Money Market Fund flows, plus real rates, VIX, wage gains, and the week in review

The Sandbox Daily (10.20.2023)

Welcome, Sandbox friends.

Today’s Daily discusses:

Money Market Fund inflows persist

are real rates restrictive enough?

VIX breaches 20, finally

wage gains propel the American consumer

a brief recap to snapshot the week in markets

Happy Friday folks - we made it to the weekend!

Let’s dig in.

Markets in review

EQUITIES: Dow -0.86% | S&P 500 -1.26% | Russell 2000 -1.29% | Nasdaq 100 -1.50%

FIXED INCOME: Barclays Agg Bond +0.36% | High Yield +0.21% | 2yr UST 5.071% | 10yr UST 4.909%

COMMODITIES: Brent Crude -0.17% to $92.22/barrel. Gold +0.70% to $1,982.2/oz.

BITCOIN: +3.10% to $29,626

US DOLLAR INDEX: -0.09% to 106.160

CBOE EQUITY PUT/CALL RATIO: 0.78

VIX: +1.45% to 21.71

Quote of the day

“Follow the evidence wherever it leads, and question everything.”

- Neil deGrasse Tyson

Money Market Fund inflows persist

The steady flows from U.S. bank deposits into Money Market Funds continues, months after the mass exodus of cash back in March and April 2023 when the regional and small banking crisis boiled over.

J.P. Morgan estimates the pace is averaging roughly $60 billion per month since the end of May.

A market environment under duress from simultaneous stock and bond losses, investors continue to favor safety and risk-free return with cash paying over 5%.

Source: J.P. Morgan Markets

Are real rates restrictive enough?

One can partly attribute the resiliency of the global economy to real rates being lower than in past extreme tightening cycles. Real rates are the nominal interest rate less annualized CPI.

At 1.64%, the real global central bank rate is the highest since 2009 – see the bottom pane of the chart below. But it peaked at a much greater 3.00% and 2.75% in 2000 and 2006, respectively.

Moreover, the percent of central banks with negative real target interest rates is at 40%, compared to around 0% in 2000 and 2007.

On rates in the United States, Nick Colas of DataTrek writes:

10-year Treasurys continue to rise due solely to higher real yields (not inflation expectations). Assuming real yields go to 2 standard deviations above the long run mean, nominal yields should reach 5.2%. That’s not far from today & current momentum says they'll get there quickly.

Source: Ned Davis Research, DataTrek

VIX breaches 20, finally

The steady hand, no more.

The VIX streak of consecutive closes below 20 ended yesterday after 105 days, the longest streak since just before the COVID-19 pandemic.

Source: The Daily Shot

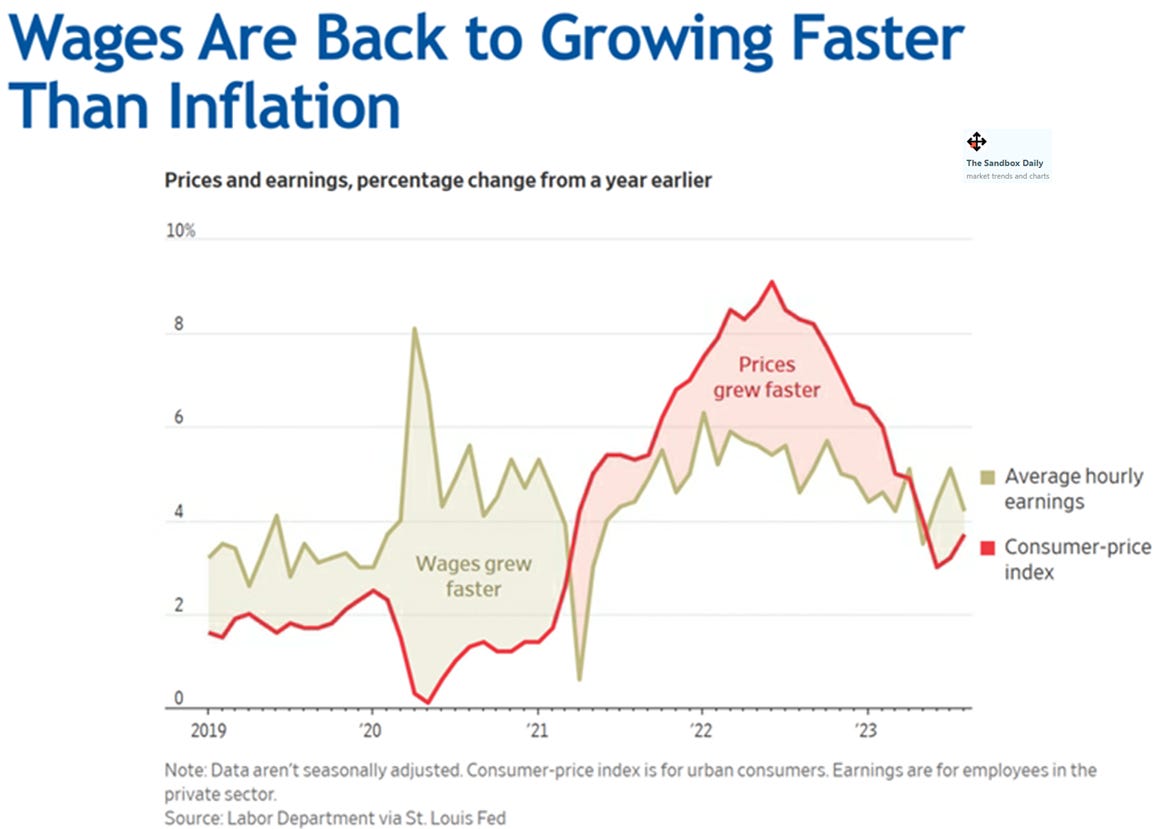

Wage gains propel the American consumer

While naysayers continue to say inflation is hurting wage earners, this was true when prices spiked in 2021 and 2022 – but this dynamic has now reversed.

Wage gains will persist, while price gains will subside.

This trend is but one example showing the American consumer continues to propel the economy forward on a path of growth.

Source: Wall Street Journal

The week in review

Talk of the tape: We are currently experiencing a no-bid market right now. Equity investors remain on edge with the relentless march higher in U.S. Treasury, mortgage, and corporate credit rates. Ultimately, the market needs confirmation that the move in the rates market hits the pause button, if not roll over, before a more durable year-end rally for equities can take shape. Such a dramatic change in the bond market tone might only come from either a financial market event or extreme weakness in the economic data. Meanwhile, earnings results have come in mostly better than anticipated.

Soft-landing expectations underpin the bullish narrative, centered around a labor market that just won’t quit. The potential for a return to positive earnings growth in Q3, record amount of money market assets on the sidelines, and favorable seasonality in Q4 flagged as other bullish drivers. Consumer resilience, although showing some signs of fatigue, continues to be a higher-profile bright spot.

Bearish talking points, which are gaining traction over the last few weeks, revolve around the upward pressure on rates, liquidity headwinds, and the lagged effects of policy tightening (19 months now). Geopolitical concerns, oil markets, and House Speakership all cited as near-term overhangs as the market decides what to make of their implications. Narrow market leadership a steady talking point among the bear camp.

Stocks: Equity markets have suffered 3 consecutive days of heavy selling pressure and remain in a firm down channel from the July highs. Approaching 5% on U.S. Treasurys has caused an inflection where equity buyers are stepping aside. When coupled with uncertainties around Israel-Gaza and the Washington political circus, one can see why markets went on a buyers strike this week.

Bonds: Another tough week for bond holders – no surprise. The Aggregate Bond Index is down -3.5% this month. High yield bond yields and spreads rose over the past week amid elevated rate volatility, limited capital market activity, and a third consecutive $2+ billion weekly retail outflow.

Commodities: Commodities had a mixed week amid the recent geopolitical crisis in the Middle East. The International Energy Agency last week described market conditions as “fraught with uncertainty” but stated that the Israel-Hamas war had not yet directly impacted physical energy supplies.

Source: Dwyer Strategy, LPL Research

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.