Negative earnings, plus valuation reset, dividend-payers, and the trend is your friend

The Sandbox Daily (1.19.2023)

Welcome, Sandbox friends.

Today’s Daily discusses the outlook for corporate earnings, the reset in valuations, a positive development for dividend-paying stocks, and the trend is your friend.

Let’s dig in.

Markets in review

EQUITIES: S&P 500 -0.76% | Dow -0.76% | Russell 2000 -0.97% | Nasdaq 100 -1.00%

FIXED INCOME: Barclays Agg Bond -0.23% | High Yield -0.59% | 2yr UST 4.122% | 10yr UST 3.399%

COMMODITIES: Brent Crude +1.49% to $86.25/barrel. Gold +1.41% to $1,933.8/oz.

BITCOIN: +1.24% to $21,041

US DOLLAR INDEX: -0.30% to 102.061

CBOE EQUITY PUT/CALL RATIO: 1.31

VIX: +0.88% to 20.52

Earnings declines ahead?

Famed Canaccord Genuity strategist Tony Dwyer is often quoted as saying: “Over time, the market correlates to the direction of earnings (EPS), EPS is driven by the direction of economic activity, economic activity is produced by the availability of money, money availability is driven by Fed policy, and Fed policy is driven by Inflation and Employment.”

With earnings season upon us, investors are paying close attention to what companies are reporting (4Q22) and what management is projecting (2023). So let’s dive into the numbers.

The estimated earnings decline for the S&P 500 for 4Q22 is -3.9%, which would mark the 1st year-over-year earnings decline reported by the index since Q3 2020 (-5.7%). This we know. This quarterly earnings cycle will likely come in weak and the market has priced in these expectations. But, perhaps more importantly, do analysts believe earnings declines will continue in 2023?

The answer is yes. Over the past few weeks, earnings expectations for 1Q23 and 2Q23 switched from YoY growth to year-over-year declines. Here are the estimated earnings growth rates progressing through time:

June 30, 2022

* Q1 2023: +9.6%

* Q2 2023 +10.3%

September 30, 2022

* Q1 2023: +6.3%

* Q2 2023: +5.1%

Today

* Q1 2023: -0.6%

* Q2 2023: -0.7%

As of today, the index is now expected to report three straight quarters (Q4 2022 through Q2 2023) of YoY earnings declines. If this happens, it will mark the 4th time it has occurred since 2015. The last time the index reported at least 3 straight quarters of YoY earnings declines was 1Q20 through 3Q20.

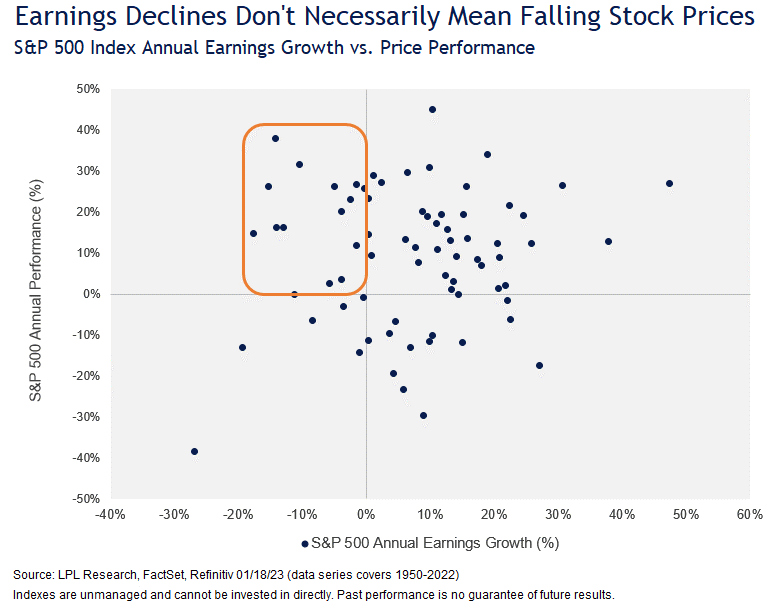

Going back to Tony Dwyer, what is the direction of the market if earnings drive stock prices?

Looking at the history of earnings growth plotted against S&P 500 price performance, the results are somewhat mixed, although there is a definitive clear bias for positive earnings growth leading to positive stock performance (top right quadrant below).

In terms of the current environment and expectations, you can see in the chart below that in years when earnings fall, found on the left side of the graph, stocks are actually more likely to rise than fall (more dots are in the upper left quadrant than in the lower left one).

This may seem counterintuitive, but it makes sense when we remind ourselves that markets are forward looking. The markets generally price in earnings declines well before they happen—maybe two or three quarters ahead. By the time earnings declines are in the books, stocks have move higher in anticipation of the next earnings upcycle.

Source: Canaccord Genuity, FactSet, LPL Research

The great reset

Valuations moved materially lower over the last year, with bond valuations resetting the most on the back of rates rising from 0% to 4.5% through 2022.

Equities have also reset lower and at current, do not appear as expensive as they were before. Within equities, the pockets that needed to correct have now done so. For example, SaaS software has contracted from 20x enterprise value (EV)/ forward revenues in November 2020, to ~5.5x today. Semiconductors P/E multiple declined from 23.5x in February 2021 to 17.8x today. And publicly traded REITs now trade at a 26.1% discount to net asset value (NAV). In private markets we’ve seen venture capital valuation correct, private credit returns decline, and commercial real estate price also started to correct.

Were the 2022 re-ratings of price multiples enough or is further compression necessary given the projected economic recession, slowing earnings cycle, and fatigued consumer?

Source: Anastasia Amoroso

Have bonds peaked? That would be welcome news for dividends.

The two-year yield peaked at 4.72% on November 7, the five-year at 4.44% on October 20 and the 10-year at 4.24% on October 24. Since then, all three maturities have contracted as inflation has moderated and interest rate hikes have been smaller than those earlier in the year.

This could be good news for dividend-paying stocks. The five-year yield has shown historical periods of correlation with dividend-paying stocks. When the yield on the five-year note built momentum by crossing above its 50-day moving average (yellow arrows in the chart below), dividend-paying stocks became less attractive. And conversely, when the yield fell below the moving average, stocks began to recover.

We’re seeing that play out now – see the chart below. The S&P 500 Dividend Aristocrats Index, which tracks stocks that have been increasing their dividends for at least 25 years – think legacy companies like Clorox, McDonald’s, Johnson & Johnson and AT&T – hit its 2022 low when the five-year yield was well above its 50-day moving average. Stocks began to rebound when the yield fell below its moving average.

The five-year yield is once again trading below the key moving average, meaning momentum is slowing and this development could be constructive for dividend-paying stocks.

Source: VettaFi

The trend is your friend, unless it’s down

Investors are laser focused at the moment on the downward-sloping 200-daily moving average trendline for the S&P 500 index. (see Tuesday’s The Sandbox Daily for more information)

Why does the 200-DMA matter so much?

When the index is sitting above the 200-DMA, your returns are higher with less volatility - offering investors a better risk-adjusted return.

What’s interesting though is over the past couple of decades, whether the average is rising or falling has mattered a lot more than whether the index is above or below it.

Source: Willie Delwiche

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily.