would-be buyers.

How bad is it?

Here’s the math (yes, there’s a lot of it coming below):

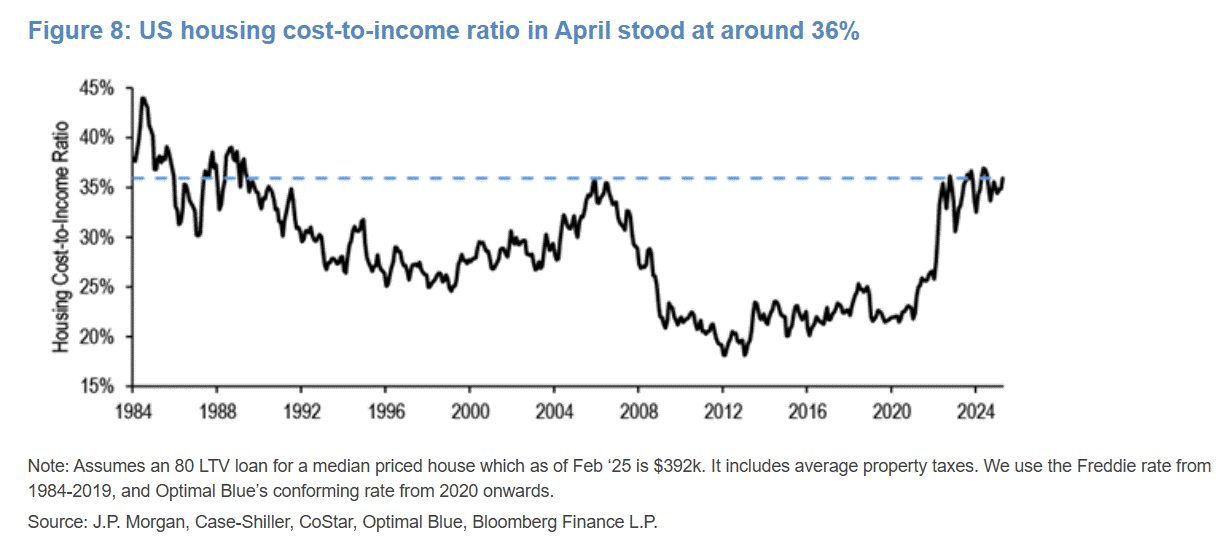

A hypothetical homebuyer in 2024 would need to spend ~45% more of their income on mortgage payments than in 2019.

Stated differently, a mortgage with monthly expenses equal to 40% of take-home pay in 2019 would take 58% of 2024 take home pay, assuming median growth in incomes.

Historically, nominal incomes and home prices would tend to move together, albeit imperfectly, which helped stabilize the portion of household budgets that went toward housing.

More recently, that relationship has fallen out of balance.

Increases to both home prices and interest rates have shifted the cost of home ownership upward in 2024, relative to changes in household income, by the most since the early 1980s.

Below, notice how the blue markings (2019-2024) on the “affordability worsening” scale are historically the worst, only outdone by the late 1970s when inflation was at its worst.

Presented another way, this data from the National Association of Realtors visually displays the affordability constraints on the average household.

What’s worse, this appears to be a somewhat global phenomena.

Housing affordability across 40 countries is worse than at any time since the Global Financial Crisis, and the post-pandemic sudden deterioration in affordability stands out.

A housing affordability index (HAI) rating below 100 indicates a household has less income than necessary to qualify for a typical mortgage.

Additional factors are to blame here, including undersupply of new construction, changing preferences (rentals, post-pandemic regional shifts, slower household formation, etc.), stricter permitting regulations, and competition coming from wealthier, cash-rich older generations.

Today, the U.S. housing market is best characterized as frozen.

At the start of 2025, there was considerable optimism that some of the housing affordability pressures might abate as mortgage rates were drifting down on expectations for Fed easing.

However, with the increased concern about a global slowdown and greater U.S. equity market volatility, housing demand has fallen while mortgage rates have increased.

The housing market’s slump is getting worse as tariffs are making home construction more expensive, while deportation threatens immigrant labor in construction.

Where it goes from here is likely a slow and steady thaw.

Sources: New York Fed, JP Morgan, St. Louis Fed, National Association of Realtors

That’s all for today.

Blake

Questions about your financial goals or future?

Connect with a Sandbox financial advisor – our team is here to support you every step of the way!

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

Please see additional disclosures (click here)

Please see our SEC Registered firm brochure (click here)

Please see our SEC Registered Form CRS (click here)