Monetary policy lags, plus negative-yielding debt, EV market share, Macau casinos, and Avatar: The Way of Water

The Sandbox Daily (1.9.2023)

Welcome, Sandbox friends.

Today’s Daily discusses the lag in monetary policy, saying goodbye to negative-yielding debt, EVs share of the U.S. market grows, Macau casinos dealt a tough hand, and Avatar: The Way of Water makes big splash at box office.

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 +0.62% | Russell 2000 +0.17% | S&P 500 -0.08% | Dow -0.34%

FIXED INCOME: Barclays Agg Bond +0.25% | High Yield +0.36% | 2yr UST 4.197% | 10yr UST 3.528%

COMMODITIES: Brent Crude +1.48% to $79.73/barrel. Gold +0.29% to $1,875.1/oz.

BITCOIN: +1.53% to $17,214

US DOLLAR INDEX: -0.67% to 103.181

CBOE EQUITY PUT/CALL RATIO: 0.91

VIX: +3.98% to 21.97

The lag in monetary policy

The prognostications and range of outcomes for U.S. economic growth are as disparate and wide-ranging as ever – given the confluence of data suggests that either a soft landing or hard landing is possible in 2023. With the Fed’s 425 basis points (4.25%) of interest rate hikes behind us, the question on everyone’s mind is what happens from here?

The consensus view is that the lagged effects of the Fed’s monetary tightening measures will exert an increasing drag on growth and push the economy into recession before long. On the surface, this seems consistent with Milton Friedman’s famous dictum that monetary policy operates with long (and variable) lags. But it is clear from reading Friedman’s actual quote that he was referring to the impact on the level of GDP. By contrast, both Goldman Sachs’ analysis and the academic literature imply that the peak impact of monetary policy shocks (and financial conditions shocks) on GDP growth occurs only about two quarters later.

Most of the tightening in financial conditions occurred in the first half of 2022, when markets digested the sharp change in the outlook for Fed policy, and very little net tightening has occurred since mid-year. This implies that the drag from financial conditions and Fed tightening on GDP growth should diminish significantly in 2023, barring a large renewed monetary tightening shock.

Source: Jan Hatzius (Goldman Sachs Global Investment Research)

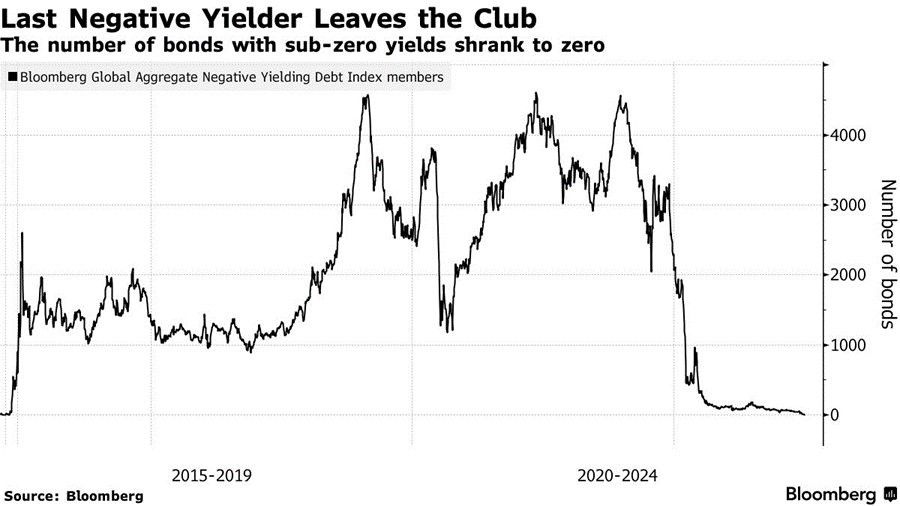

Goodbye negative-yielding debt

Remember the negative yielding debt experiment? The one where borrowers could be paid to borrow money when interest rates were held below zero?

Well, the pool of these securities, as tracked by the Bloomberg Global Aggregate Negative Yielding Debt Index, just shrank to zero.

So to recap:

2020: $18.4 trillion in negative yielding debt – the peak – across 5000+ issues of bonds

Today: $0

It only took multi-decade high inflation to cause central banks to pivot towards tighter monetary policy by implementing synchronous interest rate hikes – a painful normalization process that caused bonds to have historically porous performing in 2022.

Source: Bloomberg

EVs share of U.S. market grows

While U.S. auto sales fell 8% in 2022, electric vehicle (EV) sales grew to 5.8% of all vehicles sold, up from 3.2% in 2021.

Auto makers sold 807,180 fully electric vehicles in the U.S. last year. Tesla still dominates the U.S. EV market, accounting for 65% of total sales last year, while Ford Motor Co. jumped into the number 2 position in EV sales, accounting for (just) 7.6% of the U.S. market for fully electric vehicles.

The shifting market dynamics reflect early jockeying in a sector that remains a small slice of the broader car market, but is being targeted by auto executives as a major growth opportunity. Some near-term obstacles have emerged over the past year, such as the rising cost of lithium and other battery minerals that are prompting car makers to raise prices; the average price paid for an EV in the U.S. hit about $66,000 last summer, up from about $51,000 a year earlier, according to J.D. Power.

Source: Wall Street Journal, The Hill

Macau casinos dealt a tough hand

Macau, a special administrative region of China and major gambling destination hit hard by Covid lockdowns, saw casino revenues in 2022 plummet 51% YoY to $5.24B – it’s worst year since 2004 as China’s strict Covid Zero policies wrought havoc on the gambling hub.

Short-term headwinds remain after China’s abrupt U-turn on Covid-zero policy in December sparked a record wave of infections in both the mainland and Macau. But the mainland’s reopening in January, and Macau’s own moves to scrap quarantine for overseas arrivals, paves the way for a major rebound for gaming in 2023. Casinos also face brighter prospects over the longer-term. All six current operators were recently granted new licenses for 10 years, with the decision removing a major uncertainty that had hung over the sector for much of the past year.

Source: Financial Times, Bloomberg

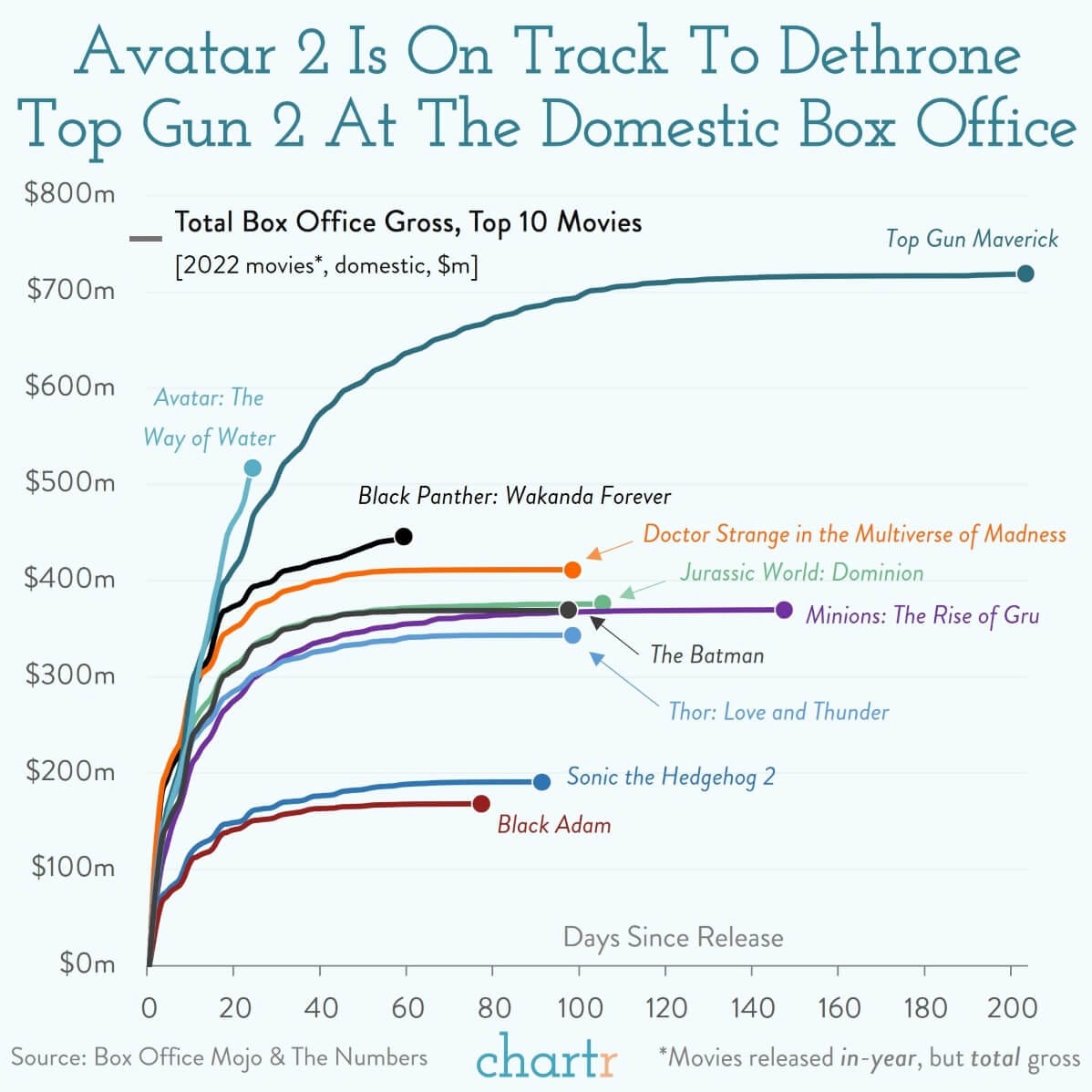

Avatar: The Way of Water makes big splash at box office

After only four weeks of release, James Cameron’s Avatar: The Way of Water has made $1.71 billion worldwide, which puts it above the $1.49 billion made by Top Gun: Maverick last summer to become the 2nd-highest grossing films of the pandemic era, after Spider-Man: No Way Home which made $1.91 billion. The latest box office figures elevates the 2nd installment of the franchise into the 7th-highest grossing movie spot in history.

In the United States, however, its $517mm haul hasn’t been quite enough to knock Top Gun: Maverick off the top spot — though it’s tracking to do so based on the first 24 days of the movie’s release.

Director James Cameron has been quoted that The Way of Water needed to become one of the highest grossing films of all time just to break even. The movie’s exorbitant budget was rumored to top $450mm – $350 million dollars spent in production costs and another $100 million dollars spent on marketing.

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.