Jobs report, plus Elon battles Apple, U.S. paper currency, and the week in review

The Sandbox Daily (12.2.2022)

Welcome, Sandbox friends.

Today’s Daily discusses the strong November jobs report, Elon Musk brings the spotlight back on Apple, the security underlying U.S. paper currency, and a brief recap to snapshot the week in markets.

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 +0.59% | Dow +0.10% | S&P 500 -0.12% | Nasdaq 100 -0.40%

FIXED INCOME: Barclays Agg Bond +0.41% | High Yield -0.08% | 2yr UST 4.284% | 10yr UST 3.492%

COMMODITIES: Brent Crude -1.70% to $85.55/barrel. Gold +1.21% to $1,809.6/oz.

BITCOIN: +0.48% to $17,052

US DOLLAR INDEX: -0.21% to 104.506

CBOE EQUITY PUT/CALL RATIO: 0.81

VIX: -3.93% to 19.06

Labor market surprisingly resilient

The Labor Department's release of its November jobs report showed nonfarm payrolls expanded by 263,000 in November, above the consensus expectation of 200,000.

The unemployment rate remained at 3.7%, matching expectations, as the participation rate dropped yet again.

The big surprise was the jump in average hourly earnings to nearly +0.6%, almost double expectations of +0.3%. Although this likely won’t deter the Fed from downshifting in December to 50 bp, how many more hikes will be needed next year remains an open question, as the economy is not in recession.

Source: U.S. Bureau of Labor Statistics, Ned Davis Research, Bloomberg

Why Elon Musk went to war with Apple

Earlier this week, Elon Musk tweeted that Apple had “threatened to withhold Twitter from its App Store,” unleashing a tirade of tweets criticizing the company for inconsistent “censorship” and building on previous complaints about Apple’s App Store fees, which he has called “a 30% tax on the internet”.

Screenshots seen by Platformer show that weekly advertising bookings in Twitter’s EMEA region are down 49% — hastening the need for Twitter to shift their revenue towards subscriptions. The problem for Musk is that subscriptions will incur Apple’s hefty App Store fee.

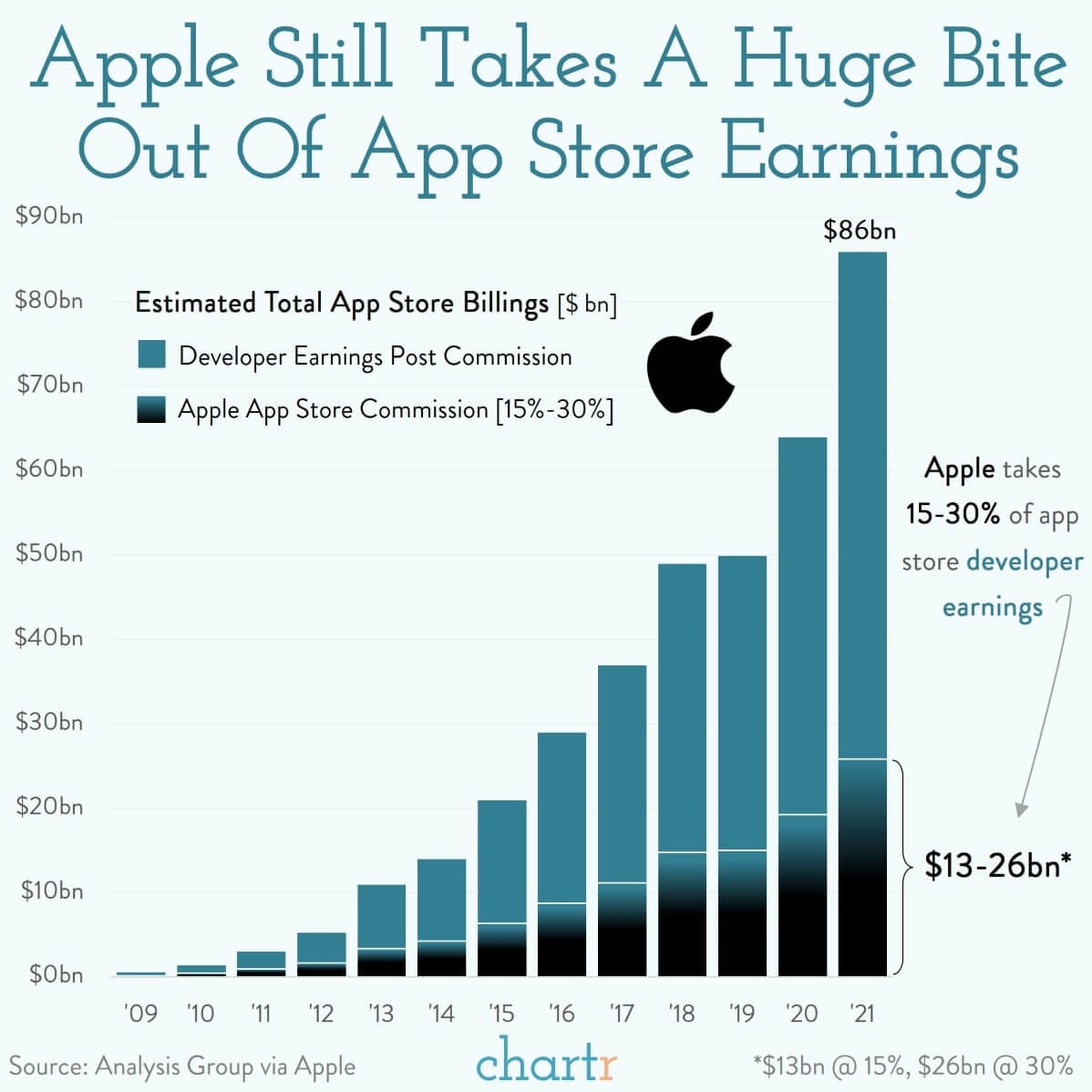

Musk’s comments put Apple’s “in-app purchase” policy, in which it takes a 15-30% rake of digital purchases from App Store apps, back in the spotlight. A very bright spotlight. As the Apple ecosystem has grown, the App Store has been a remarkable marketplace for app developers to reach the 1.2bn+ iPhone users — and its earned Apple a fortune in the process.

Figures from Analysis Group, endorsed by Apple, show that some ~$86bn is estimated to have been made by developers in 2021, with Apple’s cut of that likely towards the top end of the $13-26bn range. The iPhone maker claims to use this to cover costs in reviewing apps, in order to protect consumers, but the lack of alternatives for developers has led to calls of anticompetitive practices.

Source: Chartr

The makeup of American paper currency

There are 6 key features that identify real bills and protect the falsification of American money. Let’s run through them:

serial numbers and the EURion Constellation (star-like grouping of yellow rings near the serial number)

color changing ink at different angles thanks to small metallic flakes within the ink itself

microprinting allows for verifiable images that cannot be scanned by photocopiers or seen by the naked eye

intaglio printing uses magnetic ink and every different bill value has a unique magnetic signature

a security thread embedded and running through the bill seen only under UV light

Blue and red cloth fibers are woven into the material as well as the use of watermarks

Source: Visual Capitalist

The week in review

Market drivers: Good week for stocks overall with the lower rate backdrop stemming from the dovish spin surrounding Powell’s comments on Wednesday. Stronger November nonfarm payroll and wage growth the big story today. This plays into concerns about upside risk to terminal rate and Fed's heightened emphasis on a higher-for-longer rate policy. However, labor market resilience also provides some cushion against the hard-landing and earnings risk themes that have been flagged as big headwinds for stocks in 2023. Also more signs of a shift away from zero-Covid policy in China, along with the implementation of property support measures.

Stocks: The major markets finished higher this week as Federal Reserve (Fed) Chairman Powell on Wednesday signaled smaller interest rate hikes during upcoming FOMC meetings amid improving inflationary conditions. Given discussions of interest rate stability, growth sectors communication services along consumer discretionary led this week’s market results. The energy sector lagged the markets this week on lower energy commodity prices.

For the month of November, the Dow Jones Industrial Average closed up more than 20% off its September 30, 2022 closing low, which many interpret as the end of the bear market for the granddaddy of the modern equity index. The S&P 500 had consecutive months higher for the first time since August 2021, the fifth longest streak all time dating back to 1928 (including the S&P 500’s predecessor indexes).

Bonds: The Bloomberg Aggregate Bond Index finished the week higher as yields continue to decline on expectations of a less aggressive Fed. Markets have embraced a downshift in Fed rate hikes, with a fifth consecutive 75 bps hike next month no longer the consensus. In addition, high-yield corporate bonds, as tracked by the Bloomberg High Yield index, gained ground for the week.

Commodities: Oil and natural gas prices finished the week little changed. Last week, U.S. West Texas Intermediate (WTI) crude oil reached prices not seen since December 22nd of last year amid the softening fuel demand outlook, especially in China. The major metals (gold, silver, and copper) finished the week solidly higher.

Source: Dwyer Strategy, LPL Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.