Leadership within the S&P 500, plus AI/cybersecurity, volatility, and Charlie Munger

The Sandbox Daily (11.28.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

lowest share of stocks outperforming the index in over three decades

A.I. and cybersecurity: new tech, new threats

broad asset class volatility compression, except within rates

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 +0.30% | Dow +0.24% | S&P 500 +0.10% | Russell 2000 -0.46%

FIXED INCOME: Barclays Agg Bond +0.44% | High Yield +0.44% | 2yr UST 4.738% | 10yr UST 4.323%

COMMODITIES: Brent Crude +2.01% to $81.58/barrel. Gold +1.45% to $2,062.5/oz.

BITCOIN: +2.64% to $37,978

US DOLLAR INDEX: -0.45% to 102.732

CBOE EQUITY PUT/CALL RATIO: 0.87

VIX: no change to 12.69

Quote of the day – Charlie Munger, in memorium

“I constantly see people rise in life who are not the smartest, sometimes not even the most diligent, but they are learning machines. They go to bed every night a little wiser than they were when they got up and boy does that help, particularly when you have a long run ahead of you.”

- Charlie Munger, Vice Chairman of Berkshire Hathaway (1924-2023, RIP)

Lowest share of stocks outperforming the index in over three decades

Narrow leadership has been a lingering issue for the stock market in 2023.

We all know the S&P7 – the “Magnificent 7” (AAPL, MSFT, GOOGL, AMZN, NVDA, META, TSLA) – is already up 80% this year and have an average forward P/E ratio of 29x, while the remaining S&P493 have returned just 7% and sport a more affordable 17x multiple.

This performance disparity ironically masks the underlying weakness across the broader market because the cap-weighted indexes skew higher from the performance contribution coming from the largest companies, i.e. the Mag 7.

The breadth issue becomes strikingly obvious when simply counting the number of index constituents outperforming the index itself.

The current share is close to 25%, which is the lowest in over three decades and just half the median figure (49%). In fact, the narrow leadership of 2023 more closely resembles 1998 and 1999.

To be clear, the story isn’t 7 stocks going up while 493 are going down. Quite the contrary.

6 of the 11 index sectors are green in 2023. The problem remains strength (across sectors and at the individual level) relative to the index itself, which is limited to Tech and Tech-adjacent areas (right column is relative performance, 3 green and 8 red):

Perhaps the winds are changing as we speak, though – more stocks made new 52-week highs than lows for the first time in 16 weeks.

After all, in bull markets, more stocks are going up than going down.

But, the lack of breadth expansion has caused many investors to pump the brakes on this young bull market, who may share the following view as expressed from Richard Bernstein Advisors:

“Narrow leadership is typically the result of deteriorating fundamentals in the broader market. When the profits cycle decelerates, investors gravitate to the fewer and fewer companies that can maintain growth during an increasingly adverse backdrop. Leadership narrows as fundamentals deteriorate, and growth becomes scarce.”

OR, perhaps the stark dichotomy between this year’s winners and losers is justified based on fundamentals (alongside investors’ enthusiasm).

The Magnificent 7 collectively have stronger balance sheets, faster expected 2023-25 CAGR sales growth (11% vs. 3%), higher 2023 margins (22% vs. 10%), and a greater re-investment ratio (61% vs. 18%) than the other 493 stocks – while trading at a relative valuation in line with recent averages after accounting for expected growth (0.9x relative PEG ratio).

So, perhaps the argument one could make is that the risk/reward profile of the Magnificent 7 vs. the S&P493 is not especially compelling given elevated expectations.

Source: Torset Slok, Richard Bernstein Advisors, Grindstone Intelligence, Hi Mount Research, Goldman Sachs Global Investment Research

New tech, new threats

AI’s potential for transformation is without question the story of 2023 and the future as seen in the tech-heavy Nasdaq 100 Composite which is up a staggering +46% year-to-date.

However, AD-driven advancements in cyber warfare pose an emerging geopolitical and business security threat with the potential to cause systemic destabilization, with cyberattacks supercharged through AI-enhanced surveillance as well as disinformation campaigns.

Nearly 50% of business leaders indicate that geopolitical instability is causing them to re-evaluate the countries with which they do business according to the World Economic Forum’s Global Cybersecurity Outlook 2023, citing business continuity and reputational damage as the key concerns.

And businesses are backing up their words with action.

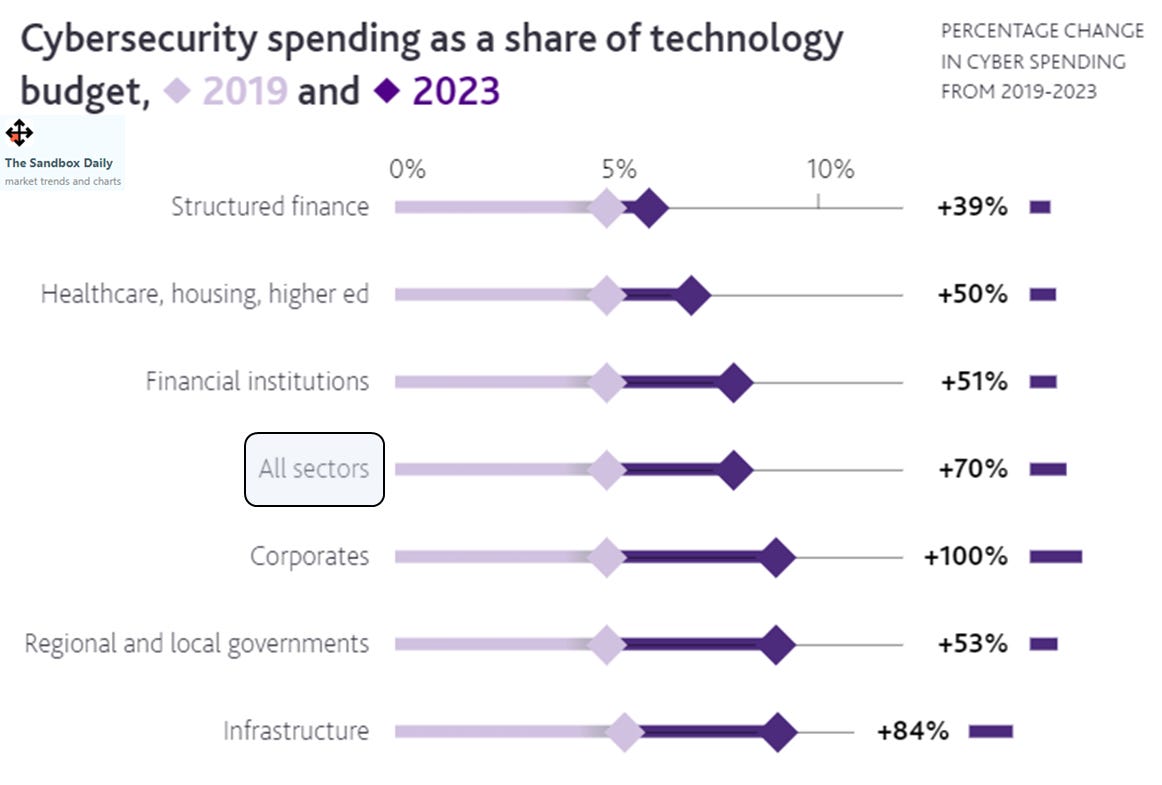

A recent Moody’s survey highlights that cybersecurity spending as a share of technology budget has increased by 70% across all sectors between 2019 and 2023.

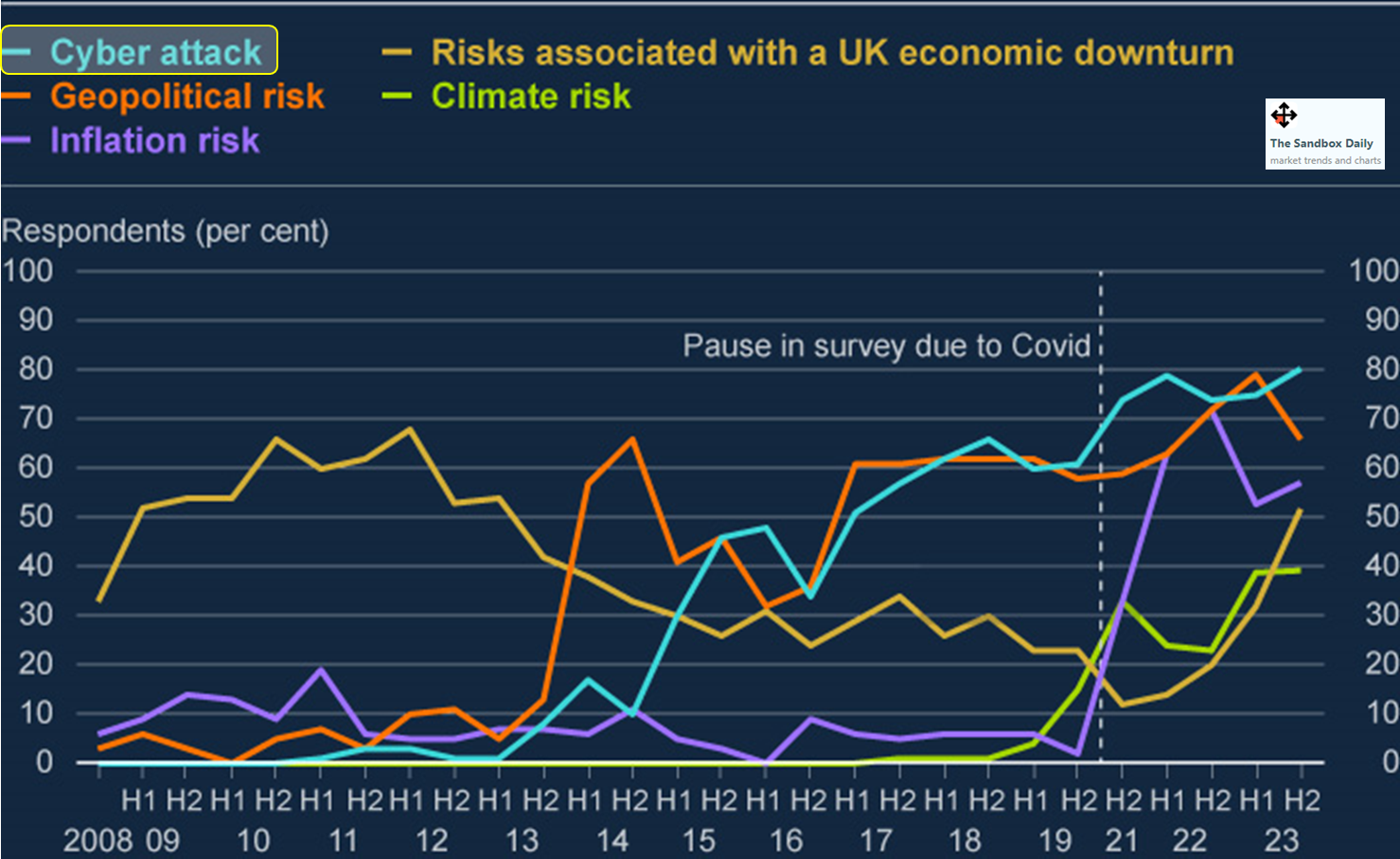

Cyber events, especially cyberattacks, are already among the top and most frequently cited risks in financial stability surveys in the U.S. and globally.

The recent ransomware attack on the Industrial & Commercial Bank of China (ICBC), the world’s largest lender by assets, temporarily disrupted trades and liquidity in the US Treasury market. This event highlights how malicious actors could expose vulnerabilities in the financial system and set off a cascade of disruption to financial stability.

Bank of England's Systemic Risk Survey lists cyberattacks, along with geopolitical risks, as the most frequently cited risks among participants – with cyber at its highest level recorded in the history of this survey.

Source: J.P. Morgan Markets, World Economic Forum, Moody’s, Bank of England

Broad asset class volatility compression, except within rates

The VIX Index declined to a post-pandemic low of 12.5 on Friday, further widening the gap between implied equity volatility (VIX index) and rates volatility (MOVE index).

In fact, cross-asset volatility has continued to reset lower across the board, supported by markets further embracing the more goldilocks backdrop in the U.S. with faster-than-expected inflation normalization and growth remaining resilient.

Rate volatility remains disconnected from the other major asset classes, an outlier at historically elevated levels.

Source: Goldman Sachs Global Investment Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.