Market bears head for the locker room, plus gasoline prices, geopolitics and risk premia, and time horizons

The Sandbox Daily (12.19.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

market bears head for the locker room

wealth effect back just in time for the holidays

low risk premia ahead of busy 2024 geopolitical calendar

short-term pain, long-term gain

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 +1.94% | Dow +0.68% | S&P 500 +0.59% | Nasdaq 100 +0.49%

FIXED INCOME: Barclays Agg Bond +0.12% | High Yield +0.29% | 2yr UST 4.444% | 10yr UST 3.933%

COMMODITIES: Brent Crude +1.72% to $79.29/barrel. Gold +0.64% to $2,053.6/oz.

BITCOIN: +0.19% to $42,428

US DOLLAR INDEX: -0.42% to 102.136

CBOE EQUITY PUT/CALL RATIO: 0.57

VIX: -0.24% to 12.53

Quote of the day

“It’s waiting that helps you as an investor, and a lot of people just can’t stand to wait.”

- Charlie Munger

Market bears head for the locker room

The bull market is open for business.

I’m seeing a wholesale change in tone from the market strategists and traders on CNBC to the business- and finance-focused podcasts to the fast-capitulating bears, even the dad’s in attendance last night at K-2 rec basketball in Annapolis, Maryland.

It takes me back to my AAA playing days in the hockey rinks around Chicago when the five guys on the ice screwed up so royally – like giving up 2 goals in the same shift, for instance – that when the shift ended and you couldn’t focus between the steam emanating from your head coach’s forehead or the expletives being leveled at you, the only place on the bench appropriate for those 5 skaters was at the end of the pine. Past the guys who were injured or not in uniform for deficient grades. You were done for the night. Time to untie the laces.

That’s where you will find the bear market case, these days – practically back in the locker room getting undressed.

Last week, Federal Reserve Chairman Jerome Powell decided enough was enough. Enough with the war on inflation, back to managing the business cycle. The most aggressive monetary policy tightening cycle in 4+ decades is coming to an end.

The chart below from Jason Goepfert of SentimenTrader captures this wholesale change in market dynamics. To wit, the equal-weight S&P 500 index mooned from a 52-week low to a 52-week high in just 33 days.

33 days!

Jason notes “the only time since 1957 it happened faster was in September 1982 when the average stock went on to gain 46% over the next year.”

This about-face for the average stock in the S&P 500 tells a very different story than the Magnificent 7.

One can’t help but notice that the list of countries making new highs is growing. The list of sectors and industry groups making new highs keeps getting longer. The list of individual stocks making new highs keeps expanding.

Even certain corners of the market that have been stuck below overhead supply for years are showing signs of seller exhaustion.

Market breadth is broadening out, confirming the price action you are seeing in the major averages.

All classic behavior of a bull market in stocks.

Source: Jason Goepfert

Wealth effect back just in time for the holidays

Gas prices are now at a 2.5 year low.

Last week, AAA's national average for a gallon of gas ticked down to $3.087, its lowest level since June 24, 2021.

With the S&P 500 approaching new all-time highs, home prices appreciating meaningfully through the post-pandemic period, and gas prices nearing a $2-handle, the wealth effect is gathering some holiday cheer.

This is good news for everyone.

Source: Bespoke Investment Group

Low risk premia ahead of busy 2024 geopolitical calendar

Geopolitical events represent key risks for portfolios, but they are particularly difficult to position for – timing and market impact tend to be hard to anticipate, especially the former.

In spite of this, geopolitical risks continue to be front and center in daily conversations we have with investors. While the escalation of tensions in the Middle East since the beginning of October has re-ignited concerns, more broadly the war in Ukraine is continuing and Mainland China-Taiwan tensions are lingering. In addition, a number of elections will be held next year, including in the United States, Taiwan, and India – representing nearly half of the world’s population will be voting.

Nevertheless, risk premia remains relatively low at the moment and volatility has reset lower with the VIX near 12 after a strong, broad-based rally was induced by a relief in rates.

Geopolitical episodes can change the status quo rather quickly and drive extreme volatility in markets as investors get fearful, potentially leading to a rapid and sharp drawdown in assets.

During these periods of heightened geopolitical risk, investors may hedge more actively, either by gaining exposure to hard assets closely linked to escalation in tensions or resorting to traditional safe haven assets.

Below, you can see the results are not perfect.

Source: Goldman Sachs Global Investment Research

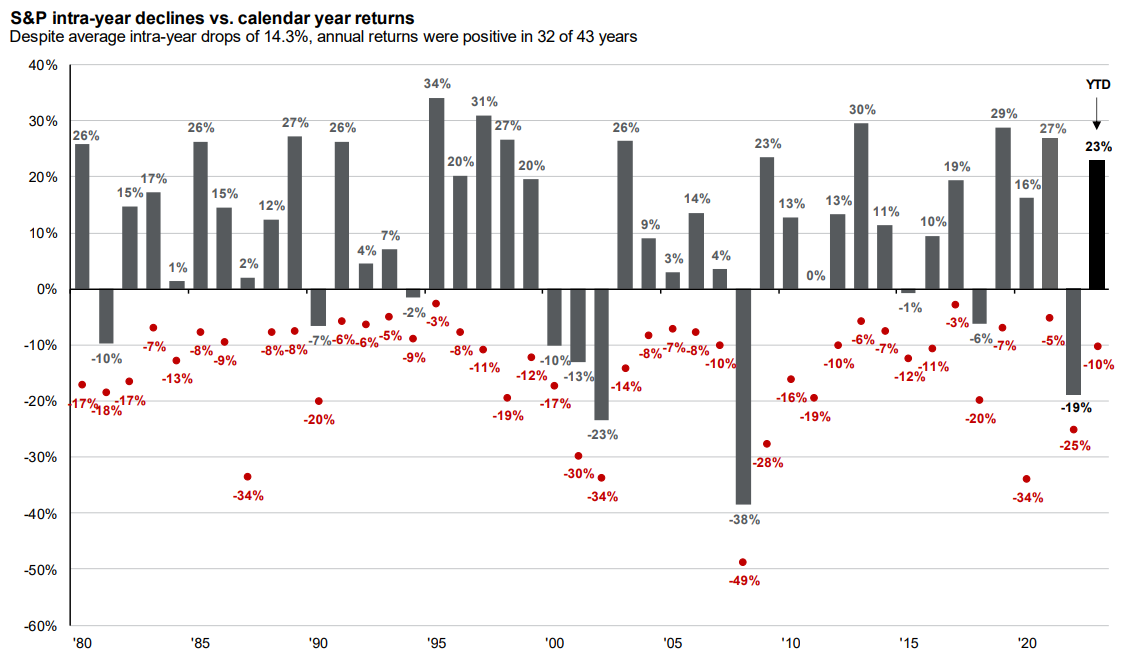

Short-term pain, long-term gain

Often times it’s easy to get caught up in the day-to-day noise of markets, when we really should be taking a step back and adopting a more long-term perspective.

In order for us to achieve those wonderful often-advertised positive returns in the long run, we often must sit through periods of underperformance in the short run that are rather uncomfortable.

To illustrate, let’s examine my favorite chart in the J.P. Morgan Guide to the Markets report.

Since 1980, the S&P 500 has averaged an intra-year decline of 14.3%, yet at the same time it has also managed to produce a positive calendar return 75% of the time.

Can’t enjoy that 75% hit ratio of positive calendar year returns in the S&P 500 index unless you endure all those red painful dots above.

Source: J.P. Morgan Guide to the Markets

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.

What an end to the year. You’re the man, Blake. Keep it up!