No stress in credit, plus the Strategic Petroleum Reserve (SPR) rebuild, cash on the sidelines, and small-caps

The Sandbox Daily (8.27.2024)

Welcome, Sandbox friends.

The market has been stuck in a bit of a holding pattern this week as it awaits Nvidia's quarterly earnings report tomorrow (Wednesday). Fed Chair Jerome Powell delivered last week; now it’s Nvidia’s turn.

Today’s Daily discusses:

bonds aren’t stressed, are you?

SPR rebuild should support oil prices

an object in motion stays in motion

consider small-caps after Fed’s first rate cut

Let’s dig in.

Markets in review

EQUITIES: Nasdaq 100 +0.33% | S&P 500 +0.16% | Dow +0.02% | Russell 2000 -0.67%

FIXED INCOME: Barclays Agg Bond +0.03% | High Yield +0.06% | 2yr UST 3.901% | 10yr UST 3.829%

COMMODITIES: Brent Crude -1.90% to $79.88/barrel. Gold +0.18% to $2,559.8/oz.

BITCOIN: -2.56% to $61,959

US DOLLAR INDEX: -0.30% to 100.552

CBOE EQUITY PUT/CALL RATIO: 0.57

VIX: -4.46% to 15.43

Quote of the day

“Investing in the market without knowing what stage it is in is like selling life insurance to 20-year-olds and 80-year-olds at the same premium.”

- Victor Sperandeo

Bonds aren’t stressed, are you?

When markets are under stress, it shows up in credit spreads.

The bond market is the biggest segment of the capital markets, with a total valuation at roughly $130 trillion. If there’s serious systemic risk in the stock market, credit spreads will notify investors.

So far, these spreads have been narrowing, not widening – despite the temporary growth scare earlier this month.

The High Yield option-adjusted spread (OAS) is currently around 321 bps, well below its mean of 524 bps and median of 466 bps since 2000. The record low was 241 bps in May 2007, while the pandemic low was 266 bps.

Equities benefit when credit spreads contract, and that’s exactly the environment we’re in now.

With more stocks pushing higher and participation expanding – the NYSE Advance-Decline Line is at all-time highs – stock market bears have little to support their thesis.

Source: St. Louis Fed, WisdomTree, All Star Charts

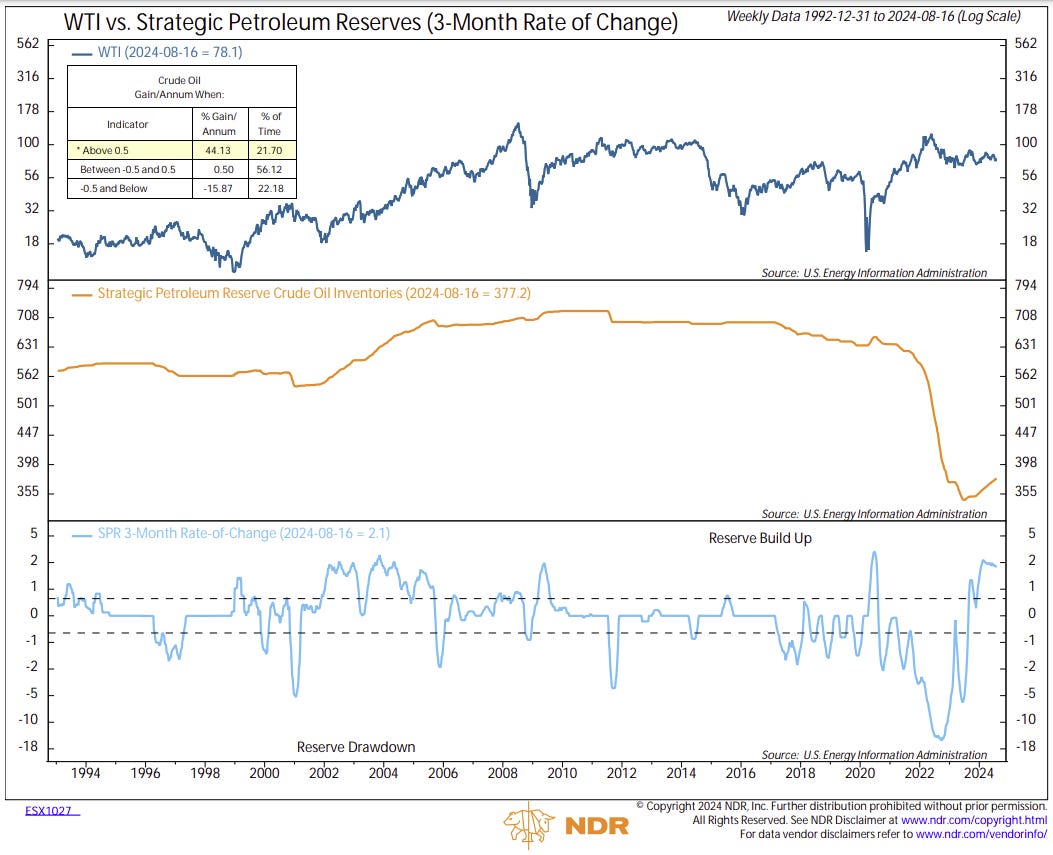

SPR rebuild should support oil prices

The Biden administration drew down roughly 45% of the Strategic Petroleum Reserve (SPR) to help contain rising gasoline prices during the early days of the pandemic and then later spiking energy prices amid Russia’s invasion of Ukraine.

President Biden inherited an SPR at 638.08 million barrels when he took office in January 2021.

The stockpile then reached its lowest level since 1983, touching 346.76M in July 2023. Today, we are up to just 377.16M – a gain of just 8.7%.

The administration installed a three-pronged strategy to return oil to the reserve: buy back oil in the open market, return oil on loan from the SPR, and work with Congress to overhaul congressionally-mandated SPR sales through 2027, which lawmakers previously voted for to fund government programs. Additionally, policy is being lobbied to reduce the minimum supply required because of the significant decline in U.S. oil imports over the past decade.

As the U.S. government replenishes its coffers over the coming months and years, oil prices should find a constant bid underneath the market.

Source: Ned Davis Research, Federal Reserve Bank of Dallas

An object in motion stays in motion

Money market fund assets have risen to another fresh record. Again.

Roughly $24.89 billion flowed into U.S. money market funds in the week ending August 21, bringing the total stock of money market funds to an all-time high of $6.24 trillion, surpassing the previous record $6.19 trillion reached in the prior week.

The chart below (data stale a/o the prior week) shows the parabolic move higher in money market funds over recent years.

Retail investors have piled into these cash-equivalent vehicles since the Federal Reserve began one of the most aggressive tightening cycles in decades in 2022 and 2023.

The inflows have so far continued, despite investors expecting the U.S. central bank to begin its rate cutting cycle next month.

Source: Investment Company Institute, Isabelnet

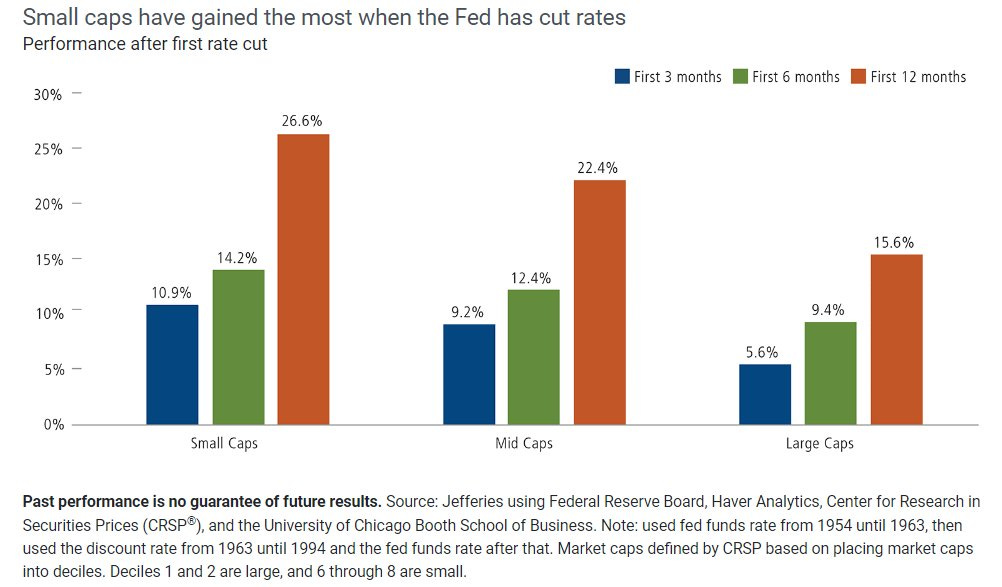

What does best on the cap stack as interest rates fall?

History shows that small-cap stocks outperform their larger-cap siblings after the Fed’s first rate cut.

This is typically due to small-caps being more sensitive to improving economic activity while also having more leveraged balance sheets.

Source: Calamos Investments

That’s all for today.

Blake

Welcome to The Sandbox Daily, a daily curation of relevant research at the intersection of markets, economics, and lifestyle. We are committed to delivering high-quality and timely content to help investors make sense of capital markets.

Blake Millard is the Director of Investments at Sandbox Financial Partners, a Registered Investment Advisor. All opinions expressed here are solely his opinion and do not express or reflect the opinion of Sandbox Financial Partners. This Substack channel is for informational purposes only and should not be construed as investment advice. The information and opinions provided within should not be taken as specific advice on the merits of any investment decision by the reader. Investors should conduct their own due diligence regarding the prospects of any security discussed herein based on such investors’ own review of publicly available information. Clients of Sandbox Financial Partners may maintain positions in the markets, indexes, corporations, and/or securities discussed within The Sandbox Daily. Any projections, market outlooks, or estimates stated here are forward looking statements and are inherently unreliable; they are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur.