May seasonal trends, plus capital market assumptions (CMAs), global trade, and the week in review

The Sandbox Daily (4.28.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

seasonal trends weaken for May

BlackRock’s capital market assumptions

China behind weaker global trade volumes?

a brief recap to snapshot the week in markets

Let’s dig in.

Markets in review

EQUITIES: Russell 2000 +1.01% | S&P 500 +0.83% | Dow +0.80% | Nasdaq 100 +0.65%

FIXED INCOME: Barclays Agg Bond +0.51% | High Yield +0.43% | 2yr UST 4.029% | 10yr UST 3.435%

COMMODITIES: Brent Crude +1.49% to $79.51/barrel. Gold -0.06% to $1,997.8/oz.

BITCOIN: -0.51% to $29,334

US DOLLAR INDEX: +0.17% to 101.673

CBOE EQUITY PUT/CALL RATIO: 0.70

VIX: -7.34% to 15.78

Quote of the day

“Those who do not study the past will repeat its errors. Those who do study it, will find other ways to err!”

-Bob Farrell

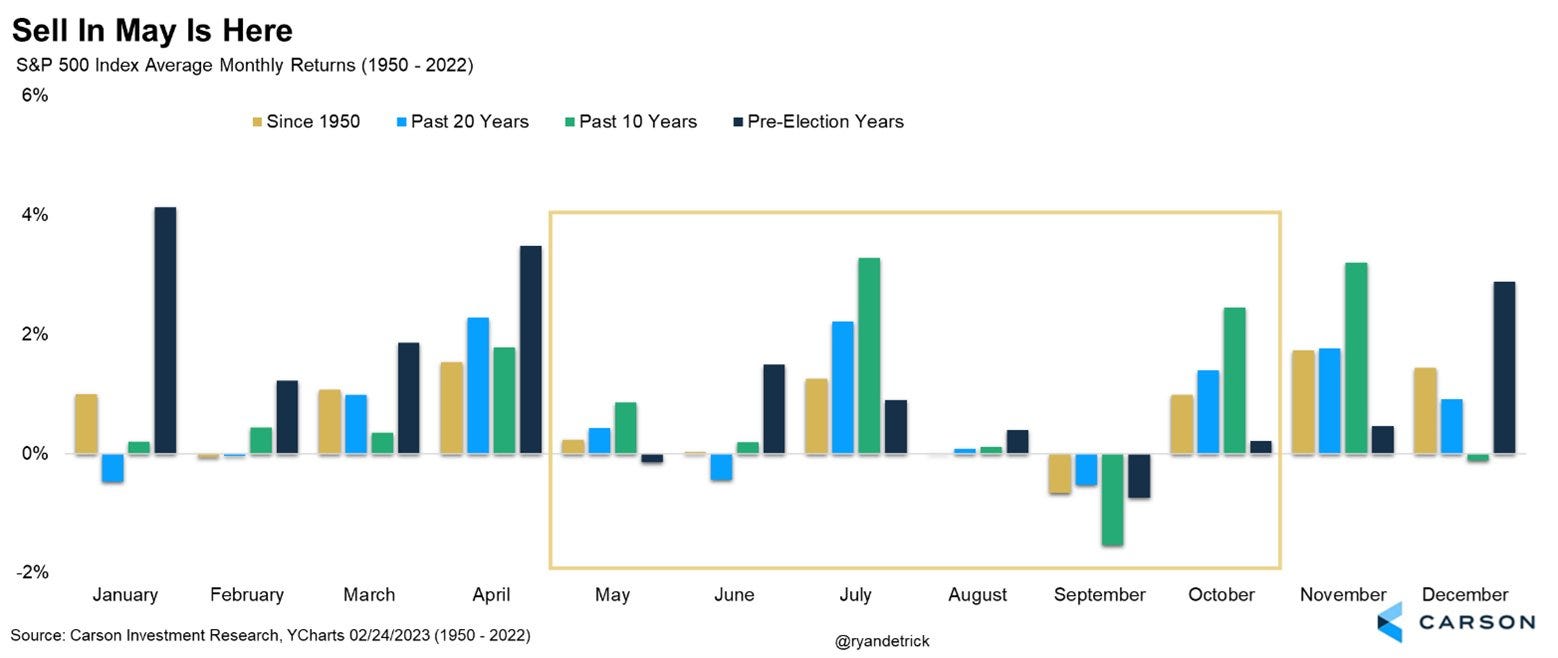

Seasonal trends weaken for May

After working through some of the strongest seasonal periods in markets, we now arrive at the “sell in May and go away” time period.

The next 6 months (May to October) are indeed the worst possible 6-month combination of the calendar year, however the S&P 500 still eeks out a +1.7% average gain since 1950 while the market is higher ~64% of the time. Not terrible.

Digging into May returns themselves, the market is only fractionally positive since 1950 (yellow bar) and up +0.9% on average in the past 10 years (green bar) – positive 9 of the last 10 times. Unfortunately, 2023 is a pre-election year in which case May is down -0.1% on average (blue bar).

Source: Carson Investment Research

BlackRock’s capital market assumptions

Capital market assumptions quantify the forward-looking risk and return prospects of all investable asset classes, and weighted together, the collection of assets are the essential inputs to formulating a strategic asset allocation framework – aka a broadly diversified multi-asset portfolio. After all, asset allocation is the primary determinant of long-run portfolio performance.

BlackRock, the world’s largest asset manager, makes their asset class return and volatility assumptions public. Along the x-axis you will find volatility and y-axis the expected return.

Equities offer greater upside potential through capital appreciation but come at the expense of higher expected volatility; Chinese equities are furthest out on the risk scale here.

The counterbalance to stocks in a diversified portfolio starts with fixed income, as bonds are more stable and cash-flow generating assets; the future path of inflation and monetary policy will be key determinants in the expected returns for bonds.

The final piece to BlackRock’s strategic asset allocation comes in the form of private market investments, which can augment traditional portfolio exposures and offer diversified growth and/or income opportunities.

Source: BlackRock, CFA Institute

China behind weaker global trade volumes?

Global trade volume growth since 2010 has generally been much slower compared to expansions in the pre-Global Financial Crisis (GFC) period. Some of this reflects the slow global growth following the GFC since it took a long time for economies to heal and rebuild from the deep recessionary crisis.

But looking at the trends by economy, it appears that China has played a disproportionally large role in the reduction in global trade volumes. The chart below shows that the shares among all the major developed economies, while subject to shorter cyclical changes in the economy, remain in long-term uptrends. The exception is China, which has seen its trade as a share of GDP fall by roughly half since 2005.

A variety of drivers have contributed to this trend: aging workforce, internalization of supply chains, the recent Trump tariffs, and more recently, onshoring, to name a few.

Source: Ned Davis Research

The week in review

Talk of the tape: Key earnings metrics still running above their historical averages and the corporate commentary still seems more supportive of a soft-landing scenario. A lot of focus on reports that regulators are working with banks to help put a rescue package together for First Republic Bank (FRC). Markets have been on the defensive as of late with many citing breadth measures as a headwind.

The Bullish dialogue emphasizes the Fed’s handling of the banking scare, better-than-feared Q1 earnings results, big tech leadership, a broader (albeit choppy) disinflation trend, elevated cash levels and still below average positioning, technicals holding strong, and the China reopening story.

Bearish talking points revolve around the central bank balancing act between inflation and financial stability risks, the higher-for-longer narrative, a policy misstep, elevated bond volatility, 10-20% downside risk to consensus earnings estimates, Fed speak, and the looming debt ceiling debate.

Stocks: Stocks ended the week mixed as over half of the companies in the S&P 500 Index have reported first quarter earnings. International stocks ended mixed this week despite improving economic reports.

Bonds: The Bloomberg Aggregate Bond Index finished higher as bond prices increased while yields declined. For credit investors, the prospect of reduced credit availability will likely lead to steady rating downgrades, but not for all (or most) companies. Large and highly rated firms can adapt to tighter bank lending standards, which is why we’ve advocated for a higher-quality approach. If anything, the notable decline in yields since late October, coupled with robust investor appetite for high-quality debt, has eased financial conditions among high-quality borrowers.

Commodities: Energy prices finished mixed for the week. Crude oil sold off while natural gas prices gained ground despite milder weather and weaker demand concerns. The major metals (gold, silver, and copper) ended the week mixed.

Source: Dwyer Strategy, LPL Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.