Money availability, plus strength from communications, the IPO draught, minimum wage, and the week in review

The Sandbox Daily (5.5.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

money availability problem

communications showing leadership

IPO draught

minimum wage

a brief recap to snapshot the week in markets

The 149th running of the Kentucky Derby will take place Saturday at Churchill Downs in Louisville, Kentucky. Post time is 6:57 p.m. ET. Forte opens as the 3-1 favorite.

Let’s dig in.

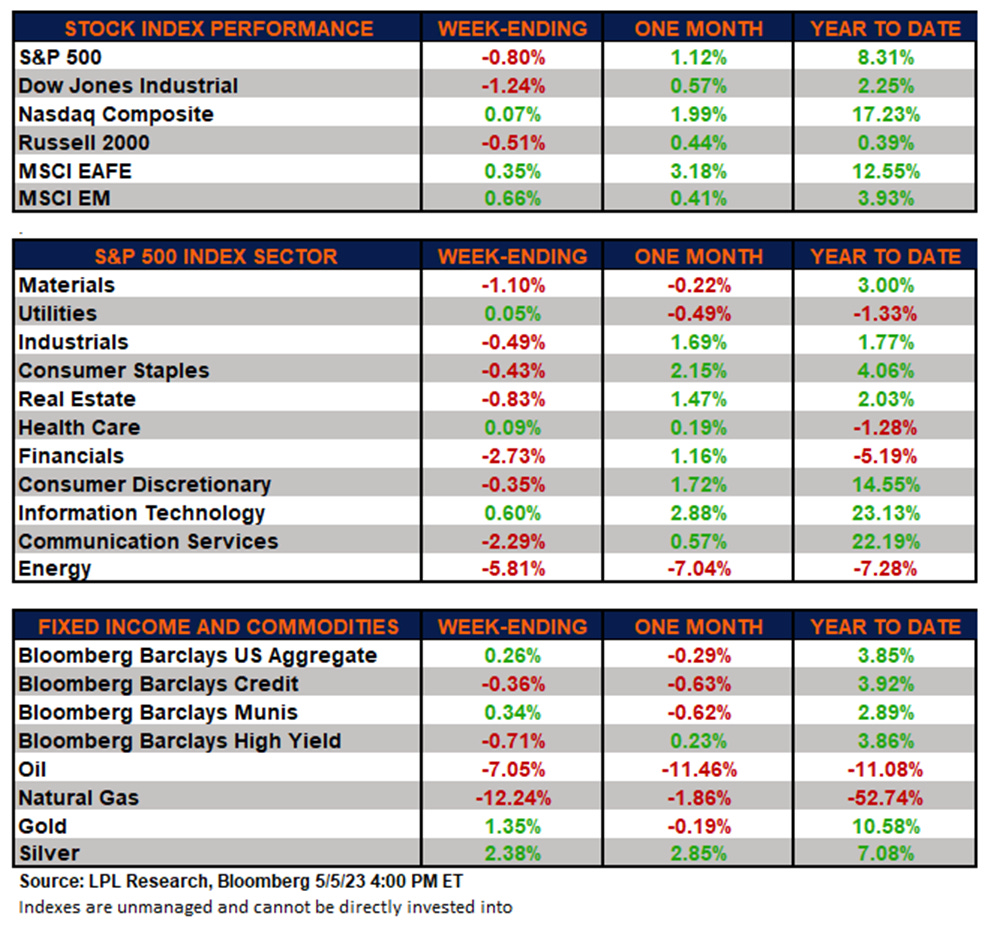

Markets in review

EQUITIES: Russell 2000 +2.39% | Nasdaq 100 +2.13% | S&P 500 +1.85% | Dow +1.65%

FIXED INCOME: Barclays Agg Bond -0.32% | High Yield +0.54% | 2yr UST 3.918% | 10yr UST 3.435%

COMMODITIES: Brent Crude +4.01% to $75.41/barrel. Gold -1.50% to $2,024.9/oz.

BITCOIN: +2.30% to $29,544

US DOLLAR INDEX: -0.12% to 101.282

CBOE EQUITY PUT/CALL RATIO: 0.82

VIX: -14.44% to 17.19

Quote of the day

“Adversity is either a privilege or a tragedy, depending on how you respond to it.”

- Mike Day, Navy SEAL

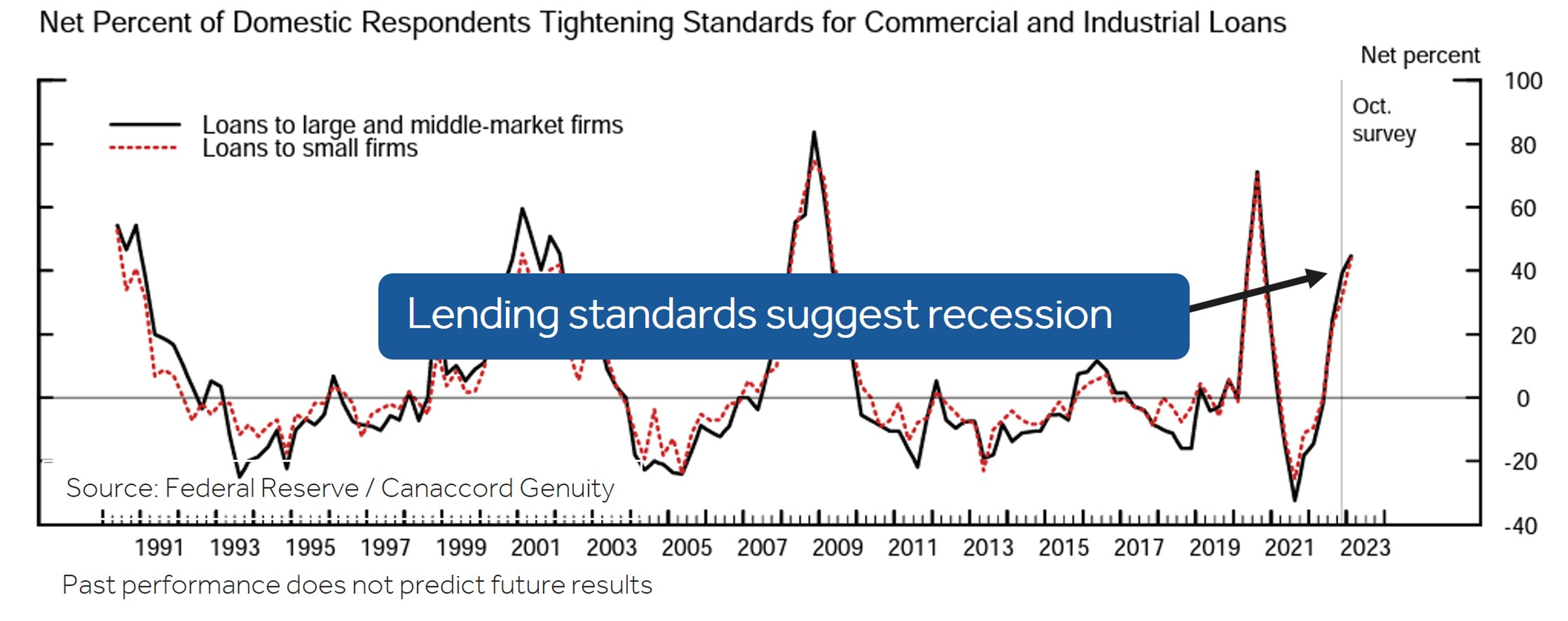

Money availability problem

The markets have been very volatile around chatter that various regional banks are reportedly in trouble. The financial media and traders continue to focus on the “systemic” side of this, but the much more important factor is how the uncertainty further pressures money availability and tightens Bank Lending Standards and overall Financial Conditions.

After all, here are the Google search results for “bank” right now. The headlines are an absolute disaster right now. Does this instill confidence in investors?

What must change to resolve our money availability problem?

The reason the market bottoms during a recession is that the economic weakness causes a spike in unemployment and fear of disinflation significant enough to: (1) force a Fed pivot causing a sharp reduction in short-term interest rates that (2) steepens the yield curve to improve bank lending conditions which (3) significantly improves the sentiment and outlook for money availability.

The Fed just raised rates by 500 basis points in 14 months, and unemployment has yet to see a significant rise. Fed Chairman Jerome Powell and the FOMC had the recent Senior Loan Officer Survey results in hand this week (ahead of the 25 bps hike to 5-5.25%) which Powell said the survey showed further tightening of credit conditions.

This makes perfect intuitive sense: rate hikes are tightening financial conditions and slowing economic activity.

It is hard to see an improved outlook for money given this backdrop, but that can change fast.

Source: Dwyer Strategy

Communications showing leadership

Trends don't usually shift from up to down, or vice versa, in rapid fashion. More often than not, there is a prolonged period of sideways, or trendless price action between the uptrend and downtrend phase.

This process is called basing. Here’s what it looks like, using the SPDR Communications ETF (XLC) as an example:

Notice how price bottomed out late last year and rallied back to the August highs before correcting back to the 200-day moving average (MA). It has since tested those pivot highs twice: once in April, and again this week.

While buyers have yet to force an upside resolution, more of the overhead supply at this key level is absorbed with each test. It could only be a matter of time until $XLC resolves higher, setting the stage for a new uptrend.

Source: All Star Charts

IPO draught

Global quarterly initial public offerings (IPOs) have fallen to their lowest level in almost a decade.

Q1 was another down quarter for raising capital amid the rise in interest rates, a lukewarm stock market, and unexpected global banking industry turbulence. Appetite for new companies coming to market is nearly non-existent.

Despite this ongoing uncertainty around the economic and geopolitical environment, the IPO pipeline continues to build up and hope remains for a turnaround later this year.

Source: Ernst Young

Minimum wage “pet thesis”

The always eloquent and wonderful Barry Ritholtz had this to say about how modest increases in the minimum wage increase economic activity and create jobs:

“I have been nurturing a pet thesis as to why higher minimum wages are a net positive for an economy: It acts as a transfer of revenue allocation from low-wage employers and franchisees, from Capital to Labor. Meaning, less profits to ownership and more wages to workers.”

Minimum wage is as much an economic issue as it is political, but empirical data does suggest an economy is more robust and productive when wages are higher in the lower quintiles of the income brackets. More income flows downstream to low-wage workers – themselves more prone to operating paycheck-to-paycheck, and most of their spending benefits the local, regional economy. Each marginal discretionary dollar will end up impacting thousands of small businesses all across the country.

Over time, the trend in the percentage of workers earning minimum wage is down. For both men and women. This is good.

44% of the U.S. workers earning minimum wage are 24 years old or younger; 25% are between the ages of 25-34.

These formative years are the most important years when launching and building your career – while sowing the seeds for capital building endeavors as your progress through life.

Source: U.S. Bureau of Labor Statistics, Zippia, Barry Ritholtz

The week in review

Talk of the tape: Stocks ended the week with a big surge, although it was a tough week for most risk assets. The debit ceiling debate is coming into focus as a major near-term headline risk.

The bull/bear debate continues, though the elements are now well understood.

Recent equity strength largely chalked up to better-than-expected Q1 earnings, while earnings guidance/revision ratios have shown some improvement as well. Expectations for the Fed moving to the sidelines is another positive spin. In addition, the corporate buyback window is reopening.

Still plenty of bearish talking points. Lot of scrutiny surrounding narrow upside leadership and weak market breadth. Valuation is another overhang. Also doubts about market pricing for a H2 policy pivot from the Fed. Debt-ceiling stalemate and potential spending cuts out of Washington another overhang.

Stocks: U.S. stocks ended the week mostly lower as the energy, financials, and communication services sectors lagged. Roughly 85% of the S&P 500 Index has now reported first quarter results, with earnings beat/surprise metrics ahead of recent averages. However, bank concerns continue to weigh on investors’ minds following reports that PacWest Bancorp (PACW) is exploring strategic alternatives amid a steep decline in its share price.

Bonds: The Bloomberg Aggregate Bond Index finished higher as bond prices increased while yields declined. Credit default activity increased in April to a 33-month high and raised both the high-yield bond and leveraged loan default rates to a 2-year high. Total defaults already account for 74% of last year’s $47.8 billion full-year total and have easily surpassed 2021’s full-year 14-year low of $13.9 billion. As lending standards continue to tighten due to stress in the banking sector, expectations are for defaults to continue to rise and high yield bond yields and spreads to widen.

Commodities: Energy prices finished lower this week on concerns over future demand following weaker-than-expected economic reports out of China, the world’s largest oil importer. OPEC+ began voluntary output cuts at the beginning of May, however some traders remain skeptical that the cuts will actually happen. The major metals (gold, silver, and copper) ended the week mixed.

Source: Dwyer Strategy, LPL Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.